Credit card debt can happen to anyone. According to the Federal Reserve, Americans now owe $1.28 trillion in credit card debt, with the average cardholder balance being $6,523. Often, credit card debt comes not from overspending but from emergency expenses. According to Bankrate, 17% of Americans would pay for a $1,000 emergency expense with financing from a credit card.

While credit card debt can feel overwhelming, it is possible to pay it off. By strategizing your savings, developing a debt management plan that works with your financial situation and personality, and by creating a budget geared toward debt repayment, you can tackle your balances and become debt-free in your lifetime.

A Quick Guide to Paying Off Credit Card Debt

Here’s a quick overview of the debt repayment strategies we cover here.

- The debt snowball

- The debt avalanche

- Balance transfer credit cards

- The debt defrost

- Debt consolidation loans

We also touch on bankruptcy, debt settlement, and other options you may be considering in your repayment journey.

Why Credit Card Debt Grows So Fast

Credit card debt has a way of ballooning out of control quickly for three key reasons: High compounding interest, low minimum payments, and the fact that it’s revolving.

One of the biggest factors in out-of-control credit card debt is compounding interest. Credit card interest tends to be on the high side, hovering at around 24% as of March 2026, according to LendingTree.

On the baseline, for every $1,000 of debt, you’ll be paying $240 per year. However, this number is often higher because of compounding interest.

Credit card companies will charge interest on a daily basis according to your balance. With an APR of 24% and with a balance of $1,000, you’ll be charged about 66 cents on the first day.

The next day, you’ll be charged interest on not only the baseline balance, but also the interest you were charged on the previous day. This applies to each day, with the interest charged slowly increasing with the balance. By the end of 90 days, your daily interest charge has crept up to 70 cents. At the end of a year, assuming you haven’t made any minimum payments, you’ll have paid a total of $271.15 in interest.

Moreover, credit card APR tends to be variable, which means your interest rate may increase or decrease with market fluctuations, meaning you won’t know how much interest you’ll be charged later.

In addition, unlike fixed-term loans, which have a set amortization period where you know how many payments you need to make, and when your loan will be paid off, credit card debt is revolving, which means the balance can increase as you pay it off if you continue to make purchases with the card. One month you may have a $2,000 balance. Six months later, even if you’ve been making payments, the balance may be at $3,000 with additional charges and interest.

The Minimum Payment Trap

When you have a balance on your credit card, your credit card company will require you to make a minimum monthly payment on the balance. While they will adjust the monthly payment amount based on your balance and interest rate so you can hypothetically pay off the balance over time, usually it would be over a period of 20 or more years, so it’s not the smartest strategy.

Let’s say you have $6,000 in credit card debt with an APR of 24%. Your minimum monthly payment is the card’s APR plus 1% of the balance, or $180.

If you pay the minimum monthly payment, you’ll pay off your balance in about 25 years (303 months), with $11,332.22 in total interest, or nearly twice the original balance. This is assuming that your rate doesn’t increase, and that you don’t incur any additional charges that contribute toward the balance.

Instead of relying on minimum payments, it’s a better idea to strategize your debt repayments.

5 Proven Strategies to Pay Off Credit Card Debt

Paying off debt strategically will help you organize your payments and pay off debt in an efficient way, while saving you on interest and getting you debt-free sooner. There are a few different strategies to choose from.

Before You Start

Before you begin aggressively paying off debt, there are a few things to take care of. Taking these steps will make your repayment smoother and help you choose the strategy that works best for you.

- Take inventory of the cards you have, their interest rates, the minimum payments, and what you owe. This will help you keep track of your repayments and inform which strategy you decide on.

- Keep spending strictly within your income. Use your budget to curb your spending so you don’t end up racking up new debt.

- Pay off any new balances each month. If you’re still charging your cards, keep track of your spending, and make sure to pay off any new balances in full.

- Have an emergency fund in place. Before you start paying off debt aggressively, save up at least $1,000 or one month’s worth of net income if you haven’t already. This will give you a cushion if you lose income or get hit with an unexpected expense.

