Over 28 million Americans are what’s known as credit invisible, lacking a credit score that makes them eligible for everything from a mortgage to a credit card. While you might be aware that a good credit score can provide opportunities, and a bad credit score can disqualify you from them, having no score at all can shut the door on being able to buy a house, getting credit card perks, and investing in your financial future.

Everyone has to start from somewhere, including with credit scores. Here’s how you can start your journey and build a credit score from total scratch.

Why You Should Care About Building Your Credit Score

When evaluating you as a borrower, lenders will want to know what your score is so they can determine how much of a risk you are to lend to. Borrowers with a high score indicate that they make their payments on time and manage their credit well, which make them attractive customers for lenders. As such, a higher score can get you better rates and more exclusive products with better perks. Insurance companies will even offer discounts on your premiums if you have a good score.

On the other hand, having a low score, or no score at all, will disqualify you from most lending products and services, including mortgages, auto loans, and business loans, which can wall you out of many options in life. Having a credit card is also a requisite to many services, including renting a car or checking into a hotel room.

The impact can even go beyond borrowing. Many landlords will require a minimum credit score, and some utility companies will require an up-front deposit if you lack a credit score.

How Credit Scores Work

Credit scores offer a quick way for lenders to evaluate potential borrowers by quantifying how good they are at borrowing and making payments. Scores are based on your credit report, which is a compiled history of the money you’ve borrowed, your on-time and missed payments, the accounts you have open, and other important factors in your credit habits.

Credit report history is compiled by the three credit reporting agencies: Equifax, TransUnion, and Experian, all of which have slightly different ways of collecting data and reporting it. You can request your credit report for free from each of these bureaus, or from annualcreditreport.com. Checking it at least quarterly is recommended to stay on top of your score and report.

From there, there are two major scoring systems for credit scores: FICO and VantageScore, which pull data from the reporting agencies and use it to calculate your score. While the methods discussed in this article apply to both systems, we’ll be using FICO scores as the main basis, since this is the model most lenders use when qualifying you for credit.

What You Need for a Credit Score

In a nutshell, in order to have a credit score at all, you’ll need:

- You will need to be at least 18 years old. You can start establishing your credit history before that if you’re an authorized user on someone else’s card (more on that later.)

- At least one open lending or credit account in the United States. If you do not have an open account, you will be reported as having no score at all.

- A Social Security Number or Individual Taxpayer Identification Number. Not only will you need this if you are applying for a card or loan, but the credit bureaus use this to link your accounts to your identity.

As soon as you open up a credit account, whether it’s taking out a loan or getting a new credit card, your lender will start reporting your payment history and account balances to the credit reporting bureaus. While there is some information you can choose to report through third parties, such as rental payment information, in general, the process is automatic.

It will take some time for your score to be established once you open a new account. For FICO, you need to have an account open for at least six months before it can contribute to your score. For VantageScore, the minimum account age is only one month.

Credit Score Ranges

FICO scores range from 300 to 850, with a set of smaller ranges qualifying your score in a certain way. Here’s a quick summary of the FICO scores and what they mean for you as a borrower. (Note that while Monarch uses VantageScore, FICO is the most common scoring model used by lenders.)

800 to 850 | Excellent/Exceptional | Top score, which qualifies you for the best lending products and rates |

740 to 799 | Very Good | High chance of approval and a good rate |

670 to 739 | Good | Good chance of approval, but you won’t get the best rates |

580 to 669 | Fair | Usually the minimum for lenders. You’ll be offered sub-par rates. |

300 to 579 | Poor | Low chance of approval, with extremely high rates and limited options |

The Five Factors That Determine Your FICO Score

When calculating your score, FICO uses five key factors from your credit report to calculate your score, each of which are weighted in a different fashion. These include:

- Payment history (35%), which includes on-time and missed payments, defaults, delinquencies, and bankruptcies.

