A credit score can be a credit to your financial name. It’s a unique snapshot into some of the info on how you handle debt and credit lines, which informs lenders as to how risky they think you might be to lend to. The higher your score, the more attractive you are to a potential lender, and the more loans and cards you’ll qualify for.

Your credit score is calculated using your credit history, which includes your payments, your open credit accounts, your balances, and other important information. How your score is calculated based on these factors will depend on the scoring company, which is why it’s important to know the differences between the two and how lenders use them.

In a nutshell: Your credit score is an important piece in your overall financial picture and future. Monarch can help you understand it, improve it, and take control of it so you can unlock financial opportunities for your life. Here’s how.

What Exactly Is a Credit Score?

A credit score is a bit like a grade on your borrowing and repayment habits. It sums up your credit history, which contains important information about the money you’ve borrowed, how long you’ve been using your credit or loan accounts, how timely you are with your repayments, the types of accounts you have, and if you’ve defaulted on any loans or filed for bankruptcy.

This gives both you and lenders a quick snapshot of how risky you might be to lend to. Your score is calculated based on risk factors that lenders consider when determining whether to lend money to you,.

Lenders typically like having borrowers with a high credit score, since it indicates that they may be good borrowers who pay on time and might be reliable clients. Because of this, lenders will often offer lower interest rates and more competitive repayment terms to borrowers with high scores. Having a high credit score will also make you more likely to be approved for a credit card, loan, or even things like apartment rentals or utilities.

Keep in mind that you need to have at least one US-based credit account open for a certain amount of time in order to have a credit score. If you don’t have any US-based loans or current lines of credit, then you won’t have a credit score in the US at all, which means you likely won’t be approved for any loans or cards.

There are two main kinds of credit scoring models: FICO and VantageScore. While both work similarly, they are calculated a bit differently and are used in different ways by lenders. (We’ll dig into that later.)

Credit Score Ranges – What is a Good Credit Score

Your credit score is a three-digit number ranging from 300 to 850. There are a range of scores to indicate where you stand on the credit scale, which lenders will use as shorthand to advertise products and your eligibility.

FICO and VantageScore both label their ranges a bit differently.

FICO Score Ranges

800 to 850 | Excellent/Exceptional | This is the best score and will get you the most benefits and highest chance of approval score-wise. |

740 to 799 | Very Good | This is a solid score, and comes with a high chance of approval and getting the best or near-best interest rates. |

670 to 739 | Good | You’ll have a good chance of being approved with this score, though you may not get the best interest rates or top-tier credit products. |

580 to 669 | Fair | This generally falls in the minimum for credit scores for most lenders. You may have a harder time getting approved, and won’t get the best interest rates. |

300 to 579 | Poor | Your borrowing options are limited. You’re unlikely to be approved, and you won’t be offered a good interest rate if you are. |

According to Ally, the average FICO credit score is 715, or “Good.”

VantageScore Ranges

VantageScore uses a similar range, though the language around it is a bit different.

781 to 850 | Superprime | The best score range, of which the best lending product and rates are offered. |

661 to 780 | Prime | You’re highly likely to be approved, and will be offered very good interest rates. |

601 to 660 | Near prime | You’ll have more difficulty being approved for lending products, and may not be offered the best rates. |

300 to 600 | Subprime | Your likelihood of being approved is low, and you’ll be offered subpar interest rates. |

According to VantageScore, the average VantageScore is 700.

Why Your Credit Score Matters so Much

Credit scores are more than just a number. They can serve as a snapshot of your overall financial health in terms of your borrowing and repayment habits, which makes them an important tool for lenders and other companies to see how much of a risk you might be.

Having a great credit score can unlock a ton of perks in your financial life, including:

- A better chance at being approved for a loan or refinance. Lenders will more readily approve you if you have a great score.

- Top-tier credit cards. The best credit cards, with access to the biggest rewards, the cushiest perks, and the most exclusive benefits, are reserved for cardholders with top-tier credit scores.

