When it comes to paying for your day-to-day expenses, how you do it has a surprising effect on your financial picture as a whole. With three in four Americans owning a credit card, cashless transactions have transformed how people manage their spending

While plastic is popular, cash still has an important place in your wallet, whether you’re paying for a candy bar from a vending machine or using cash envelopes for your budget. Both have their advantages and their disadvantages, so here’s how to find the best option for you.

The Science of Spending: Why Your Payment Method Matters More Than You Think

How you physically see and handle your money has a surprising effect on your spending. Particularly, credit cards tend to be linked to overspending, with 58% of consumers in a Forbes Advisor survey saying they were more likely to overspend when using a credit card instead of cash. In the same survey, it was found that using a card doubles your chance of making an impulse purchase.

The reasons come down to how our brains process spending differently depending on the payment method. While cash requires you to physically hand over something, using a credit card literally lights up the reward center of your brain, according to research by the MIT Sloan School of Management.

Swiping or tapping a card, especially if it has a nice design or is made of heavy material, feels more pleasurable when linked to purchasing items or services, while decoupling it from the “pain” of watching your money leave your hand.

On the other hand, many consumers use cash to “forget” the purchases they made, or to make purchases not accounted for in their overall budget, like impulse buys, according to a study by researchers at the University of Notre Dame. Cash’s limitations and lack of traceability can make it an ideal way to both fund purchases you don’t need (or want) to track, while keeping limits on your spending.

Card purchases, on the other hand, are easier to track, especially if you review your transactions on a regular basis or automatically link them to your budgeting method.

While cards can offer advantages in tracking and analyzing your spending after the fact, cash can help you put a physical limit on your purchases. Of course, it’s entirely possible to use a card and manage your spending, or to go over budget even when using cash.

Finding a balance between the two by understanding your own habits, and using tools to help you manage your spending no matter which method you choose, is key to sticking to your budget and overall financial plan.

Cash vs. Credit Card at a Glance

Here’s a quick overview of how spending with cash and cards compares.

Credit Cards | Cash | Debit Cards | |

Rewards and Perks | Robust rewards with cash back, points, perks, and more | None | Some banks may offer cashback perks, but otherwise limited |

Fraud Protection | Robust fraud protection in the form of fraud flagging and chargebacks | None. If you lose it, you lose it. | Banks can flag or halt suspicious activity, but may not be able to reverse charges |

Spending Control | Limited. Cards can encourage you to overspend, especially if your limit is higher than your savings | You’re physically limited by how much cash you have on hand | Limited. While you’re capped by how much you have in your bank account, you can still be tempted to overspend |

Credit Building | Payments, account ages, and low utilization contribute to credit score | None | None |

Fees | May incur a 1% to 3% surcharge | None | May incur a 1% to 3% surcharge |

Convenience | Useful for digital and in-person purchases, though not all places and people accept them | Nearly every in-person merchant/business will accept, though digital options are limited | Useful for digital and in-person purchases, though not all places and people accept them |

Budgeting | Transactions can be linked to budgeting apps and platforms for easy tracking, with servicers offering tracking tools | Transactions have to be tracked manually | Transactions can be linked to budgeting apps and platforms for easy tracking |

Purchase Protection | Robust, with chargebacks and fraud flagging available | Practically none | Limited; while banks can intercede, it is often treated as cash if lost |

Privacy | Transactions can be tracked by your servicer and government agencies | Limited tracking | Transactions can be tracked by your bank and government agencies |

Acceptance | Accepted at most major retailers, though limits come with card servicers and cash-only merchants | Accepted nearly everywhere, though you’ll need to convert in foreign countries | Accepted at most major retailers, though limits come with card servicers and cash-only merchants |

Travel | Useful for travel perks and protections, and required for hotel and rental equipment | Useful for cash-heavy countries and avoiding fees, though you will need to convert | Limited travel application, as hotels and rental places may not accept these |

Interest | Can incur high amounts of interest on balances not paid off, to the tune of 20% APR or more | None | None |

When Credit Cards Make More Sense

Credit cards come with a variety of advantages, depending on how you use them. From rewards to your credit score, here’s when a credit card is most useful.

Earning Rewards and Cash Back

One of the biggest perks of credit cards is the rewards on purchases. Card rewards can include cash back and point rewards that can be redeemed for gift cards, flights, travel packages, and otherwise.

While it may seem small, rewards can stack up over time. If you spend an average of $5,000 per month, 1% in rewards over a year adds up to $600. Many cards will offer promotional rates for spending at certain vendors.