- Utilization (30%), which is how much of your available credit you are using. For example, if you have a total credit limit of $5,000 across all your cards and a combined card balance of $1,000, then your utilization is 20%. The lower your utilization, the better.

- Length of credit history (15%), which is calculated accounting for the average age of your accounts, the age of your oldest account, and the age of your newest account. The longer your history, the better.

- New inquiries (10%), which looks at how many times you have officially applied for a credit or loan product in a certain span. These are known as “hard inquiries,” and while one or two hard inquiries won’t pull down your score much, making too many in a short period can tank your score.

- Credit mix (10%), looks at the mix of accounts you have on your credit file. Ideally, you should have a combination of revolving credit (credit cards and lines of credit) and installment loans (like mortgages, student loans, or auto loans), instead of only one type.

When you’re establishing your credit score, it’s important to keep these factors in mind as you build up your history and apply for new loans and cards.

8 Proven Ways to Build Credit From Scratch

There’s more than one way to build credit. Which method you choose will depend on your individual circumstances, how much money you’re willing to put down or spend, and what resources you have available to you.

Here’s the quick rundown.

Cost | Score boost potential | Best for | Pros | Cons | |

Secured card | $100 to $500 | Medium | Users starting from scratch, so long as they have the deposit | Anyone can apply Cards can offer perks | Requires money up front for deposit Deposit may be at risk Required you to regularly pay it off |

Authorized user | $0 | High | Those who know someone who trusts them to be an authorized user and has a long, positive payment history | Easy access to long-tail credit history No fees | Requires someone who trusts you enough to give you a card Main card holder will need to make payments on time |

Credit builder loan | $100 to $600 | Medium | Users who are starting from scratch, so long as you can afford the fees | Anyone can apply | Costs money for interest and loan fees Requires timely payments |

Reporting rent/utility payments | $0 to $50 (besides the payment itself) | Medium | Renters and building a history from zero | Easily accessible if you make timely payments Previous history can count | Missed payment can count against you Some reporting services may require a fee |

Student card | $0 | Medium | Students | Easily accessible to students Often no fees Perks for good grades | Limited to students Requires a source of income |

Store/retail card | $0 | Medium | Users starting from scratch if they lack funds for a deposit or interest | Low to no credit requirements Can come with store perks or rewards | High interest rates Low utilization limit |

Co-signer | Varies | High | IUsers with someone with a high score whom they trust, and can make loan payments | Can make loans more accessible | Requires someone you trust who will co-sign with you You or co-signer will need to make timely payments Co-signer is on the hook if you miss a payment |

Alternative reporting | Varies | Medium | Users who frequently use BNPL and make payments on time, or if you want to qualify for a loan with no score | Works well if you regularly use BNPL Can open up credit opportunities with consistent payments | Requires use of BNPL Not all BNPL services report to bureaus Can have additional fees for manual underwriting |

Here are the methods in a bit more detail.

Open a Secured Credit Card

A secured credit card is a credit card that is backed by a security deposit, usually ranging from $100 to $500. The amount of the deposit determines the credit limit. Depending on the card’s policy, if you miss one or more monthly payments, then the balance will either be taken out of the deposit, or the entire deposit will be forfeited. As such, these types of cards typically don’t require you to have a credit history or a high score.

Other than that, secured cards function like normal credit cards. Some card providers even offer perks on secured cards such as cash back. At the end of each billing cycle, you can choose to pay off the card balance in full or only make the minimum payment and pay interest on the balance.

When your credit score gets to the point where you can qualify for a non-secured card, some card providers will allow you to upgrade to a standard card with a higher limit and more perks.

Become an Authorized User on Someone Else's Card

If you have someone in a trusted relationship with a good history and a credit card, you may consider becoming an authorized user on their card. An authorized user is given their own copy of the primary user’s card, using the same credit card number and account. You can then make purchases on the card, which contributes to the card’s overall balance and rewards accumulation.