- The best interest rates. Lenders will offer their most competitive rates to borrowers with exceptional scores.

- More flexible repayment options. A great credit score can offer you a bit more leeway with repayments if you need to enter forbearance or pause payments due to hardship, as many lenders will only offer these options to borrowers with a reliable repayment history.

- Better housing options. Many rental companies will consider your credit score when approving you for an apartment or rental home.

- More options for utilities. Some utility companies require a minimum credit score to approve your account. Otherwise, you may have to pay a deposit or secure a letter of guarantee.

- Better insurance premiums. Many insurance companies offer discounts for policy holders with great credit.

- An entire career path. If you work in the financial sector, your employer may pull your credit report to see if you’ve had any bankruptcies or negative marks that makes you risky to trust with money.

How Credit Scores Are Calculated

Your credit score is calculated based on your credit report, which is a summary of information about your credit background. Your credit report is compiled by the three credit bureaus: Equifax, TransUnion, and Experian, all of which submit their information to FICO and VantageScore.

Each of the three bureaus collect similar information, though they differ in what and how they collect data. Both FICO and VantageScore are a summation of these scores, making them a balanced model for credit score reporting. In total, between the three credit bureaus, nine FICO scoring models, and five Vantagescore models, you may have as many as 42 possible scores!

Regardless of bureau and scoring methods, there are five key factors that are considered when calculating your credit score and compiling your credit report.

These are:

Payment history

This is the most heavily weighted across all models. Payment history includes both on-time payments and late or delinquent payments, the latter of which can quickly bring down your score.

Bankruptcies or accounts in collections are also a huge negative factor. Payments that are made on time, however, count positively toward your score.

Balances and Utilization

This looks at how much you owe across your accounts. Utilization ratio, in particular, is a scoring big factor in your revolving credit, which includes credit cards and lines of credit. This tells the bureaus how much of your available credit you are using. For example, if you have a balance of $3,000 on a card with a $5,000 limit, then your utilization ratio is 60%.

A high utilization ratio will count negatively on your score, since regularly charging your credit cards to the limit indicates you may be a risky borrower.

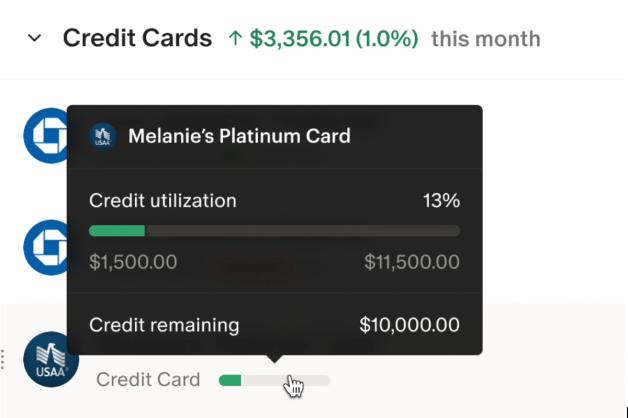

Monarch pro tip: You can track your utilization in Monarch by adding your credit limit to each card account, which will add a utilization tracker to your Accounts page.

Age of Accounts

This is the factor you have the least amount of direct control over. Having a long credit history of many years counts positively toward your credit history, especially if you have multiple accounts that are many years old. Both scoring models will look at the average age of your accounts, as well as the age of your oldest and newest accounts.

New credit/hard Inquiries

When lenders are evaluating your creditworthiness, when you submit an application, they do what’s called a hard credit inquiry. A hard inquiry is when lenders officially check your credit to make a lending decision, which they will ask you to approve of when you submit an application.

A hard inquiry will drop your credit score by a few points for a fairly short period of time. Too many inquiries over several months, however, can stack up and tank your score. The scoring models do offer a grace period, however, for periods when you need to make multiple inquiries, such as shopping for a mortgage. In this case, if you have several inquiries in a certain span of time, they’ll only count as one inquiry.

