One in ten American adults is 'unscoreable' — meaning their credit history is too thin (or nonexistent) to qualify for a credit card or loan according to the Federal Reserve. Lacking a credit score can be a major roadblock to getting your first mortgage, renting your first apartment, or getting your first credit card.

That's why your first credit card matters: it's often the gateway to building your credit score. Your first card often becomes your oldest account, which helps lift your average age of accounts — part of the 15% of your FICO score that comes from length of credit history

Choosing your first credit card is an important decision. This guide will walk you through choosing the right card for you, the application process, and what to do in the first year so you can start building your credit score.

Key Takeaways

- The most common cards to choose from are secured card, student cards, and unsecured starter cards.

- You’ll have to meet certain requirements for a starter card, including verified income, being a full-time student, putting down a deposit, and/or having a cosigner on the card.

- Making payments on time, keeping your utilization ratio low, and paying off the balance in full each month are key to building your credit score with your card in the first year.

Why have a credit card?

Credit cards come with a number of advantages, some of which are key to navigating today’s digital and financial landscape. If you’re hesitating to apply, consider some of the advantages below.

- It’s one of the easiest ways to build your credit score. Because credit cards are more accessible and affordable than taking out a loan, it’s a good way to get your credit file started.

- Many services require you to have a credit card. Vehicle and equipment rental agencies often require you to have a credit card on file, and many hotels require you to pay for your booking with a credit card.

- It’s more secure than a debit card or cash. If you have a fraudulent transaction on your card, you can reverse it through a chargeback, making it easier to get your money back through the Fair Credit Billing Act's $50 liability cap.

- You can take advantage of card rewards. Card rewards can earn you cash back on purchases, airline and travel miles, perks at certain brands, and more.

The earlier you get your first credit card, the better off you’ll be in terms of credit score building. A survey conducted by the Federal Reserve found that users who entered the credit scoring system at age 18 had a higher credit score at the age of 30 than those who entered at older ages.

That same study found that 18-year-olds who started off with a credit card as their first credit product had higher scores at the age of 30 than those who used auto loans or retail cards as their first credit product.

Getting a credit card doesn’t mean that you’re automatically going to take on debt or have to pay interest. With the right strategy and careful management, you can get the benefits of using a credit card and mitigate some of the risks.

What counts as a "first credit card"

Your first credit card will likely be a card that doesn’t require a credit history, which is the reason many credit beginners apply for a card in the first place. Low and no-credit credit cards typically fall into one of three categories:

- Secured cards, which require a deposit of cash equal to the credit limit on the card.

- Student cards, which are designed for college and university students.

- Unsecured starter cards, which don’t require a deposit but typically require a co-signer, or have an extremely low card limit, and don’t come with rewards.

If you’re under 18, or don’t have a credit history, your first credit card may be an authorized user card, which is when a cardholder you know chooses to give you what is essentially a copy of their card. Purchases made on these cards count toward the primary cardholder’s balance on their account, making them legally responsible for paying them off. Their card history also counts towards the authorized user’s credit history, making it an easy way for newer users to build credit early on.

Are you ready for a credit card?

Before you apply for a credit card, you’ll need to make sure you meet a few requirements.

Hard requirements

While credit cards will vary in terms of their specific requirements, there are some hard-and-fast rules to follow when you apply for a card in your name.

- You have to be 18 or older. If you are under 21, you will also have to supply proof of income or have a cosigner.

- You have to have permanent residency, be a US citizen, or be a qualified student or diplomat. Tourists and non-qualified temporary residents cannot apply.

- You have to have proof of income. This can include income from a full or part-time job, gig, freelance, or business income, household income, retirement or investment income, Social Security income, alimony, child support, trust funds, or financial aid or scholarships.

- You have to have a minimum credit score, provide a deposit, or have a cosigner. Credit card companies use your credit score to gauge how reliably you’ll pay down your balance. If you have no credit score or a low one, you’ll generally only qualify for a secured card or have to take on a co-signer.

Self-check

Meeting the hard requirements for a credit card is the first step to applying. The second step is to evaluate whether you’re emotionally and financially ready to apply for a card, and if you can handle the responsibility of one.

Before you apply for a credit card, ask yourself these questions:

- Do I have a way to track and manage my spending? Having a budget and spending limits will ensure you can pay off the balance.

- Can I handle the temptation to spend? If you have a tendency to overspend or impulse spend, consider how you can put limits on yourself and your card.

- Do I have the ability to pay off the balance each month? Have a hard personal limit (which isn’t the same as the card limit) that fits into your budget and income.

- What is the plan if I can’t pay off the balance? Have a plan in place if you are unable to pay the balance in full, whether it’s drawing from savings, paying off the balance next month, paying off the balance over several months, or moving the balance to a zero-APR balance transfer card.