When you become an authorized user, the payment history on the card is added to your credit reporting, meaning you can start out with a long, positive history contributing to your score.

The primary cardholder on the card is legally responsible for the payments, though authorized users can choose to do so if they wish. If the primary holder misses a payment, it will reflect negatively on both your scores. On the flip side, if the authorized user makes purchases on the card, they aren’t legally on the hook for payments if the primary user defaults.

If the primary user is concerned about the authorized user making purchases, or simply wants to build their credit history, they can choose to grant the authorized user access through the card holder, and simply not give them the card for use.

Get a Credit Builder Loan

Credit builder loans are small loans, typically ranging from $300 to $5,000, offered exclusively for the purpose of building credit. The lender will deposit the loan amount into a set savings account or a certificate of deposit. The borrower will make the monthly principal and interest payments over a period of three months to two years, depending on the loan terms. Once the loan is paid off, the funds are released and given to the borrower, sometimes with some of the interest compensated.

If you can afford to make the monthly payments, a credit builder loan can be a good entry-level way to build credit or to diversify your credit mix alongside a secured card. While you will pay interest, you’ll receive the principal at the end of the loan, which can be an indirect way to save while building credit.

Report Your Rent and Utility Payments

If you’ve been paying rent or utilities for a few months or longer, you can choose to report your payments to the credit bureaus, which will count toward your payment history. You will need to sign up for a third-party service that collects your history and reports them to the credit bureaus. While some offer this for free, others require a monthly subscription.

Services and payments you can count include:

- Water service

- Oil or gas service

- Electricity and solar services

- Rent payments

- Internet, phone, and cable

- Town or municipal services such as trash pickup

- Streaming services

Keep in mind that only formal payments made in your name will count. If you split utilities with roommates, where one person makes the payment and splits the costs informally with others, then it can’t be counted. Small-time landlord payments, as opposed to formal payments to an apartment complex or corporate landlord, can also be difficult to count.

Apply for a Student Credit Card (If You're In College)

If you’re a student enrolled in an accredited school and have a source of income, you can qualify for a student card. Student credit cards are geared toward students with low or no credit history, and often come with perks geared toward students such as cash back for school expenses or bonuses for good grades. Once you graduate, if you’re in good standing, many card servicers will upgrade you to a standard card.

While you will need to report a source of income, even having a part-time job will typically qualify you. Card limits tend to be low and interest rates tend to be on the higher end, so be sure to stay on top of your spending and monthly payments.

Apply For a Store or Retail Card

If you shop frequently at a certain retailer, you might want to consider signing up for a store card. Store cards often have low or no credit requirements, and can come with quick approval, with many retailers offering applications at checkout or customer service.

Store cards also come with discounts and perks for shoppers, offering a way to save money at retail locations you often shop at. However, credit limits tend to be low, and interest rates tend to be high, so making payments on time, watching your spending, and paying off the full balance is imperative to saving money.

Ask a Cosigner to Help You Qualify

If you’re taking out a loan and you lack a score to qualify, you can ask someone to co-sign on the loan with you. While you are responsible for the payments, a co-signer promises to pay back the balance of the loan if you default. The lender will assess the co-signer’s credit score and history in order to approve you for the loan, so you’ll need a co-signer who meets the credit requirements.

This method can be risky, as the co-signer is liable for the loan should you default. However, it can help you establish your history as you make on-time payments on the loan and allow you to borrow when you otherwise wouldn’t qualify.

Explore Alternative Credit Data and BNPL Reporting

Some forms of borrowing and payment history can be used to either build your credit score or qualify you for a loan that would otherwise require a credit score.

For example, if you’ve used Buy Now Pay Later (BNPL) in the past, BNPL servicers are now reporting payment and balance data to the credit bureaus. If you’ve made on-time payments in the past, it will help you boost your score.

