Retirement planning isn’t just about seemingly arbitrary numbers, accounts, and which investments to choose. It’s truly about understanding your complete financial picture and a vision for your future life. You need to first become clear on where you stand today, what you’ll need tomorrow, and what strategies will get you where you want to go.

Most people approach retirement planning one piece at a time. They open a 401(k) through their job. Perhaps they read an article on Social Security. Every now and again they may find themselves using an online calculator to see if they are “on track.” This results in a fragmented view and limited understanding rather than informed confidence that comes from seeing your entire picture clearly through your own eyes.

This guide is different. We’re going to walk through everything you need to know about retirement planning in 2026. How much do you actually need? Which accounts should you use and when? What should you be doing in each decade of your working life? How can you avoid mistakes that quietly derail even the best savers?

Whether you’re still in your 20s or approaching retirement in the next few years, this article will give you a framework that will provide clarity and essential tools.

What Retirement Planning Means in 2026

Retirement planning is the process of figuring out how much money you’ll need to live the life you want after you stop working. Then you’ll need to make deliberate decisions throughout your career to achieve this goal.

It sounds simple enough, but it plays out over decades and through changing tax laws, markets, and evolving lives. This is the reality of retirement planning. It’s complex because life doesn’t stay simple. In 2026, there are a few updates to retirement planning you should be aware of.

SECURE 2.0 changed the rules. The SECURE 2.0 Act of 2022 introduced several changes that are still being phased in. These include higher catch-up contribution limits, later ages for required minimum distributions (RMDs), new Roth treatment for employer contributions, and provisions designed to make it easier for part-time workers and small business employees to participate in retirement plans. If you haven’t revisited your retirement strategy since 2022, it’s worth taking a look at now.

The retirement confidence gap is real. According to the Employee Benefit Research Institute’s 2026 Retirement Confidence Survey, workers’ confidence they’ll have enough money to live comfortably in retirement fell yet again to 61%. The gap between how people feel and what they actually know about their own retirement planning is enormous. That’s exactly what we’ll work on in this guide.

The shift from pensions to personal responsibility is complete. For most Americans under age 60, pensions are from a bygone era. Retirement security is now almost fully self-funded, which means the quality of your retirement depends on the quality of your decisions. That’s both the challenge and the opportunity.

The goal of retirement planning isn’t to hand your financial future to somebody else. It’s to understand your picture clearly enough to make every decision on your own terms.

How Much You Actually Need to Retire

Here’s the most common mistake in retirement planning: people plan based on their income rather than their spending.

The traditional rule of thumb says you’ll need between 70-90% of your pre-retirement income. That is a rough proxy at best. Your salary tells you almost nothing about what you actually spend. High earners who save aggressively might spend 40% of their income. Middle-income households with high fixed costs might spend 95%.

Plan from your spending, not your salary. The question isn’t “what percentage of my income will I need?” It’s “what does my life actually cost and how will that change in retirement?”

Start with your current annual expenses. Then adjust for retirement-specific changes. You’ll no longer be commuting. You also won’t be saving for retirement anymore. You may have paid off your mortgage. On the other hand, you may spend more on travel, healthcare, and leisure throughout your retirement.

The 4% Rule and Its Limitations

The 4% rule is the most widely cited retirement planning guideline. It states that you should withdraw no more than 4% of your portfolio in year one of retirement, then adjust that amount for inflation each year, and you’ll have a very high probability of not running out of money over a 30-year retirement.

For a $1 million portfolio, that’s $40,000 per year. To live on $80,000 per year, you’d need $2 million. The formula is simple: annual spending / 0.04 = retirement portfolio target.

The 4% rule was developed based on historical market data (the Trinity Study), and it’s a reasonable starting point, but has real limitations.

- It assumes a 30-year retirement. If you retire at 55, you may need to fund your life for 40 or more years.

- It’s based on historical U.S. stock and bond returns, which may not repeat.

- It doesn’t account for flexibility. Most retirees naturally spend less in down years.

- Healthcare and long-term care costs can blow through assumptions.

A better approach is to use the 4% rule as a sanity check, and not a ceiling. Run your own scenarios with your actual numbers including your real spending, accounts, and timeline.

Savings Benchmarks by Age

If you want a quick gut-check on where you stand, savings benchmarks by age offer a decent starting point. These are rough targets, and not laws. They give you something by which you can evaluate where you stand today.