- Is my partner on the same page about this? If you share finances with someone else, it's important they know you're applying for a credit card and what parameters you set around it.

After you’ve considered these questions, it’s time to think about which card is best for you.

Your three options: secured, student, or starter unsecured

If you’re applying for your very first credit card, you’ll get to choose from three different types of cards: Secured, student, and unsecured starter. Here’s a quick overview comparing the three types, with a more in-depth look at each type below.

Secured cards | Student cards | Unsecured starter cards | |

Eligibility | Nearly anyone can qualify with a deposit | Can qualify if you are a college/university student with income | Can qualify with good income or cosigners |

Income | Can qualify with no income | Requires income | Requires income |

Limit | As much as deposit | Low to medium | Low |

Deposit | $100 to $500 | Not required | Not required |

APR | 14% to 29%* | 16% to 26%* | 25% to 37%* |

Co-signer | Not required | Not required | May be required |

Time to upgrade | Six months to a year | Two to four years | Six months to a year |

Rewards | Varies | Yes | No |

*Numbers pulled from Bankrate.com as of May 29, 2026

Secured cards

Best for: Total credit card beginners

Secured cards are the most common and easiest to qualify for starter cards, as most card companies will accept your application even with bad or no credit. This is because the card is secured with a cash deposit equal to the card limit, which the card company can use to repay themselves if you fail to pay off the balance.

Deposits, and your credit limit, tend to range from $100 to $500. Most secured cards don’t offer rewards, but if you’re in good standing with the credit card company and have built enough credit history, you can upgrade your card to one with more perks and get your deposit refunded.

Student cards

Best for: Students with qualifying income

Student cards are designed for students enrolled in a college or university, allowing you to start building your credit history and take advantage of card rewards from the start. Most don't require a credit score. They typically ask only that you're enrolled in a qualifying program and have proof of consistent income — scholarships, financial aid, a part-time job, work study, a side hustle, even an allowance.

Many cards come with traditional credit card reward programs, such as cash back with every purchase. They can also offer student-exclusive rewards such as discounts on books and supplies, or cash bonuses for good grades.

Once you graduate, if you’re in good standing, the card company will often upgrade your student card to a standard card, often with higher limits and similar or better rewards.

Starter unsecured

Best for: Beginners without the cash for a deposit

If you don’t have the cash for a deposit, there are unsecured starter cards available. These cards tend to come with extremely low credit limits and high interest rates, which makes them a bit riskier than secured or student cards. Card companies may scrutinize your income more carefully, set a higher income requirement, or require direct deposit.

Though this is becoming less common, some card companies will require you to have a cosigner on an unsecured card. Your cosigner will agree to be responsible for the balance and any accumulated interest on your card if you fail to make the payments, and will usually have to have a good credit score and credit history.

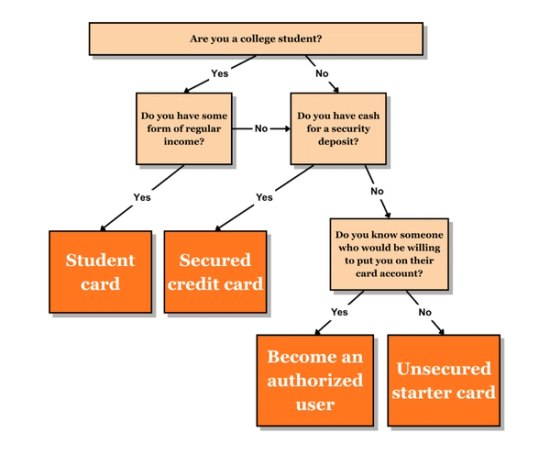

How to choose the right credit card for you

Trying to figure out which card is right for you? Here’s a simple decision tree to help you narrow down your choices.

For example, if you’re a 19-year-old with part-time income and no credit history, a secured card with a $200 deposit will give you more options than an unsecured card or being an authorized user.

On the other hand, if you’re a student, a student card can net you more rewards or get you bonuses based on your grades.

How to apply for a credit card

Once you've chosen a card, you'll submit an application, undergo a credit check, and provide supporting documents. First-time applicants will generally have a longer waiting period since you’ll have to submit additional verification and documents due to a lack of credit history.

Step 1: Check your credit history

Even if you're sure you have no credit history, check anyway. Sometimes rental payments, utility bills, and Buy Now Pay Later (BNPL) payments are reported to credit bureaus, and if you’ve ever had a bill go to collections, it may end up on your credit report.

You can check your credit report from the three bureaus for free through annualcreditreport.com. If you want to see your score, you can either make an account through one of the three bureaus or check your score through a third party. For example, you can see your VantageScore on your Monarch account dashboard.