Card perks go beyond earning rewards. Many cards offer access to airport lounges, free upgrades at restaurants and airlines and credits for subscription services, especially if you’re a loyal customer or have paid for a trip using points.

Chargebacks

If someone makes a fraudulent transaction on your credit card, or if you purchase a good or service on your card that didn’t turn out as advertised, you can file a chargeback. Chargebacks are disputes on charges filed by the cardholder that reverse the charges on a card. While a business or merchant can dispute a chargeback, if the card servicer deems it legitimate, then the charge is removed from the cardholder’s balance.

Chargebacks are easier to initiate on a credit card than a debit card, since the card servicer is technically the owner of the credit card debt and thus is incentivized to resolve the dispute under the Fair Credit Billing Act (FCBA).

With cash or a debit card, most of the time, you’re solely responsible for your own funds, so chargebacks are more difficult to see through.

Keep in mind that chargebacks shouldn’t be used lightly. If you initiate a chargeback on a business, it’s likely they’ll blacklist you from their services permanently, even if the chargeback doesn’t succeed. If you initiate too many chargebacks, your card provider may choose to close your account.

Fraud Protection

In addition to chargebacks, credit cards protect you from fraud in a couple of unique ways. Many card providers have built-in fraud protection that alerts you if your card has suspicious activity on it, such as a large purchase out-of-state, and can even block flagged transactions. You can set custom alerts for transactions that go over a certain amount, and freeze your card through your account if it gets lost or stolen.

Building Your Credit Score

Credit cards are a great way to build your credit score, since you can keep the account open indefinitely, unlike an installment loan, which can really boost the average age of your account. Contrary to popular belief, you don’t have to keep a balance on your credit card to build or maintain your score, which means you can build your score without incurring any interest if you pay off the balance in full.

Large Purchases and Emergencies

Using a credit card can be a secure way to make a large purchase, as it’s safer to carry around a card instead of a large amount of cash. Large purchases on a card can clear more quickly than using a check, and offer more fraud protection than using a wire transaction or cash.

A card can also be useful in emergency situations, if you use it wisely. If you need to cover a large expense immediately and don’t have cash up front, a credit card can help fill the gaps until you are able to withdraw your emergency fund or until the next paycheck hits.

Be careful, however, that you don’t use your credit card as your only emergency fund. Credit card interest falls between 21% and 24% on average, which means that credit card debt can quickly balloon if you don’t manage it.

Online Shopping

Credit cards are ideal for digital transactions, since they’re more secure than directly linking your bank account.

Travel

Credit cards are useful for travel because of their security. On top of protections for lost or stolen cards and fraudulent transactions, many cards will waive foreign transaction fees as a perk. Certain card types, like Visa and MasterCard, are widely accepted at any locations that have a card reader.

Beyond their accessibility, cards can be mandatory for certain services. Renting a car or a hotel room often requires you to use a credit card instead of a debit card or cash, as the rental or lodging company will put a temporary hold on your card that can be used to cover any damages incurred during the service period.

Moreover, booking with a travel card can offer you additional protections. Many cards offer trip insurance if you book through the provider’s travel platform, which compensates you for costs incurred due to trip delays or cancellations. If you rent a car, some cards offer secondary insurance, which can help to cover costs for damages your primary insurance doesn’t cover.

Budgeting and Tracking Tools

Using a credit card is ideal if you want to track every purchase you make without having to do so manually. You can see all of your transactions, the date they were made on, and the merchant they were made with at a glance through your card account, and easily link those transactions to financial management services like Monarch, or to accounting software.

Many card providers also offer basic budgeting tools that allow you to see how much you’re spending on a given category each month and show your month-to-month spending activity.

Sharing Expenses

If you’re splitting expenses with a partner, credit cards can offer a way to manage a shared expense account, often without the need for a shared savings account. Many couples will use the same credit card account, often by making one partner the owner and the other authorized user, in order to help their partners build their credit score, earn rewards more efficiently, and track expenses together.

Paying Off Your Balance in Full

Credit cards ultimately work best when you are able to pay off your balance in full each month, allowing you to avoid hefty credit card debt that can quickly grow out of control because of high, compounding interest. By not spending more than you can comfortably pay off at the end of the statement period, you’ll reap the benefits of credit cards and avoid the high costs that can come with leaving your balance on month-to-month.

When Cash is the Better Choice

Cash has its own unique advantages, whether you’re paying for small purchases or trying to cap your spending. Here’s when cash can work better for you.