Age | Benchmark | Example ($100k salary) |

30 | 1x your annual salary | $100,000 |

40 | 3x your annual salary | $300,000 |

50 | 6x your annual salary | $600,000 |

60 | 8x your annual salary | $800,000 |

67 (retirement age) | 10x your annual salary | $1000,000 |

These benchmarks assume full Social Security benefits at age 67, a roughly 15% savings rate throughout your career, and spending in retirement that’s between 55-80% of pre-retirement income. If you find you’re behind the benchmark, that’s merely information and not a verdict. It tells you where to focus on improving.

The $1,000-a-Month Rule

A simpler heuristic is for every $1,000 per month you want in retirement income (not including Social Security), you need approximately $240,000 saved, assuming a 5% annual withdrawal rate. If you want $4,000 per month from your portfolio, you need around $960,000 in this case. This is not a replacement for real math, but instead a fast way to connect a savings number to a monthly income.

The Retirement Accounts You Need to Know

Before you can optimize, you need to understand the tools. Here’s what’s available, how they work, and how to think about which ones to take advantage of.

401(k) Plans

A 401(k) is an employer-sponsored retirement account that lets you contribute pre-tax dollars, reducing your taxable income today. Your investments grow tax-deferred and you pay ordinary income taxes when you withdraw in retirement.

2026 contribution limits: $24,500 for those under age 50. Workers aged 50-59 can contribute an additional $8,000. A special catch-up amount of $11,250 is allowed for workers between the ages of 60-63.

Always capture the employer match first. If your employer matches contributions up to a certain percentage of your salary, that’s an instant 50-100% return on those dollars. Not maximizing the match is leaving compensation on the table.

Many employers now offer a Roth 401(k) option, which accepts after-tax contributions but grows tax-free. We’ll discuss that more below.

Traditional IRA

An Individual Retirement Account (IRA) you fund with pre-tax dollars (if you meet income and deductibility requirements). Much like a 401(k), growth in a traditional IRA is tax-deferred and withdrawals are taxed as ordinary income.

2026 contribution limits: $7,500 per year, or $8,600 if you are 50 or older.

Income limits for deductibility: If you have access to a workplace retirement plan, your ability to deduct traditional IRA contributions phases out at higher income levels. Check out the IRS’s current thresholds as they can adjust annually.

Roth IRA

A Roth IRA is funded with after-tax dollars. The payoff is that qualified withdrawals in retirement, including all the growth, are completely tax-free. Roth IRAs also have no required minimum distributions during your lifetime, which makes them powerful for estate planning and tax flexibility in retirement.

2026 contribution limits: Same as the traditional IRA, but Roth IRAs have income limits for direct contributions. In 2026, eligibility phases out for single filers above $153,000 and for married filing jointly above $242,000. If you’re above the phase out incomes, look into backdoor Roth IRA strategies.

Health Savings Accounts (HSAs)

Often overlooked as a retirement tool, the HSA is arguably the most tax-efficient account available. Contributions are pre-tax, growth is tax-free, and withdrawals for qualified medical expenses are also tax-free. A triple tax advantage. After age 65, you can withdraw for any reason and pay ordinary income taxes like a regular traditional IRA.

HSAs require you’re enrolled in a high deductible health plan. So one solid strategy is maxing out your HSA and investing it for the long-term. Pay current medical expenses out of pocket if at all possible, and let the HSA compound. Healthcare is typically a retiree’s biggest variable expense. Having a dedicated tax-advantaged pool set aside for it is significant.

2026 HSA limits: $4,400 for individuals and $8,750 for families.

SEP IRA and Solo 401(k)

For self-employed individuals and small business owners, these accounts offer dramatically higher contribution limits than standard IRAs.

A SEP IRA allows contributions of up to 25% of the net self-employment income, with a dollar cap that adjusts annually. It’s fairly simple to set up and maintain.

A Solo 401(k) allows for both employee and employer contributions, often permitting higher total contributions than even a SEP IRA for those with moderate self-employment income. It also allows Roth contributions and participant loans.

Choosing Between Accounts: Traditional vs. Roth

The core question is do you want to pay taxes now or later? Here are a few things to consider:

Situation | Consider |

You’re in a low tax bracket now, expect higher tax rates later. | Roth IRA or Roth 401(k) |

You’re in a high tax bracket now, expect lower in retirement. | Traditional 401(k) or Traditional IRA |

You want flexibility and no RMDs | Roth IRA |

You’re unsure and want to hedge your bets | Split contributions between traditional and Roth |

You’re above the Roth income limit | Backdoor Roth IRA (consult a professional first) |

The right answer depends on your current tax rate, expected retirement tax rate, time horizon, and state taxes. Most people benefit from having both pre-tax and Roth assets. It gives you flexibility to manage taxable income in retirement.