- Get your employer’s 401(k) match. Leaving free money on the table can hurt you in the long run, so if all your debt has interest rates below 25%, make sure you contribute enough to get up to 6% of your salary matched by your employer. If your interest rates are higher than 25%, you can pause your contributions until you pay down the debt with those extra high rates first.

- Make sure you have basic insurance. This includes car, house/renter’s, and medical insurance at the minimum amounts. This will help guard you against any catastrophic expenses you may incur during your repayment process.

- Watch your credit score. Keep an eye for any new balances or credit lines, and make sure there aren’t any missed payments pulling it down.

Figuring Out Your Debt Hierarchy

Not all debt is created equal, and, as mentioned above, debts with higher interest rates can quickly spiral out of control. As such, you should prioritize your repayment strategy around your debts in this order:

- Level 0 (Highest priority): Debts at 25% interest or higher, which you should focus on aggressively paying down.

- Level 1 (Middle priority): Debts at 10% to 25% interest, which you should try to refinance or transfer to a low interest balance transfer card.

- Level 2 (Lowest priority): Debts at 10% interest or lower, which you can focus on paying off last, after reaching any other more important financial goals.

Since credit card debt for the average American is often at Level 0, you’ll typically want to prioritize your card balances above all other types of debt when choosing where to focus your repayments.

With that said, here are some general and popular repayment strategies to consider.

The Debt Snowball Method

The debt snowball is a good starting point if you feel overwhelmed by your debt and want to start paying off balances quickly.

To start, choose the card with the lowest balance and focus-fire any extra cash you can find toward paying off the balance, while still paying the minimum payments on your other cards. Once the balance is paid off, you roll the payment of the paid-off balance into the next-lowest balance, “snowballing” your payments as you pay off each card.

Keep in mind that even with the snowball method, you should still take your interest rates into consideration. If you are using the snowball method, consider grouping different balances by interest rate, and focus on paying off smaller balances with higher interest rates instead of the bottom-line smallest balance.

The Debt Avalanche Method

The debt avalanche method is more efficient than the snowball method, and will save you more on interest. However, it doesn’t always come with the quick “wins” offered by paying off your balances quickly.

Like the snowball method, you’ll be rolling the payments of each paid-off balance into the next one as you pay them off. However, instead of going in order by lowest balance size, you start with the balance with the highest interest rate and work you way down. This saves you more on interest in the long run, though you may be stuck paying down a larger balance for a long time instead of quickly paying off balances like the snowball method.

Balance Transfer Credit Cards

If you have a good credit score, you may qualify for a balance transfer card. Balance transfer cards allow you to transfer the balance of one or more cards onto a new card with a low or 0% introductory APR. This allows you to focus on paying down your balance for the introductory period, which is usually three months to a year, without accumulating interest.

Qualifying for a balance transfer card usually requires a credit score of FICO 670 or higher, with a better score qualifying you for cards with longer introductory periods or more rewards. If you’re paying off multiple balances, or have missed payments in the past, it may be difficult to have a high enough score to qualify. This brings us to the next method.

The Debt Defrost Method

With this method, you can use your payment history and available credit to boost your credit score enough to qualify for a balance transfer card.

Begin with either the snowball or avalanche strategy, and pay down your balances to 30% or less of your total available credit limit on each card.

This will boost your credit score as you lower your utilization ratio. Then, once your credit score is high enough to qualify for a balance transfer card, apply for one or more and transfer your remaining balances in order of highest to lowest interest rate, allowing you to pay off the remainder of your debt without worrying about compounding interest for the introductory period.

Debt Consolidation Loans

An alternative to a balance transfer is using a debt consolidation loan. This loan bundles your different balances into one loan by paying off the balances with the money you borrow. In the case of credit cards, this can often snag you a better interest rate if you have a good credit score.