Credit Mix

Lenders like to see that you have a mix of what’s known as revolving credit and installment loans. Installment loans are traditional loans where you borrow a lump sum and pay a set amount back over time, while revolving credit is when you have a line of credit that you can continuously draw from, like a credit card.

The more diverse your credit mix, the better your score, which is why it’s a good idea to have both installment loans and at least one card.

Monarch pro tip: You can see all of your credit and installment loans in one place with Monarch’s accounts dashboard, giving you an idea of your credit mix at a glance.

FICO vs. VantageScore: Understanding Different Scoring Models

Both your FICO score and your VantageScore will use the key factors of payment history, credit mix, utilization, hard inquiries

Here’s a quick summary of the key differences between the two models.

FICO | VantageScore | |

How it’s calculated | Payments, utilization, average age, credit mix, recent credit | Payments, credit mix, utilization, balances, recent credit, available credit |

Length of time | Minimum account age of six months | Minimum account age of one month |

Weights | Credit mix is weighted less | Credit mix is weighted more |

Late payments | Weighted the same, smaller collection accounts not counted | Late mortgage payments weighted more heavily, all collection accounts counted |

Hard inquiry window | 45-day reporting window | 14-day reporting window |

Popularity | Widely used by lenders and card companies | Not as common for use in lending approval |

Let’s break down the two models in more detail.

FICO

FICO calculations are broken down across the five categories in this way:

- Payment history (35%)

- Utilization (30%)

- Length of credit history (15%)

- New inquiries (10%)

- Credit mix (10%)

There are a few key differences in each category which makes FICO differ from VantageScore.

Firstly, FICO requires you have an account open for at least six months before it can contribute to your score. Secondly, new hard inquiries have a 45-day window of being reported as one in a short span of time, which gives you more wiggle room to shop around for a good rate if you’re applying for loans.

Finally, FICO treats all collections and late payments with the same weight, with no special attention paid to medical collections. However, most FICO scoring models ignore collections bills of less than $100, and the more recent models also ignore debts in collections that have been paid in full.

FICO is by far the most popular score, used by about 95% lenders, so keeping an eye on it will give you the most accurate idea of your approval likelihood when it comes to your score.

VantageScore

VantageScore splits the categories a bit differently than FICO, in this way:

- Payment history (40%)

- Length and mix of credit history (21%)

- Credit utilization (20%)

- Balances (11%)

- New inquiries (5%)

- Available credit (3%)

VantageScore puts a bit more weight on payment history, and puts credit age and mix as second in the order. It also splits your utilization ratio and available credit (or how much of your credit limit you have left in your revolving credit accounts).

You also have a shorter window for rate shopping with VantageScore, as it only bundles hard inquiries made in a 14-day window.

Late payments also tend to be weighted more heavily. All unpaid accounts in collection are counted, regardless of amount, with the exception of medical collection accounts.

Something important to note is that VantageScore is not used as widely as your FICO score by lenders. While your VantageScore will still accurately reflect your credit history, you may not want to use it as a baseline when considering credit score minimums when applying for lending products.

How to Check Your Credit Score (and Report) for Free

Keeping an eye on your credit health is both easy and free, if you know how. Here’s where to go.

Requesting Your Free Credit Report

You can request your credit report for free from each one of the credit bureaus once per week through annualcreditreport.com. Your credit reports will contain a summary of your credit accounts being reported, your payment history, inquiries, bankruptcies, missed payments or bills that have gone into collections, and unpaid child support or alimony.

This can be a good way to monitor your credit and accounts, though it doesn’t always contain your credit score.

Checking Your Credit Score for Free

You can check your credit score by signing up through one of the three credit bureaus, all of which offer free access to your credit score through an app.