Controlling Discretionary Spending

Cash has hard limits, which can come in handy if you want to keep a cap on your spending. This can be useful both for your long-term budget and for managing day-to-day spending. If you have a certain amount budgeted for grocery shopping, for example, you can carry only as much cash as you have budgeted when you go to the store, forcing you to stick to your limit.

Small Purchases and Cash-Only Businesses

Cash, as the saying goes, is king. Since cash doesn’t come with transaction fees or require special equipment to handle, it’s accepted at most businesses, whether it’s a gas station, a farmer’s market stall, or a food truck. It’s also handy for transactions below five dollars, especially if a business has a card minimum or imposes fees on card payments. Some businesses will even offer a discount or fee waiver for cash purchases.

Avoiding Interest and Fees

Unlike cards, cash doesn’t come with interest and fees. Many businesses will charge 1% to 3% of your final bill for credit card purchases to cover for transaction fees if you use a card, which can add up quickly, especially on large purchases. Paying with cash will help you avoid these fees.

Sticking with cash also lets you avoid one of the biggest downsides to using a credit card: Interest. With credit card APRs reaching easily over 20%, avoiding having a month-to-month balance will save you greatly in the long run.

The Cash Envelope Budgeting Method

Cash is key to the cash envelope budgeting method, which entails putting cash in “envelopes” that categorize your spending. One envelope can have cash for groceries, while another has cash for the housing payment, and so on.

If the cash in the envelope is spent, it’s done for the month, setting a hard limit on how much you can spend. Money left over at the end of the month can be distributed to other envelopes, put into savings, used for discretionary purchases, or rolled into next month’s budget.

Cash vs. Credit by the Numbers

With digitalization, more access to remote transactions, and the convenience of cashless transactions, the relationship with how Americans spend and how they choose to pay has evolved over the last decade. Here are some of the core numbers behind the way consumers choose to pay.

- Cards are king in terms of transaction volume. In 2024, credit cards were the top choice for consumers to make purchases with, accounting for 35% of all payments, followed by 30% by debit card and 14% by cash, according to the Federal Reserve’s 2025 Diary of Consumer Choice.

- Card transactions are going up, and cash is going down. In 2016, 18% of transactions were made with card, and 31% with cash. In 2024, card transactions increased by 17 percentage points, while cash transactions decreased by 17 percentage points, according to the Federal Reserve.

- Consumers overwhelmingly prefer cards, as 82% of consumers said they prefer credit cards, with only 5% stating they preferred cash, according to the Federal Reserve.

- Cash is the primary backup for card-users. Over one in four (29%) of consumers who used cash for a transaction said they prefer using a credit card, according to the Federal Reserve.

- Households with lower income prefer cash more. Households making below $25,000 a year made 24% of their purchases with cash. On the other end of the spectrum, households making $150,000 a year or more use credit cards for 51% of their transactions, according to the Federal Reserve.

- Despite the popularity of credit cards, cash isn’t going anywhere. Nine out of ten (92%) of all consumers said they intend to use cash in the future, and 80% had cash in their wallets at least one day of the year, according to the Federal Reserve.

- Credit card users primarily use cards for rewards, safety, and borrowing. According to a Forbes survey, 35% of cardholders used cards to take advantage of rewards, while 33% said they used cards for the security they provided. Over one in four (28%) used them to cover expenses they could not afford.

- Nearly half of cardholders carry a balance month to month. According to a Bankrate survey, 47% of cardholders have a balance from the previous month, with 41% of those carrying a balance stating it came from an emergency expense.

- The average credit card balance in 2025 was $6,735, according to Experian. The average credit card interest rate was 21.22%, according to the Federal Reserve.

Find Your Approach: The Cash vs. Credit Decision Framework

Deciding whether to use cash or credit isn’t a strictly binary decision. There are certain situations where using one over the other will be more advantageous. While the decision is ultimately up to you, here’s a general framework for when you should use cash over a card.