A Decade-by-Decade Retirement Action Plan

In Your 20s: Start Early, Automate Everything

Time is your biggest asset, by far. A dollar invested at 25 has roughly four times the growth potential of a dollar invested at 45, assuming a 7% average annual return. Compounding works well in your favor if you let it.

The priority list for your 20s:

- Capture your full employer 401(k) match, don’t skip this if at all possible.

- Build an emergency fund of 3-12 months of essential expenses so a job loss or unforeseen circumstance doesn’t force you to raid your retirement accounts. While building a full emergency fund is important, it can take considerable time. Prioritize a starter emergency fund of $1,000 or one month of net income to start.

- Open a Roth IRA and contribute what you can. Young earners often pay low marginal tax rates. Locking in tax-free growth now is a tremendous advantage.

- Automate contributions so you never have the temptation to skip a month.

- Invest in low-cost, diversified index funds. Don’t let perfect be the enemy of good.

When you’re young, even $50 per month matters. The goal in your 20s is to build the habit and let time in the market be on your side.

In Your 30s and 40s: Increase Contributions as Income Grows

Your 30s and 40s are when income typically rises, but also when competing financial priorities pile up. Mortgage, childcare, aging parents are all factors that could absorb any pay raise.

The priority list for your 30s and 40s:

- Push 401(k) contributions toward the maximums as your income allows. Specifically, contribute enough for your employer match first and foremost. Then build to 10% of gross income, and finally up to 15% or the amount needed to fully maximize.

- Fund a Roth IRA if eligible, or consider executing a backdoor Roth if your income exceeds the limit.

- Max your HSA if you’re in a high deductible health plan.

- Revisit your asset allocation as you approach your 40s. You still want significant equity exposure, but a check-in at this point really makes sense.

- Run a retirement projection. Not just “am I on track?” but “what happens if I increase my contributions by 1 or 2%?” and “what if I retire at 60 instead of 65?” Run the scenarios.

- Build understanding of your investments. Fees compound as well so make sure you’re keeping fees such as fund expense ratios as low as possible. It is advisable to keep expense ratios under 0.5%.

This is also when couples need to coordinate explicitly. Ensuring you’re on the same page as you save for retirement in separate accounts is crucial. A cohesive household retirement strategy will keep both parties informed and on track. You should also refer to Monarch’s priority checklist if you are simultaneously paying down debt.

In Your 50s: Accelerate and Prepare

Your 50s are the last major window to building your nest egg, and also the first window to seriously stress-test your retirement plan.

The priority list for your 50s:

- Maximize catch-up contributions if possible. New rules have expanded the catch-up contribution limits for people over 50 and then again for people between the ages of 60-63.

- Eliminate high interest debt before retirement. Carrying expensive debt into a fixed income is a structural problem.

- Start healthcare planning. If you stop working before age 65 you’ll need to figure out how you’re going to bridge the gap for health insurance. This could be through marketplace coverage, a spouse’s plan, or other options.

- Get serious about Social Security optimization. Run the numbers on different claiming ages. If you’re married, the spousal and survivor benefit strategies are important to understand.

- Shift toward a more conservative asset allocation, but don’t over-correct. With a potentially 30-year retirement, you will still need growth in your portfolio. Many financial planners suggest something in the range of 50-70% equities in your late 50s, but the right allocation really depends on your specific situation.

- Consider working with a fee-only financial planner to review your overall picture if you haven’t already.

In Your 60s: Transition and Execute

Your 60s are when planning becomes action. This decade involves some of the most consequential financial decisions of your life such as when to claim Social Security, enrolling in Medicare, and sequencing your withdrawals.

The priority list for your 60s:

- Decide on your Social Security timing. This is a major decision. More on this below.

- Enroll in Medicare at age 65. Missing the enrollment window can result in premium penalties. If you’re still covered by an employer plan, understand how that interacts with Medicare.

- Develop your withdrawal strategy. Which accounts do you draw down first? The sequencing has major tax implications.