Alternatively, if you’re trying to qualify for a loan or card to get you started, and don’t have a credit score, you can request the lender assess alternative credit data. In this case, you would provide information such as payment history for services, employment data, and income through gig assignments or business revenue. This can take longer than qualifying through a traditional credit score, and may come with extra fees, but it can otherwise open up borrowing opportunities that can help you establish and boost your score later down the line.

The Step-by-Step Plan to Build Credit From Scratch

Ready to get a credit score? Here’s how you can start.

Choose One Starter Path

Choose which one of the methods above you want to start building credit with. While it might be tempting to use multiple methods at once, start out with just one so you can focus on your payments and balance and avoid having too many hard inquiries build up on your account.

Once your score becomes established after a few months, you can start diversifying your credit mix.

Open an Account That Reports

Once you’ve chosen your starter method, go ahead and open your account. No matter which method you choose, you will need either your Social Security Number or your Individual Taxpayer Identification Number ready.

When you apply, keep these things in mind.

- Understand the terms and conditions. Look at the interest rate, understand your monthly payments, and be aware of what your responsibilities are for the monthly payment and when it’s due.

- Be aware of the credit limit on your card. Starter cards will have a low limit, so track your spending and make sure you don’t go over it.

- For cards, start small. If you prefer to stick to a debit card or cash for payments, you can keep your card open by putting a monthly subscription on it.

- If co-signing or becoming an authorized user, set clear expectations. Discuss if they trust you with a card, what your individual limits are, if they expect you to contribute to payments, and what you will do if you can’t make a payment.

Automate On-Time Payments

Making your payments on time is the biggest factor contributing to your credit score. Automating your payments will help you pay off your balance in the background and ensure you don’t miss a payment.

If you’re using a card, be sure to pay off the balance in full each month, which will help you avoid paying interest. Contrary to popular belief, you do not need to carry a balance on your card to have a credit score — you just need to keep the card open.

Keep Utilization Low

Credit utilization is the second-largest factor in your score’s calculation. You should keep our utilization below 30%, though 10% is ideal in terms of optimizing the impact to your score. As such, be sure to stay well within your card’s limit. For most card providers, you can set custom alerts on your card if your utilization goes over a certain amount.

Limit New Applications

Even as your score improves, don’t start applying for new credit products too quickly, since too many hard inquiries can sink your score. For a newer score, it’s a good idea to wait at least six to twelve months before applying for a new credit card or loan, and then space out any new applications by at least six months.

Monitor Reports and Dispute Errors

Keep an eye on your credit score and reports to make sure your credit history is going in the right direction. You can request free reports once a year from each of the three credit bureaus, and monitor your score through financial services such as your bank account.

If you see an entry made in error, such as a payment you made on time that is marked as late, you can dispute the error through any of the three bureaus. If you can provide proof that the entry is not correct, it will be removed from your report.

5 New Credit Mistakes to Watch Out For

Beware of these new credit pitfalls, which can pull down your score quickly.

- Applying for too many cards at once. Hard inquiries can stack quickly, and if you have a thin credit file, you could see a major impact on your score. Pace out new applications to six months apart or more.

- Carrying a balance "to build credit.” This is a persistent myth. You don’t need to carry a balance on your card, and, in fact, it’s a better idea to pay it off in full each month to keep your utilization ratio low and save on interest.

- Closing your oldest account. Old accounts are your friend, since they count toward your average account age and available credit, and include the positive payment history on your report. You can keep old cards open by leaving a subscription or recurring expense on them and auto-paying them each month.

- Maxing out your first card. Since starter cards have low limits, it can be easy to max one out. However, pushing your utilization ratio to 20% or higher will seriously bring down your score. Keep your utilization low, and set alerts for going over a certain balance threshold.

- Ignoring your credit report. Your credit report offers you a crucial window into your payment history and accounts. If you’ve missed a payment, have had an account opened without your authorization, or if there’s an error on your report, you’ll want to catch it as soon as possible.

Building Credit in Specific Situations

Different circumstances call for different approaches. Here’s how you can build a credit score whether you’re a student, newly moved to the United States, or are working with a tight budget.