If you want to… | …you should use... | …because |

Keep a transaction secure | Credit card | Credit cards come with more robust protections, like chargebacks and fraud detection. |

Make a transaction untraceable | Cash | Cash generally can’t be traced back to the owner. |

Make a digital/online transaction | Credit card | Cards are usually required to make digital or remote purchases, and usually work faster than mailing a check or wiring funds. |

Take advantage of rewards | Credit card | Credit cards come with perks and rewards for your transactions. |

Make a large transaction | Credit card | Not only do big purchases come with more rewards, but it can be safer to carry around a card than a large amount of cash. |

Avoid fees | Cash | Businesses will waive card fees or offer discounts if you use cash. |

Keep a cap on your spending | Cash | Since you’re physically limited by cash, it can be a good way to keep strictly to your budget. |

Make a small transaction under $5 | Cash | Many stores have minimums on card purchases, or else charge a card fee. |

Easily keep track of your expenditures | Credit card | Credit cards digitally track every penny you spend, making it easy to plug into a budgeting platform and keep an eye on your spending |

Avoid fees and interest | Cash | Cash almost never comes with fees, and does not incur an interest-accumulating balance. |

Build your credit score | Credit card | Your credit card payment history and utilization ratio contributes to your credit report. |

Travel abroad | Credit card | While cash is useful if you’re sightseeing in a place with cash businesses, you should use a card for all other purchases, both to rack up points and to protect yourself from fraud and card skimmers. |

How to Make Both Strategies Work

Taking a hybrid approach to cash and credit cards can offer you the advantages of both methods. Here are a few ways you can do it.

Treating Your Credit Card as Cash

If you want to use a credit card but don’t want to run the risk of overspending, there are a few ways you can configure your card settings so you don’t run into the temptation to overspend or rack up interest on your balance.

- Pay your card in full each month. This way, you won’t have a balance that accumulates interest.

- Set alerts when you go over a certain spending threshold. You can set your card to send you push notifications and text alerts when transactions go over a set amount, or if your balance hits a certain threshold, helping you keep track.

- Set a card lock on certain transactions. Some cards will allow you to block purchases made in certain geographic areas or through certain merchants, which can be helpful if you’re trying to limit impulse purchases.

- Request a low credit limit. If you’re truly worried about overspending, you can request your card servicer lower your credit limit to what you can afford to pay off each month. Keep in mind that this has the potential to heavily impact your utilization ratio, which can tank your credit score.

Use Cash Where You Want Limits

If you find yourself tempted to overspend in certain situations, such as eating out, window shopping, or attending an event, leave your card at home and instead give yourself a set amount of “pocket money.”

For example, if you’re planning on doing your holiday shopping and have a set budget in mind, head to the mall or the holiday fair with your budgeted cash in hand. This way, you have a hard limit that you have to contend with and work around, and won’t slip into the pattern of “just a few dollars more” that may come from using a card.

Limit Certain Transactions to Your Card and Use Cash for the Rest

This method works well if you want to take advantage of certain rewards but don’t want to use a credit card as your primary method of payment. In this case, you would open a card with a specific reward set, such as bonuses for travel, discounts at a retailer you frequent, a high cash back percentage, or a generous sign-on bonus.

Then, limit transactions on the card to specific, pre-determined purchases that you can afford in your budget and pay off in full. These can include:

- Buying expensive appliances like a washer or dryer

- Paying for travel expenses

- Covering for event expenses

- Funding a home improvement project

With this approach, you can reap the benefits of rewards while still limiting and protecting your purchases. The key thing with this method is that you need to be able to pay off the balance in full – otherwise, you’ll be paying a high interest rate on the balance.

Credit Building With a Card in the Background

If you want to avoid the temptation to overspend, or simply prefer cash, you can still build your credit score in the background with a card. Simply put a small recurring purchase on the card, such as a subscription, insurance payment, or utility bill, and set it on autopay from your bank account.

This way you avoid accumulating a balance, keep your utilization ratio low, and build a positive payment history while still using cash.

Tracking Both Cash and Credit in One Place

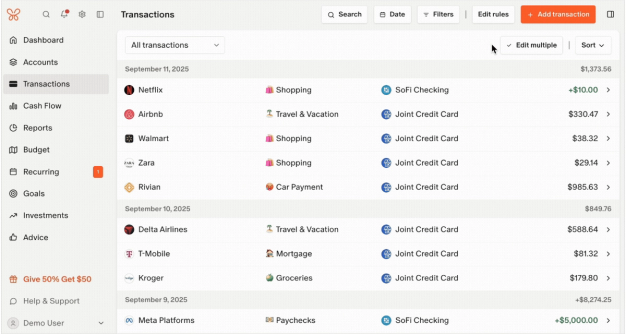

When it comes to using both cash and cards, it’s important not to miss out on the details for your spending when it comes to managing your budget. You can enjoy the benefits of both cards and cash, while avoiding spending more than you can pay off on your card, or losing track of your transactions with cash. Here’s how you can manage both types of transactions in Monarch.