- Run a full retirement income projection with your actual numbers. How much will come from your Social Security? How much from your portfolio? What does your spending look like in your first retirement year versus 15 years into retirement?

- Revisit your estate plan including beneficiaries, wills, powers of attorney, and healthcare proxies.

In Your 70s and Beyond: Manage and Optimize

Required minimum distributions (RMDs) begin at age 73 now. You must withdraw a calculated minimum from traditional IRAs and 401(k)s each year, and pay ordinary income taxes on them. Failing to take your RMD results in a 25% excise tax on the amount you should have withdrawn.

Qualified Charitable Distributions (QCDs) allow you to transfer $111,000 per person each year directly from your IRA to a qualifying charity, satisfying your RMD obligation without the transfer counting as taxable income. For charitably inclined retirees, this is one of the best tax strategies available.

Estate planning becomes increasingly important in your 70s and beyond. Your beneficiary designations, account titling, and trusts all need to be reviewed. The rules governing inherited IRAs also changed under the SECURE Act. Non-spouse beneficiaries generally must deplete the inherited accounts within 10 years, which has major implications for how you leave accounts to heirs.

Social Security: When to Claim and Why It Matters

Social Security is the largest single source of retirement income for most Americans, yet most people make the claiming decision without fully understanding the stakes.

The Basics

Your Full Retirement Age (FRA)is the age at which you receive 100% of your earned benefit. For anyone born in 1960 or later, FRA is 67.

- Claim at 62 (the earliest possible): Your benefit is permanently reduced by up to 30%.

- Claim at FRA (67): You receive 100% of your earned benefit.

- Claim at 70: You receive 124% of your FRA benefit, thanks to delayed retirement credits of 8% per year between 67 and 70.

The difference between claiming at 62 versus 70 can be 70-80% higher monthly payments for the rest of your life.

When Earlier Claiming Makes Sense

Claiming early isn’t always the wrong choice. It may make sense if:

- You have a serious health condition and shorter life expectancy.

- You need the income and have no other good options.

- You’re coordinating with a spouse’s higher benefit and the math favors early claiming for you.

Strategies for Couples

For married couples, Social Security optimization is a coordination problem to solve. The higher earner’s benefit matters most because it determines the survivor benefit (the amount the surviving spouse receives for the rest of their life).

A common strategy is that the lower earner claims early (providing income), while the higher earner delays until 70 to max the survivor benefit. There’s no universal right answer, so run the math with your specific numbers and ages.

Spousal benefits: A spouse who earned little or no income may qualify for a benefit equal to up to 50% of the higher earner’s FRA benefit. This is separate from the survivor benefit and is worth understanding explicitly.

Investment Strategies for Every Stage

Asset Allocation by Age and Risk Tolerance

Asset allocation is how you divide your portfolio between stocks, bonds, and other assets and is one of the most consequential retirement planning decisions you’ll make.

A classic heuristic: subtract your age from 110 (or even 120 if you’re more aggressive) to get your stock allocation. A 40-year-old might hold 70-80% stock, whereas a 65-year-old might hold 45-55%. Risk tolerance, other income sources, and retirement timeline matter as much as age though, so don’t forget to include them when thinking about your allocation.

In your accumulation (working) years: More equity exposure makes sense. Volatility hurts in the short-term but over the long-term you’ll see compounding take hold. A temporary market drop when you’re 40 is not necessarily a crisis so much as it is an opportunity.

In retirement: The sequence of returns matters enormously. A significant market decline in the first few years of retirement can be permanently damaging in a way that a mid-career decline is not. This sequence of returns risk is a reason to hold more conservative assets as you near and enter the retirement stage.

Target-Date Funds vs. DIY

Target-date funds automatically shift from aggressive to conservative allocations as your target retirement year approaches. They’re simple, low-maintenance, and broadly diversified. For many people, especially those who don’t want to actively manage their portfolio, a low-cost target-date fund is a perfectly solid choice.

DIY asset allocation gives you more control and you can customize your allocation, minimize fees more aggressively, and make tactical adjustments. The trade-off is time, attention, and the risk of making emotion-based decisions during market volatility.

Neither approach is universally superior. What matters most is that you’re invested, diversified, and consistent.

Rebalancing in Retirement

Over time, different assets grow at different rates and this can cause your allocation to drift. Rebalancing, meaning selling overweighted assets and buying underweighted ones, keeps your portfolio aligned with your intended risk level.