How to Build Credit at 18 With No History

If you’re starting out at 18 and have no credit history, you have a few options for building credit quickly.

- Start with a secured card. Secured cards offer easy entry into the credit world, and usually only require a small deposit and a verified source of income.

- Take out a credit-builder loan. Credit builder loans don’t have minimum credit requirements, and usually have fairly affordable monthly payments.

- Become an authorized user. You can ask a family member if you can become an authorized user on their card, which will link the payment history on the card to your credit report. You don’t even have to use the card.

How to Build Credit as a Student

Building credit while you’re in school comes with a few advantages. Firstly, you have access to a few unique options for building your credit score. Secondly, building your score as a student will set you up for success when you graduate, as it can help you be approved for your first apartment or utility service more easily.

- Get a student card and pay it off on time. Student cards often have low or no credit requirements as long as you’re enrolled. Just make sure to make the payments on time, and avoid carrying a balance so you don’t have to pay interest.

- Become an authorized user on a card. Ask someone who trusts you, such as a parent or guardian, if you can become an authorized user on their card. You don’t even need to be given a card.

- Start making payments on your student loans early. While you don’t have to officially make payments until after you graduate or unenroll, you can start making payments toward your loans while you’re in school. Even making small payments of $10 or $20 toward your balance can count toward your positive history.

How to Build Credit as an Immigrant (With or Without a SSN)

If you are an immigrant, international student, or living temporarily in the United States, it is possible to build a credit score. Keep in mind that credit history only counts for accounts and cards based in the United States. If you have an international loan or credit account, it won’t count toward your history, but it may count toward your overall financial profile and utilization ratio.

With a Social Security Number

If you have or are eligible for a Social Security Number, (SSN) most starter options are available to you for building credit. Some may require residency for a certain length of time, or only be available for U.S. citizens, so be sure to read the terms and conditions.

Without a Social Security Number

If you don’t have a Social Security Number, you may qualify for an Individual Taxpayer Identification Number (ITIN). These are offered to eligible non-resident and resident aliens that do not otherwise qualify for an SSN, and can be used in lieu of an SSN when applying for credit or loan products and when establishing your credit score.

How to Build Credit on a Tight Budget

Building credit when your budget is highly limited is entirely possible, and, in fact, having a strict budget can help you prioritize timely payments and manage your spending.

- Focus on methods with small payments. A starter credit card with a small deposit or a small credit-builder loan will keep your monthly payments affordable.

- Make payments a part of your budget. Keep your payments fixed, either by using a fixed installment loan, or keeping a strict cap on spending on your card.

- Report your existing utility and service payments. You can do so through a third-party service, or through services offered by each of the three credit bureaus.

- Have an emergency fund in place. If you don’t have a fund in place, focus on building up $1,000 in savings or one month in net income (whichever is higher) so you have a backup if you’re in danger of missing a payment.

How to Build Credit as a Couple

Building credit as a couple is crucial for your long-term financial health with your partner, especially if you plan on taking out a loan or mortgage together in the future.

- Become an authorized user on your partner’s card (or vice versa). If you have a high degree of trust with one another, becoming an authorized user on a partner’s card that has an established history can boost your score. As a bonus, it can be a way to share expenses without having to share a bank account.

- Become co-borrowers. Similar to the authorized user trick, co-signing or co-borrowing can help you boost your history with on-time payments.

- Hold each other accountable for making payments on time. Be transparent with one another about your card and loan balances and payments. Create a budget, and hold regular money dates and check-ins to ensure you’re not missing anything.