Tracking credit card spending is essential to keeping your balance in check. With credit card transactions, it’s pretty straightforward: Simply link your card info to Monarch, and watch your transactions populate your budget.

This helps you overcome one of the downsides of using a card: Overspending. You can keep an eye on your utilization and spending balances all in one place and integrate your card transactions into your budget, allowing you to stick to your limits and get alerted if you are approaching your limit, helping you avoid impulse purchases and going over your budget.

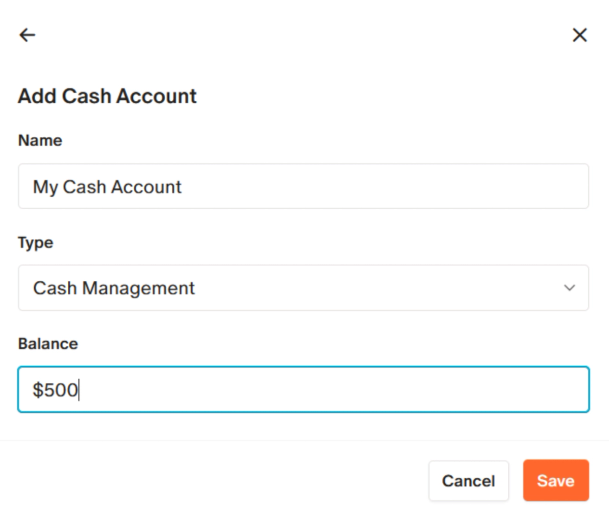

Monarch also makes tracking with cash easier on the go, so you don’t have to be in the dark about your cash flow and expenditures, even when you’re on the go.

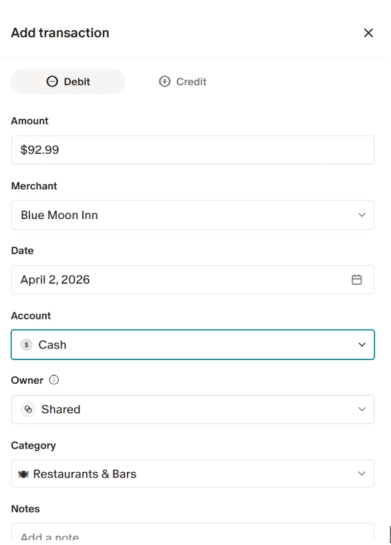

With a Cash account in Monarch, you can link your transactions to your cash balance and get an at-a-glance view of where your spending and balances are.

You can then add or subtract from the balance using manual transactions. You can add details like the date, merchant, amount spent, and other notes, giving you as much insight as a card transaction.

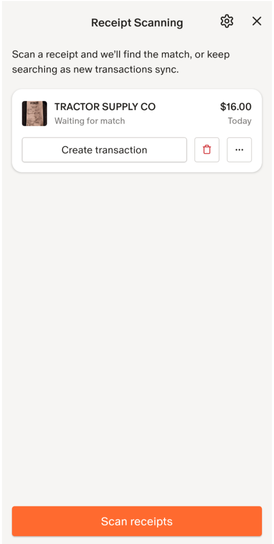

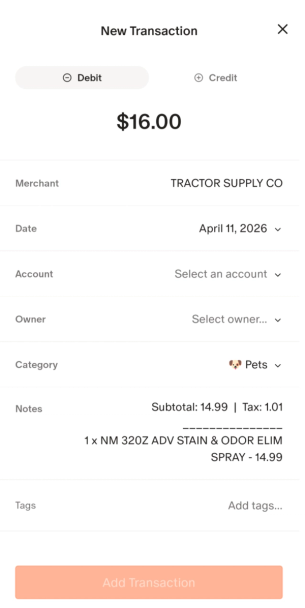

Monarch’s receipt scan feature makes it even easier to import information from digital receipts, screenshots, or images you take with your phone. You can take a picture of your receipt or upload a photo from your phone gallery.

From there, Monarch will import the merchant, the transaction amount, the transaction date, and any relevant notes, automatically categorizing it based on the rules you’ve set. You can then link the transaction to your cash account, and treat it like a card transaction.

You can add and access your transactions wherever you have an internet connection with the Monarch mobile app, making it easy to keep track of your budgeting wherever you go and no matter what payment method you use.

What About Debit Cards?