In retirement, rebalancing takes on additional complexity, as you’re drawing down assets, not just reallocating them. The general principle is to draw from overweighted assets first (natural rebalancing through withdrawals), and to be thoughtful about which accounts you draw from to manage tax efficiency.

Planning Retirement as a Couple

When two people retire, the financial picture is more complex, but also there’s more opportunity.

Aligning on Timeline and Lifestyle

The most important retirement planning conversation couples often don’t have: what does retirement actually look like for each of you? Are you going to stay where you are? What does your daily schedule look like? Who retires first? Even a small age gap between partners can mean a decade’s difference in retirement income planning.

Get very specific. What does a good retirement week look like? Where do you want to live? What does your ideal budget look like? Getting aligned on lifestyle expectations will make everything else easier.

Coordinating Accounts and Benefits

Couples have more flexibility than individuals, but that flexibility requires active coordination.

- Maximize both employer matches: never leave an employer match on the table because you’re focusing all savings in only one partner’s account.

- Coordinate Roth vs. traditional contributions: based on your combined income and projected retirement tax situation.

- Optimize Social Security timing: Do this together, not separately. The decision each of you make about when to claim affects the other’s survivor benefit.

- Medicare enrollment: for each partner enrollment is independent, so track both timelines.

Yours, Mine, and Ours

A useful mental model for couples managing joint finances is to think of accounts as “yours”, “mine”, and “ours”. All accounts need to be visible in one place to make coherent decisions.

Monarch is designed specifically for household financial management, both partners see the same complete picture. This makes retirement coordination an ongoing conversation rather than a quarterly reconciliation.

Tax-Efficient Withdrawal Sequencing

One of the biggest drivers of how long your money lasts isn’t your investment returns, it’s how you draw it down. Tax-efficient withdrawal sequencing can make a meaningful difference in your after-tax retirement income.

The General Framework

Step 1: Required minimum distributions. If you’re over 73, you have no choice and need to take your RMDs first to avoid penalties.

Step 2: Taxable accounts. Draw from taxable brokerage accounts next, where long-term capital gains rates are often lower than ordinary income tax rates. Selling appreciated assets here may trigger capital gains, but potentially could be lower at 0% or 15% for many retirees.

Step 3: Tax-deferred accounts. Withdrawals from your 401(k) or traditional IRA count as ordinary income. Draw these down before Roth accounts, but manage your brackets, don’t pull so much that you spike into a higher bracket unnecessarily.

Step 4: Roth accounts last. Roth withdrawals are tax-free and not subject to RMDs. Letting Roth accounts compound as long as possible, and leaving them to heirs or drawing on them in high-tax years, is typically the most advantageous strategy.

This is a framework and not a formula. Your specific tax situation, Social Security income, Medicare premiums, and state taxes all affect the optimal sequence.

Common Retirement Planning Mistakes (and How to Avoid Them)

Starting Too Late

Compound interest is time-dependent. Starting at 35 instead of 25 doesn’t mean you’re 10 years behind, it means you’ve lost years of exponential growth. Waiting from 25 to 35 to start saving can cost you hundreds of thousands of dollars by the time you retire.

The fix is to start now, regardless of how much. Even small contributions create the habit and begin compounding. Then continue to increase over time.

Not Maximizing the Employer Match

Failing to contribute enough to earn the full employer match is the most common and most expensive retirement planning mistake. An employer match is literally free compensation you’ve earned but haven’t claimed.

Ignoring Inflation

A retirement that costs $50,000 per year today will cost roughly $93,000 in 25 years at 2.5% inflation. Plans that don’t explicitly model inflation tend to look better than they actually are.

Underestimating Healthcare Costs

An average 65-year-old couple in retirement could easily spend well into the six figures on healthcare. Medicare doesn’t cover everything, and costs can add up quickly. Build healthcare into your budget as well.

Over-Relying on Social Security

Social Security was designed to replace roughly 40% of pre-retirement income for average earners. Most Americans need substantial personal savings to maintain their standard of living. Treating Social Security as a safety net rather than a retirement income plan is the best way to frame it.

Not Adjusting for Taxes

Gross retirement income is not net retirement income. A $1 million traditional IRA is not worth $1 million to you, as every dollar you withdraw is taxable. Not accounting for taxes in your retirement projections can lead to overconfidence.