Some sites offer free credit score checks in exchange for contact information that their affiliates can use to advertise lending products to you. Many credit card companies and banks also offer credit score reporting through your account. To get all the versions of your FICO scores from all three bureaus, you’ll need to go directly through MyFICO.com and pay for a subscription - there is currently no free way to get all 27 FICO scores elsewhere.

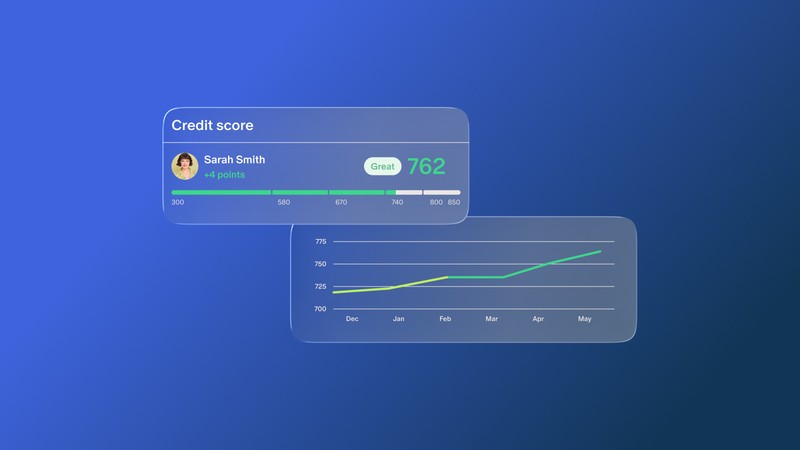

Monarch pro tip: You can check your credit score right on your Monarch dashboard. Simply enable credit score tracking on your dashboard widget, and get your credit score at a glance. FYI, Monarch currently uses the VantageScore 3.0 based on Equifax data.

Is Credit Monitoring Worth it?

Some companies offer what’s known as a credit monitoring service, which alerts you to changes in your credit score and entries on your credit report, such as hard inquiries, missed payments, or new accounts being opened in your name, in exchange for a monthly fee.

For a typical user, you can stay on top of your credit score by checking on it on a weekly or monthly basis without the need for a monitoring service. However, if you have recently experienced identity theft or a major data leak and want to keep an eye out for unauthorized activity, or if you are about to make a major purchase using a loan such as real estate or an auto, it may be worth it to subscribe.

Credit Score Requirements by Loan Type

Different lending products will have different minimum requirements, which we have listed here. These numbers will vary depending on the lender and the product, but you can use this as a general guide.

Keep in mind that lenders look at a variety of factors beyond your credit score, including income, extended lending history, assets, and otherwise, which means simply having the minimum credit score won’t automatically qualify you for the loan.

In addition, having a higher credit score than the minimum will net you better terms, including less of a down payment, a lower interest rate, and access to better card perks.

Loan Type | Minimum Score Required | Notes |

Personal loan | 600 to 670 | You may be asked to provide collateral such as real estate if you have a lower credit score. |

Line of credit | 600 to 670 | Like personal loans, you may be asked to provide collateral for lower scores. |

Auto loans | 500 to 680 | Be wary of lenders who offer no-credit auto loans, as these can come with extremely high interest rates. |

Mortgage | 620 | Some federally-backed loan types, such as VA or FHA loans, can have lower credit score requirements. |

Jumbo mortgage | 700 | Jumbo loans are any mortgage above $832,750 for a single-family house, or $1,249,125 in designated high-cost areas. |

Federal student loans | Dependent | While most federal loans don’t require a credit check, PLUS loans do. |

Private student loans | 640 to 680 | It’s common to have a cosigner for private student loans, as many students lack credit history. |

Business loans | 550 to 650 | Many business lenders will also check your business credit score, which is separate from your personal score |

Credit card | 580 to 800 | Card credit requirements can vary greatly, with some high-end cards requiring Exceptional/Superprime scores to qualify. Secured credit cards or credit-builder cards often have no or low credit requirements. |

Proven Tips to Improve Your Credit Score

Improving your credit score takes time and dedication. Key to this is focusing on the different factors that go into your score: payment history, utilization, inquiries, and credit mix. Here’s how to boost your credit score the smart way with Monarch.