Debit cards offer a bit of the best of both worlds, with the physical limitations of cash and some of the convenience of cards. A debit card allows you to make purchases with the funds in a checking account you have through a bank, which adds the hard limits of cash to the convenience of a card. There are risks, however: Since a debit card is a direct link to your checking account, it means you (or potential fraudsters) have direct access to your money.

That said, a debit card can offer a nice combination of convenience and financial limits. Here are the pros and cons to consider.

Pros:

- A debit card comes with a hard limit. If you try to spend more than your account balance, your card will be declined unless you have overdraft service.

- Debit cards offer all the digital convenience of a credit card. You can make purchases online or swipe or tap your card at a register just like a credit card.

- You don’t need a credit check to get a debit card. Most banks will offer a free debit card with a checking account.

- More security than cash. You can freeze your card if it gets lost or stolen, and your PIN adds an extra layer of protection that cash doesn’t offer.

- You can track your purchases. Like credit cards, your debit card purchases can be tracked and viewed through your account, and linked to your budget platform.

- You can draw cash without fees. Many credit cards will charge a fee if you use them to withdraw cash. Debit cards, however, don’t have a cash advance fee (though you may be charged an ATM fee).

- No interest or debt. Since you can’t spend more than you have, you don't run the risk of high-interest credit card debt.

Cons:

- Purchases are treated as cash when it comes to fraud protection. Chargebacks are more difficult to file with a debit card, and you’ll have a harder time getting your funds back.

- You could be charged overdraft fees. If you opt for overdraft service, the bank will charge you a fee between $30 to $40 for each overdraft if your account goes into the negative.

- They don’t come with rewards. While some cards may offer a small cash back bonus, debit cards generally don’t offer any spending rewards at all.

- Travel protections and perks are limited. Some debit cards come with international charges if you use them abroad, and they usually don’t offer lounge access or upgrades.

- You generally can’t use them to book hotels or rent cars. Most rental agencies or lodging services will require you to have a credit card on file.

- It’s less secure. Carrying a debit card can be like carrying your entire checking account balance in your pocket, which makes it a risk if it gets stolen.

- You won’t get any boosts to your credit score. Since your credit score draws on data from credit lines and loans, if you only have a debit card, you will have no credit history, which makes borrowing harder.

- It has the same abstract spending issues as a credit card. If you have a problem with overspending with a credit card, a debit card may pose the same problem, since you may not have a mental picture of how much you’re spending.

FAQs

Is it better to pay with cash or credit card?

That depends on your circumstances. Credit cards are more useful when you want to protect a purchase from fraud, take advantage of card rewards, or if you’re making online purchases. Cash, on the other hand, comes with no transaction fees, is untraceable, and can help limit your spending more than cards.

Do you spend more with credit cards?

Statistically, yes. Using cards has been linked to overspending, according to the Forbes Advisor survey, with 58% of consumers saying they were more likely to overspend when using a credit card instead of cash. Cards are also more likely to fuel an impulse purchase, according to the same survey.

Should I use cash for groceries?

Cash can be useful if you’re using a strict budget with a set amount you have put aside for groceries. Because of the physical limits of cash, you can avoid overspending on groceries. On the other hand, a credit card can earn you rewards on your grocery spending.

Is paying with cash safer?

Not necessarily. While cash is untraceable, it can be more easily stolen and used than a credit card, and it can be much harder to get a refund on a cash purchase if you lost the funds to a fraudulent transaction.

Does using credit cards help your credit score?

Depending on the usage, yes. Using a credit card, keeping the utilization ratio low, and paying off the balance in full and on time each month will help build your credit score. On the other hand, applying for too many cards at once, maxing out your cards, or missing payments will all hurt your score.

Are credit card rewards worth it?

That depends on your circumstances and spending habits. If you use credit cards wisely and are able to pay off the balance in full each month, they can be worth it for the rewards, trackability, security, and perks they offer. However, if you find yourself regularly accumulating a balance and racking up high-interest debt, a credit card may not be worth it.

What is the cash envelope method?

The cash envelope method is when you allocate a certain amount of cash into envelopes denoting categories of spending, such as Mortgage/Rent, Groceries, Entertainment, and so on. This can be a good way to physically divide up your monthly income and put a hard cap on your spending, since you can’t spend more cash than you have. Any leftover cash is put into savings, put toward discretionary spending, or rolled over into next month’s budget.

How much cash should I carry?

If you use cash primarily, then take as much as you’ll need for a particular expense or outing. If you use cash as a backup, it’s a good idea to have about $100 to $300 on hand, with $500 to $1,000 in a safe or secure place at home in case of emergencies.