Cashing Out When You Change Jobs

When you leave an employer, you’ll typically have the option to cash out your 401(k). Doing so triggers ordinary income taxes and if you’re under 59 ½, a 10% early withdrawal penalty. Instead, consider rolling the funds to an IRA or the new employer’s plan, or even leave the 401(k) where it is for now.

Retirement Planning in Monarch

Monarch is built for exactly this kind of household complexity. Here’s how it works in practice for retirement planning:

- Connect all of your accounts. Monarch aggregates your retirement accounts alongside everything else including your cash accounts, mortgages, loans, etc. You’ll see your complete financial picture all in one place. Net worth, investment performance, spending, and retirement balance are all visible together.

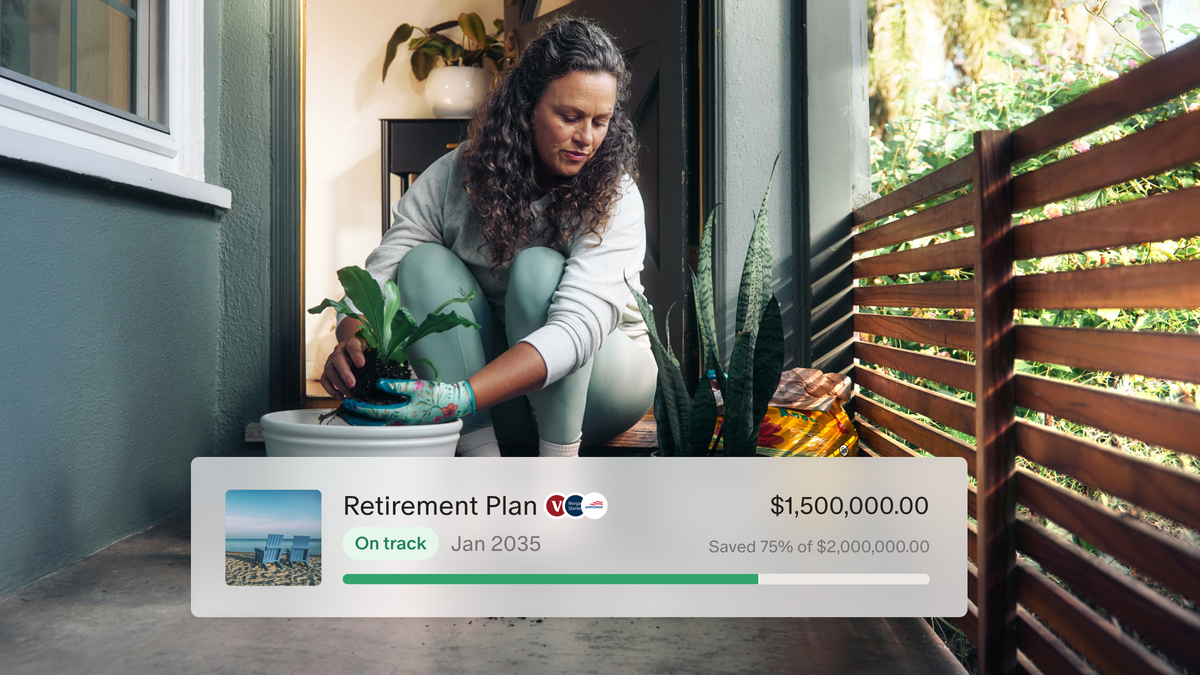

- Create a retirement goal linked to your accounts. Set a retirement goal in Monarch and link your retirement accounts directly to it. As you contribute and your portfolio grows, your goal progress will update automatically. There’s no manual tracking required.

- Set growth rates for long-term goals. Monarch’s goal tools let you set projected growth rates, so your retirement projection reflects investment growth, not just contributions. Your number isn’t static, it evolves with your actual situation.

- Use Forecasting to model scenarios with your real numbers. This is where retirement planning gets real. What happens if you retire early at 60 instead of 65? What if you increase your contribution rate by 3%? Can you afford to take a mid-career break? Monarch’s forecasting tools let you run these scenarios with your actual account balances, income, and spending so they won’t be just hypothetical assumptions. If you’re curious what retiring at 60 instead of 65 costs you, Monarch tells you with your real numbers and not just arbitrary assumptions.

- Validate your investment picture. The Investments view in Monarch shows your asset allocation, performance, and holdings across all accounts. You can see whether your allocation actually matches your intention and track performance over time.

The goal isn’t to hand your retirement planning to an algorithm. It’s to give you complete clarity so that every decision you make regarding your retirement is informed, specific, and truly yours.