If you’ve frozen your credit score (which Monarch recommends you do in order to protect yourself from fraud and identity theft), now is the time to “unfreeze” in order to apply for a card. Once you’re approved and you have your card in hand, you can freeze it again.

Step 2: See where you pre-qualify

If you have a credit history, you may pre-qualify for a card.Prequalifying is when companies use a soft credit check to tell you, in advance, which of their cards you're likely to be approved for. You can prequalify for as many cards as you think you’re eligible for, though confirm the issuer is only running a soft check before you submit information.

Step 3: Gather documents

Once you’re ready to officially apply, get your relevant documents and information ready to submit to the card issuer. Though requirements will vary depending on the card, you’ll generally need:

- Your Social Security Number or Individual Taxpayer Identification Number

- Identification such as a driver’s license or passport

- Proof of income, usually through your W2 or paystubs

- Proof of student status (if you’re applying for a student card)

- Co-signer information (if using a co-signer)

Step 4: Apply for one card at a time

. When you officially apply for a card, card issuers will conduct a “hard” inquiry that officially appears on your credit report. A hard inquiry lowers your score by a few points for less than a year. Too many hard inquiries, however, can quickly pull down your score.

Step 5: If approved, set up autopay immediately

Once you’re approved and your card is activated, set up autopay — ideally for the full statement balance, or for the minimum payment as a safety net if you'll pay the rest manually. By keeping autopay on in the background, you’ll make sure you don’t miss any payments and that you won’t rack up any late fees, excess interest, or hits to your credit score.

How to use your credit card for the first year

Starting out the right way with your first credit card can make upgrading, applying for a second card, or applying for other lending products much easier down the line. Here’s what to do in the first twelve months of having your credit card.

Month 1

The first month is mostly housekeeping and getting your card set up. In general, you’ll want to:

- Activate your card. New cards will come with instructions on how to activate them safely.

- Note your statement period and payment due date. Your statement period is when charges will contribute to the monthly statement that needs to be paid off if you want to avoid interest, and your due date is when your minimum monthly payment is due, typically 15 to 30 days after the end of the statement. They may not coincide with the first days of the month, so be aware.

- Set up autopay. While the baseline is the minimum payment, paying off the statement balance is a better idea in terms of saving money. Make sure it’s linked to a bank account you know will have enough funds to make the payment.

- Set up a small recurring charge. Putting a subscription on your card means you’ll always have activity on it, even if you don’t use it for the month. This is useful since your first card will be your oldest later down the line, which you’ll want to keep open for the sake of your credit score, even after you’ve moved on to other cards.

Months 2 to 6

Once your first month is complete, the next half of the year should focus on keeping your card balance relatively low and building a positive payment history.

From months two to six of using your new card, you should:

- Keep your utilization low. Card utilization is the ratio of your card balance to your credit limit. Keeping your balance and utilization low will help boost your credit score and help you avoid getting into debt. For example, if your credit limit is $600, then you’ll want to keep your balance below 30% ($180) or, ideally, 10% ($60).

- Pay off your balance in full. Paying off your balance fully each month means you can avoid paying interest and continue to keep your utilization low. Contrary to popular myth, you don’t need to keep a balance from month to month to maintain your credit score or keep your card open.

- Keep an eye on your spending habits. Don’t spend more than you can comfortably pay off when your balance comes due. If you notice that you’re starting to overspend, set some limits for yourself and pull back on using the card.

Months 6 to 12

In the latter half of the year, you can start to branch out a bit more.

- Request a credit limit increase. Many companies will grant you an increase if you’ve consistently made payments, or if you’ve recently increased your income.

- See if you can upgrade your card. If you have a secured card and are in good standing with the card company, you may be eligible to upgrade to an unsecured card and receive your deposit back.

- Consider getting a second card. If your credit score is in good shape, you may want to consider getting a second card with different or better perks.

- Keep your first card open. If you qualify for a second card, don’t close the account. Keeping your first card open will keep the credit history on it open and help increase the average age of your score.

Common mistakes

There are many myths and misconceptions around credit cards, which can hurt you and your credit score in the long run. We clear them up and answer your common questions here.

"Should I have 5 cards or 1?"

While it’s fine to have multiple cards, when you’re just starting out, stick to one card. Applying to multiple cards at once will pull down your credit score, and early in your credit history, you’re not likely to qualify for many. Juggling multiple credit cards with multiple payments, limits, and due dates can also be a lot to handle as a credit newbie.

Later down the line, when your score improves and you gain experience with using (and paying off) a card, you can start applying for more cards with different perks.

"Should I carry a balance to build credit?"