How Monarch Helps You Build Credit From Scratch

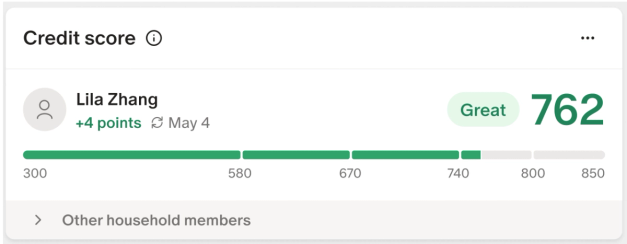

Financial management and building your credit score go hand-in-hand. Monarch can help you track your credit score as it develops, manage your credit accounts, and get a full picture of your borrowing and payment activity and how it fits into your overall financial plan.

Keeping an eye on your score is essential to staying on top of your credit history — and, when you watch your score rise, you’ll be more motivated to stay on course with your credit building plan. You can track your VantageScore credit score in Monarch’s dashboard, with updates and score movements from week to week.

Managing your balances is crucial to keeping your utilization low, especially in the early days of credit building. When you link your accounts in Monarch, you can see your card balances and utilizations at a glance and set alerts for when your balance goes over a certain threshold.

Payment history is also key to keeping your score up. You can sync your bills and payments to Monarch so you can factor your payments into your overall budget, and set reminders for yourself so that you never miss a payment. You can track recurring payments in calendar view, and get a bird’s-eye perspective of when your payments are due.

If you’ve taken out a credit builder loan, you can track your progress through Monarch’s Debt Dashboard, which tracks your payments and helps you visualize your balance shrinking in real time.

Crucial to keeping your score growing is building credit resilience. Monarch helps you build a budget that fits your lifestyle and that builds your financial scaffolding over time, from helping you save up for long-term goals such as an emergency fund, to budgeting for your monthly payments so that you have enough funds for everything.

While you watch your credit score grow, Monarch helps you grow in the big picture, from helping you track your goal progress, to helping you build a long-term financial plan that works for you.

FAQs

What credit score do you start with?

Before you open a line of credit or start making payments on a loan, you will have no credit score, which is not the same as zero. When you do open a line of credit or take out a loan, your score will depend on how you begin your credit history. In general, it will fall somewhere between 300 and 850 for the FICO model, and will depend on your first few months’ of payment history, number of accounts, and credit utilization.

How long does it take to build credit from nothing?

From the first loan or line of credit you take out, your credit score will take about one to six months to be calculated by the credit bureaus. From there, it can take one to two years with positive payment history, a good credit mix, and low utilization ratios in order to get a high score.

Can you build credit without a credit card?

You can build credit without a credit card by taking out a loan or a line of credit. Some reporting agencies have now begun to accept utility and rental payments toward your payment history as well.

Is it possible to have a credit score of zero?

No. The lowest your credit score can go is 300.

Does checking your credit score hurt it?

Not necessarily. Looking up your credit score online through your bank, credit card, or financial service provider for the sake of seeing your score will not hurt it, nor will requesting your annual free copy of your credit report or score through any of the credit bureaus. What will hurt your score is when a lender performs a hard inquiry, which is a formal request of your credit score for the purpose of approving you for a loan or card. When this happens, you will need to sign consent and be informed of the inquiry before it can be performed.

What is a good credit score?

Technically, a “good” credit score is 670 to 739 for a FICO score, and 661 to 780 for a VantageScore (which is called “Prime”) while a “good” credit score does qualify for most lending products, a FICO score of 740 or higher (“Very Good” to “Exceptional”) or 781 and above for a VantageScore (“Super Prime”) will get you better interest rates and more exclusive credit products.

Can I build credit with a debit card?

You cannot build a credit score with a debit card. Credit scores are based on your borrowing history, which means you will usually have to take out a loan, line of credit, or credit card to start building a history.

What is the fastest way to build credit?

If you’re starting from scratch, you can build credit quickly by taking out a secured or starter card or taking out a credit-builder loan and making payments on time and consistently. If you have someone you can trust, you can ask if you can be made an authorized user on their credit card, which will put their positive payment history on your credit report. You don’t even have to use the card. Just be sure that they make payments on time and are comfortable with having you as a user on their card.