Pay Every Bill on Time, Going Forward (Payment History)

The biggest impact to your credit score is your payment history. On-time payments contribute greatly to your positive history. On the other hand, missed payments, defaulted loans, or accounts sent to collections can quickly sink your score.

Make sure you make your payments every month. Set up automatic payments for the earliest date possible so you prioritize your payments over all else, and have a robust emergency fund that can help you cover your payments if you have an unexpected loss of income.

If you’re struggling to make payments, consider refinancing or consolidating your loans for a better rate or a simplified payment. You can also try asking your lender for a pause in payments due to hardship, which will allow you to hold off on paying without a negative mark on your score. While this won’t pause the interest, it will give you a chance to get back on your feet.

Monarch pro tip: Monarch can remind you of due dates for loan and credit card payments through Bill Sync. Simply connect your accounts in the Monarch app through our partner Spinwheel, and get automatic notifications based on your preferences when it comes time to pay. Monarch will track your payments based on your transactions in the app. Never miss a payment again!

Reduce Your Credit Utilization (Pay Down Balances)

Credit utilization can quickly change your score, depending on how much you charge on your credit cards. Getting close to the limit or using more than 20% of the credit limit at any one point in time can drive up your utilization ratio and drive down your score, which is why it’s in your best interest to keep your utilization down.

Ideally, you should be using your credit card like a debit card and only charging what you can afford to pay, then paying off the balance in full each month. If you have existing credit card debt, focus on paying it down. If you have multiple balances, consider using the snowball or avalanche method to tackle your debt efficiently.

Monarch pro tip: Use Monarch Pay Down goals to track your debt as you pay down your balance, giving you the psychological boost to stay disciplined and motivated.

Don’t Close Old Accounts (Maintain History and Limits)

Your credit score is calculated based on your payment history for open accounts. If you were to close all your cards and loan accounts, you would no longer have a score at all.

As such, old accounts, especially if you’ve held them for many years, can be a boon to your credit score. Maintaining an account for many years keeps your average age up, and the credit limit on them contributes to the credit pool that is used to calculate your overall utilization ratio. Closing these accounts might reduce your average age and increase your utilization ratio, which will drop your score.

Instead of closing an old card, see if you can keep it open with a small recurring transaction such as a monthly subscription that you pay off in full automatically, especially if the card has no annual fee. As mentioned above, you don’t need to worry about keeping a balance; just keeping the account open. You can “lock” the card or freeze your credit if you’re worried about thieves stealing your card info and running up the balance.

Monarch pro tip: You can track recurring expenses on all of your credit cards by linking your accounts to Monarch. It’s fast, secure, and an easy way to keep an eye on subscription-only accounts without having to juggle multiple logins.

Be Cautious with New Credit (Limit Hard Inquiries)

While there may be a credit card for everything, be careful about applying for new cards, loans, or lines of credit frequently. While you do have a grace period in which you can bundle your inquiries into one, applying for a new card every month will drag down your score and average account age.

Instead, keep a couple of cards open and focus on building history with your existing accounts.

Add Positive Credit History (If You Have Limited Credit)

Work on adding positive history to your account if you have limited credit. Many credit card companies offer credit builder cards with a low limit and a security deposit if you have a limited credit history. Some banks and lenders also offer credit builder loans, though these come with interest rates and fees. If you’re a student, consider getting a student card, or making small payments on your student loans to start building your score.

As always, make sure to keep your utilization low and make your payments on time.

The Authorized User Trick

If you want to start building positive credit history quickly, one trick is to become an authorized user on someone else’s credit card. This adds you on as a cardholder to the primary user’s account, which gives you their credit age and history. Authorized users have access to their own card, which draws upon the credit account of the primary user, though they aren’t required to use it. As such, you should only use this method with someone whom you trust and who makes their payments on time, and with someone who trusts you to have access to their card (although they technically don’t ever have to give you a card to use on the account).