While there are specific credit card consolidation loans offered by lenders, you can also take out a personal bank loan and use the cash to pay off your balances. Keep in mind that you will be charged fees for origination and administration, and your credit score may take a hit with the hard inquiry.

An important thing to keep in mind: at Monarch, we do not recommend using a debt consolidation loan to refinance credit card debt if you are still actively using the cards, since this can often lead to increased debt and endless debt paydown cycles in the long term.

Other Ways to Help Pay Down Credit Card Debt

Besides the strategies above, there are a few other ways you can manage your debt and make repayments a bit easier.

Negotiate a Lower Interest Rate

If you’re a consistent customer with your credit card company, and have made your payments on time, see if you can request a lower interest rate. Card companies prefer to retain their customers, especially if they pay consistently. If you indicate you’re thinking of transferring your balance to a different account, they may be willing to cut you a deal.

Some credit card companies also offer financial relief or hardship programs where they lower your interest rate for a set period of time, usually 1-5 years, if you qualify based on life circumstances. However, you typically cannot use the credit card during that time, you may not have access to the card features or benefits, and any reduction in your credit limit will be reported to credit bureaus and could affect your credit score.

Increase Income and Redirect Windfalls

The more money you put toward your debt repayments, the faster you’ll pay off debt and the more you’ll save on interest. Here are a few ways to increase your cash flow.

- Take advantage of windfalls. If you get an inheritance, a tax refund, or other one-time cash bonus, take 90% and put it toward your debt repayments. Use the rest for something fun, so you don’t feel like you are restricting yourself too heavily.

- Start a side hustle. Tutoring, ride sharing, selling crafts and baked goods, or doing some landscaping work can all boost your income.

- Sell old gift cards. If you have a gift card for a restaurant or store you don’t go to, see if you can sell them on a trusted, third-party marketplace.

- Declutter and sell your stuff. Old clothes, toys, books, and games can net you some cash, especially if they’re collectibles.

- Share your space. Consider taking on a roommate or renting out part of your living space such as a garage or parking spot to bring in extra rental income.

How to Build a Budget that Actually Pays Off Debt

Your budget and debt repayment go hand in hand. A budget will help you map out your expenses for the month so you know you have enough to cover the essentials, while still giving you some wiggle room for unexpected expenses and “fun” things. Here’s a quick guide for building a budget.

Figure Out Your Cash Flow

Your income will help you determine how much you can put toward your debt repayments and will set the tune for the rest of your budget. Map out how much post-tax income you’re bringing in each month. If you have any irregular income (such as side hustle income) list that separately, and don’t use it as a baseline

Once that’s done, list out your average expenses for each month, and whether you’re breaking even, have some money left over, or if you’re in the negative.

Prioritize Your Essentials

With debt repayment, making your debt payments is a must-have on your budget, alongside housing costs, utilities, and basic groceries. Since these payments come first, you’ll want to adjust your spending accordingly for other, non-essential categories.

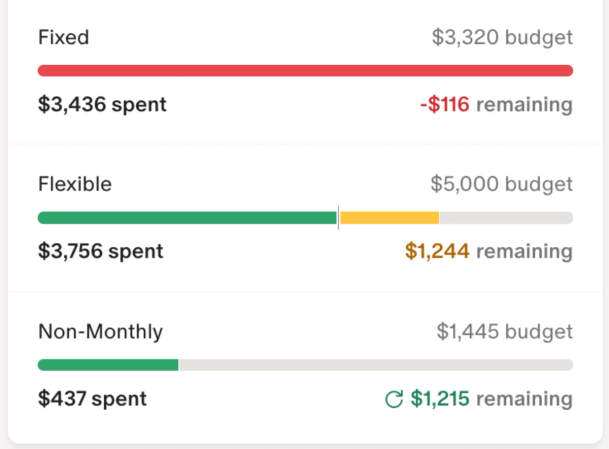

How you prioritize your essential expenses will depend on your budgeting style. If you use a category budget, you’ll divide your categories into “needs” and “wants” and set your parameters and limits from there. With a flex budget, debt repayments and other essentials would fall in the “fixed” category, since the payment is the same each month.