Your Retirement Planning Checklist for 2026

If you’re just getting started:

- Open a 401(k) and contribute at least enough to earn the full company match.

- Open a Roth IRA and set up automatic contributions (check to make sure you’re eligible).

- Open an HSA if you’re enrolled in a high deductible health plan.

- Check your Social Security earnings record at SSA.gov.

- Run a basic retirement projection to establish your baseline.

If you’re in your accumulation years:

- Max your 401(k) if possible.

- Max your Roth IRA if eligible.

- Max your HSA if possible.

- Rebalance your portfolio to your target allocation.

- Review your investment fees.

- Update your beneficiary designations.

- Coordinate with your spouse on your combined retirement strategy if applicable.

If you’re within 10 years of retirement:

- Maximize catch-up contributions if you’re over 50.

- Run detailed Social Security timing scenarios.

- Plan for healthcare between retirement and Medicare eligibility at 65 if applicable.

- Develop a tax-efficient withdrawal sequence strategy.

- Eliminate high-interest debt before you retire.

- Review and update your estate plan.

Remember under SECURE 2.0 there are changes to RMDs, catch-up contribution windows, and Roth 401(k) matching. Check to confirm you understand how these changes may affect your retirement planning.

Retire With Confidence, Not Guesswork

Retirement planning isn’t a one-time event. It’s a continuous process of understanding where you stand, modeling where you’re headed, and making deliberate decisions to close the gap.

The people who retire with confidence aren’t the ones who got lucky. They’re the ones who understand their picture completely. They know every account, every income source, and they control their spending. Their decisions are informed and made over decades. You don’t have to guess whether you’re on the right track with Monarch.

FAQs

How much do I need to retire?

The answer to this depends primarily on your spending, not your salary. Calculate your expected annual retirement expenses, then divide by your anticipated withdrawal rate. 4% is a common starting point, but not the rule. If you plan to spend $80,000 per year and use a 4% withdrawal rate, you need $2 million. Add Social Security in to reduce the burden on your portfolio. Your SSA statement will show your estimated benefit at different claiming ages.

What is the 4% rule?

The 4% rule states that you can withdraw 4% of your portfolio in your first year of retirement, then adjust that dollar amount for inflation annually, and have a very high probability of not running out of money over a 30 year retirement period. This is a useful guideline and not a guarantee. Actual results depend on market performance, your spending, and your retirement length.

When should I start saving for retirement?

Now is the best time to start regardless of your age. The earlier you begin, the more compounding works in your favor. It’s never too late to improve your position, either. Starting at 40 is dramatically better than starting at 50.

What are catch-up contributions?

Catch-up contributions are additional amounts that workers 50 years old and older can contribute to retirement accounts beyond the standard limits. For 401(k)s in 2026, the base limit is $24,500, but workers over 50 can add another $8,000. For those ages 60-63, you can contribute an extra $11,250.

How much Social Security will I get?

Create an account at SSA.gov to access your personal Social Security statement, which shows your projected benefit at 62, FRA, and 70 based on your actual earnings history. The numbers are specific to you. General averages aren’t useful for individual planning.

When should I take Social Security?

It fully depends on your health, your spouse’s benefit, your other sources of income, and your tax situation. Delaying increases your monthly benefit by 8% per year between FRA and 70. For most healthy people who can afford to wait, delaying to 70 makes mathematical sense, but the right answer requires running your specific numbers.

What are RMDs and when do they start?

Required minimum distributions are mandatory annual withdrawals from traditional IRAs and 401(k)s. Under current law, RMDs begin at age 73. The amount is calculated based on your account balance and IRS life expectancy tables. Failing to take your RMD will result in a penalty, 25% on the amount you should have withdrawn.

Should I use a 401(k) or an IRA?

Ideally, you can use both. Start with the 401(k) particularly if your employer offers a company match. Then fund a Roth IRA if you are eligible. The right blend of traditional versus Roth depends on your current and expected future tax rates. When in doubt, having both gives you flexibility.

How do I make my money last in retirement?

Three key factors are a sustainable withdrawal rate, tax-efficient sequencing of account withdrawals, and keeping enough equity exposure throughout retirement to maintain long-term growth. The biggest risk to portfolio longevity is a combination of poor sequence of returns in early retirement and overspending. Monitoring your actual spending against your plan, not just annually, but continuously, is what will keep you on track.