Check Your Credit Reports for Errors and Dispute Them

Credit reports aren’t infallible. Sometimes, the credit bureaus or lenders who report to the bureaus can make errors, which can pull down your score if you don’t catch them. This is why it’s a good idea to check your report regularly.

You can dispute these errors and request that they be removed from your credit report.

For example, if your report includes missed payments for an account you’ve previously paid off, you can contact the reporting company and provide proof that you have paid off the balance and the report was made in error. This process is entirely free, and can be done through equifax.com, transunion.com or experian.com.

Should I Use a Credit Repair Company?

You may have heard of credit improvement or repair companies, which claim to improve your credit score by disputing errors on your credit report on your behalf in exchange for a fee or subscription. While these may improve your score, especially if you’re struggling to pay off debt, there are a few ways we recommend using to improve your score and pay off your debt before using a repair company.

- Prioritize consolidation and making payments. This can simplify payments and help build up your positive history.

- Try debt counseling. Using a non-profit debt counseling service certified by the National Foundation for Credit Counseling (NFCC), which can connect you to a certified counselor and help you pay off debt and improve your score.

- Be careful considering credit repair. Credit repair companies can be costly, and their process doesn’t always guarantee an improved score. You may be better off disputing errors yourself instead of outsourcing it.

Credit Score Myths Debunked

Because there are so many factors that go into your credit score, there are a few persistent myths about credit scores floating around. We’ll clear up the misconceptions here.

Myth: Checking Your Score Hurts it

Checking on your credit score or requesting your credit report doesn’t impact it at all. You can check on your score as many times as you like throughout the year, with free weekly credit reports available through Equifax, Experian and TransUnion.

What does impact it is when a lender, credit card company, or other entity performs what’s known as a hard inquiry, which is when they officially request your credit report in order to make a lending decision. This will lower your credit score by a few points, which means you’ll have to be careful about how many lending products you apply for in a small window. As such, you will always be informed ahead of time about a hard inquiry, and will have to give your permission for it to go forward.

Myth: Closing Old Cards Helps

Closing old credit cards doesn’t always help boost your score for two reasons: Age and utilization.

When you close an old account, you remove the average age from your account, which can really bring down your score if you haven’t had any other cards for that length of time. For example, if you have a 10-year-old card and a one-year-old card, then your average age will be 5.5 years. Closing the 10-year-old card will drop your average age to 1 year, which can bring down your score by a significant degree.

Closing an old card with a high limit can also impact your utilization ratio, as removing credit limits from the pool can increase the ratio. Let’s say you have three cards. Card one has a limit of $1,500 and a balance of $500, card two has a limit of $1,000 and a balance of $500, and card three has no balance and a limit of $500, giving you a utilization of approximately 33%. If you decide to close card three, you lose $500 from the credit pool, pushing your utilization ratio up to 40%.

Myth: You Need to Carry a Balance

This is one of the biggest, and most harmful, myths about credit scores. You don’t need to keep a balance on your credit cards in order to maintain your credit score. In fact, keeping a balance means that you’re increasing your base utilization ratio, which hurts your score in the long run. Not only that, you’ll end up paying unnecessary interest.

Instead of keeping a balance, you want to keep your lines of credit open, which maintains your payment history and pool of available credit, which impacts your utilization ratio. Otherwise, keep paying off the balance in full each month if you’re able to do so, and pay down whatever balance you currently have in a timely manner.

Myth: All Credit Scores are the Same

Credit scores differ between the different credit reporting bureaus and between the two score types.

Firstly, the credit bureaus (Experian, TransUnion, and Equifax) calculate your credit score with different weights. For example, TransUnion tends to weigh average account age more than the other bureaus. They may also report on slightly different information. Experian, for example, has a feature that allows you to report your utility payment history.