No. You don’t need to carry a balance to build credit. Carrying a balance can increase the amount you pay in interest and hurt your utilization ratio. Paying off the balance is better for you in the long run, and won’t hurt your score.

What’s important to keep in mind is keeping your card open with regular activity, even if it’s a small, monthly subscription that you pay off each month. If you go for too long without using your credit card, the card issuer may close the account, which will cause you to lose the history on the card and hurt your credit score.

"Will applying hurt my score?"

Your score will decrease by a few points when there’s a hard inquiry on your account. This dip usually lasts for less than a year, and shouldn’t prevent you from enjoying the advantages of using a credit card.

What is important to keep in mind is that multiple inquiries in a short amount of time can pile up quickly, which is why you should space out applications.

"What if I get denied?"

Getting denied isn’t a judgement on you or your finances. It can happen for any number of reasons, including having too low a credit score or income, the credit card issuer having high standards, or you having a thin credit file.

When you get denied, you’ll be sent an Adverse Action Notice within 30 days of your denial, which will outline exactly why you got denied. From there, you should review your credit report, shop around for cards you’ll have a better chance of getting approved for, and see if you’re prequalified.

To speed up the process, it’s a good idea to have a “backup” card you can apply for if you don’t qualify for your first card, such as a secured card, or becoming an authorized user.

How Monarch helps once you have your card

Keeping track of your transactions, balance, payments, and credit score happens all in one place on the Monarch platform, making managing your credit card a seamless part of your financial plan.

Once your card is activated, you can link it to Monarch, where you can immediately start tracking your transactions and payments. You can view your balance, your available credit, and your statement balance all in one place, making it easy to keep an eye on your utilization ratio and how much you’ll need to pay. Monarch will also notify you if you go over a certain threshold in your utilization that you set (such as 30%).

You can also keep ahead of your card bills with Monarch. The platform can securely sync with your credit account so you can see your due dates, minimum balances, and balance owed in one place, with alerts and notifications so you never have to miss a payment.

Having a budget in place is a major part of managing your card responsibly, which you can do with Monarch’s budgeting and tracking options. You have options for setting up a category or flex budget in the platform based on your budgeting style. Your card transactions link directly to your budget and set categories, making it easy to track your spending and make sure your balance doesn’t get too large to pay.

If you’re keeping an eye on your credit score, Monarch has it covered. You can track the progress of your VantageScore on the Monarch dashboard and see how your score has changed from month to month.

Finally, if you do have a balance you need to pay off, Monarch can help you tackle your debt productively with pay down goals, which helps you set a timeline based on your monthly payments and interest and link your payments to your budget.

When you're ready to manage your card alongside the rest of your money, Monarch puts your card balance, statement due date, credit score, and budget in one view — so you actually see what's happening all in one place.

Your first card is the foundation. Use it like one.

Choosing your first credit card isn’t a light decision. It can form the foundation for your credit score, what lending products you have access to, and how you’re able to access services from apartment rental to booking a hotel. Make sure to weigh the pros and cons of your first credit card choice, make sure you keep your spending and balance manageable, and make your payments on time. If you do, your credit score will grow, and you’ll enjoy the benefits for years to come.

FAQs

What's the difference between a secured and unsecured credit card?

A secured credit card requires a cash deposit, which is held by the card issuer and can be used to pay the balance of the card if the card holder misses a payment. Secured cards, as such, tend to have low limits and low or no credit requirements. Unsecured credit cards, on the other hand, don’t require a deposit, though they usually have higher credit and income requirements.

What credit score do I need to get my first credit card?

For your first credit card, you technically don’t need a credit score at all, since many starter cards are built to be accessible for users with low or no credit. These cards do tend to have low limits, high APRs, deposit requirements, and limited rewards, If your score is fair-to-good (around 650+), you'll qualify for cards with better terms.

Can I get a credit card with no credit history?

You can. Many secured and student cards come with no credit requirements, so long as you either provide a deposit or provide proof of income. These cards do often come with additional requirements (such as being a full-time student or providing a security deposit), higher APRs, and lower limits, however.

How long does it take to build credit with my first card?

Usually about six months to a year. Your first payments will start reflecting on your credit reports at around six months for your FICO score, which is the most commonly used scoring model for credit and lending companies. After six months, your score grows from payment history and utilization. With a positive year of history, you can apply for a second card or upgrade your current one.

Can I get a credit card without a job?

If you have a regular source of income, such as through a side hustle, a trust fund, regular allowance or stipend deposits (specifically if you’re under 21), financial aid or scholarships, or retirement/investment income, you can use this as income to qualify for a card.

If you don’t have regular income, you may have a harder time qualifying unless you provide a security deposit on the card or have a co-signer.