The two score types (VantageScore and FICO) also calculate scores differently. It’s important to note that FICO is by far the most popular credit score among lenders and card companies, which means that keeping an eye on your FICO score can give you a more accurate picture of what your lender is looking for.

Myth: Income Affects Credit Score

Income doesn’t impact your credit score directly. While if you make more, you may have an easier time keeping up with your payments and keeping a lower utilization ratio, your income isn’t directly reported to the credit bureaus and thus doesn’t have a bearing on your score.

Myth: Only Loans and Credit Card Payments Affect Credit Score

Your credit score can go beyond lending product payments. Old bills from utility companies, medical practices, and other entities can have a way of tanking your credit score if they’re sent to collections. This is why it’s a good idea to not just stay on top of your bills, but to regularly check in on your credit score so you can catch issues before they grow.

Take Charge of Your Credit Future

Your credit score is an incredibly important part of your financial picture. Not only does it determine your eligibility for loans and credit cards, it also can determine what interest rates, insurance premiums, card perks, and utility and housing access you get.

As your score is calculated using your payment history, credit utilization, and other factors around how you handle your loans and credit, staying on top of what and how you borrow is crucial to building your score over time.

Whether it’s your FICO or VantageScore, Monarch is there to help you every step of the way. With account linking, debt management tools, utilization tracking, and a handy way to monitor your score on your dashboard, Monarch can help you take control of your credit score journey and unlock the benefits of having a great credit score.

FAQs

How often should I check my credit score?

As a rule of thumb, you should be checking your credit score on a monthly basis to keep an eye on your payments, utilization ratio, and other factors. Incorporating checking your credit score into your weekly or monthly budgeting routine can be a good way to make it a habit.

What is a good credit score in the U.S.?

The strict definition of a “good” credit score is 670 to 739 for a FICO score, and 661 to 780 for a VantageScore (which, in this case, is known as “Prime.”) While this will qualify you for many lending products, having a FICO score of 740 or higher (“Very Good” to “Exceptional”) or 781 and above for a VantageScore (“Super Prime”) will give you access to the best interest rates and the widest variety of lending options.

How quickly can I improve my credit score?

You may start seeing small improvements on your credit score in about a month, though that will depend on what is on your credit history. Some negative marks on your score, such as a new credit inquiry, only fall off after three months. Others, such as bankruptcy, will take six years or more. As well, because of the way reporting works, it will take a minimum of 30 to 45 days for your credit score to change after you’ve closed an account, made an on-time payment or otherwise. Improving your credit score massively will likely take months or years, so be prepared to be diligent and patient.

Which credit bureau should I monitor?

Ideally, all three. Both FICO and VantageScore use all three bureaus in calculating your credit score. You can also keep an eye on all three by requesting a free weekly report from Equifax, Experian, and TransUnion through annualcreditreport.com.

What affects your credit score the most?

The biggest factor across both VantageScore and FICO is your payment history. Making payments on time, avoiding late payments, not going into default or bankruptcy, and keeping your credit utilization ratio low will go a long way to boosting your score.

Can I get a loan with a 600 credit score?

That will depend on the loan and the lender. While there are many lenders who will offer you a loan for a fair score, you won’t be offered as high a loan amount or as good an interest rate. Unsecured loans will also generally have higher credit score requirements than secured loans like mortgages or auto loans.

Why is my credit score different on different websites?

Different websites will pull from different credit bureaus. Some websites might use your VantageScore, while others will use your FICO score. They may also update at different times, so if you’ve recently increased your utilization ratio or closed a line of credit, it may take some time for some websites to update.

How can I start building my credit score as a student?

If you’ve taken out student loans, you can start making small payments on the account. Generally, this shouldn’t change your required minimum monthly payment starting time, and it will start to generate positive history on your account. You can also consider applying for a student credit card, which generally has low requirements, low limits, and perks for full-time students.