See Where You Can Cut Spending

If your income isn’t lining up with your essential expenses, or if you want to dedicate more cash to your debt repayments, you can use your budget to adjust your projected spending in other categories. This might mean reducing your housing expenses, trading in your vehicle for one with a lower monthly payment,, lowering your grocery budget by shopping at discount stores, cutting some subscriptions, or skipping out on a vacation.

At the same time, be sure not to completely shave your budget down. If you can, give yourself a little bit of wiggle room for fun. Debt repayment is a marathon, which means you’ll want to pace yourself throughout the process and give yourself some room to breathe.

Check In Frequently

Stay on top of your budget throughout the week and the month. Checking in frequently will help you stay on top of your spending and make sure you’re sticking to your budget limits, so you can pace your spending accordingly.

Monarch Pro Tip: Monarch makes budgeting easy, with pre-set categories and flex budget options that automatically log your transactions and help you keep on top of your finances in the background. Our swipe to review feature on the mobile app makes reviewing transactions a breeze, and dare we say, even a little bit fun!

When to Get Professional Help

Tackling credit card debt doesn’t have to be something you do alone. Here are some resources you may want to consider if you’re struggling with managing your debt and paying it off.

Credit Counseling and Debt Management Plans

Credit counseling companies help you organize your debt repayments by offering financial education, and by giving you an avenue to bundle your payments through a debt management plan. When working with a credit counseling company, you’ll make one payment to the company, which will then make payments to each of your creditors on your behalf, through what is called a “debt management plan”.

Often, credit counselors are able to negotiate a lower interest rate with your credit card company, allowing you to save more on your payments. However, you’ll usually have to close any lines of credit you include in a debt management plan, which can hurt your credit score and leave you less wiggle room in emergencies. Typically plans will take three to five years to complete. While credit counseling companies can charge fees, they may waive or discount them if you meet a need threshold.

Credit counseling can be a good option if you feel overwhelmed by debt and don’t know where to start. You can find certified credit counseling companies through the National Foundation for Credit Counseling.

Debt Settlement

Debt settlement, also known as debt relief, is when you or a debt settlement company negotiates with your creditors to forgive part of your debt. This can be an option if it’s becoming difficult or impossible for you to make the minimum payments on your balances, or if you feel your debt is growing faster than you can pay it off.

When working with a debt settlement company, they will typically recommend that you stop making repayments and that you let your balance go to collection. From there, they will negotiate with the debt collectors to reduce part of the original balance in exchange for you repaying the remainder. You’ll then make payments to the settlement company, typically encompassing your debt repayments and a fee for the company.

While debt settlement companies may feel like a good option if you’re struggling with repayments, it can tank your credit score, since the process will cause you to miss payments for a long time without any guarantees that the card company will accept a settlement offer. Moreover, you may be required to close your cards and/or be banned from applying for new cards with your credit card companies if you go through the settlement process. Finally, you’ll have to pay fees through your repayments, which means you might not be saving much money.

Weigh your options before going through debt settlement, and be sure to know what you’re getting into before you apply.

Bankruptcy

Bankruptcy is a legal process where you establish to your creditors that you are unable to repay the debts, and want to start anew by having the debt written off. You may have your assets (such as your house, car, and other personal property) auctioned off to pay off the balance, though depending on the type of bankruptcy you file for, you may be able to avoid this.

There are two types of personal bankruptcy to know about

- Chapter 7 bankruptcy involves selling off your assets to pay your debt, the remainder of which is discharged once all your assets are sold. This is known as liquidation.

- Chapter 13 bankruptcy reorganizes your debt into a repayment plan that takes three to five years to complete, with the remainder being discharged.

Bankruptcy comes with filing and court fees, which can add up over time. Hiring a lawyer isn’t required, though it can be helpful if you need guidance through the process. Once the process is complete, expect your credit score to take a massive hit. Bankruptcy stays on your report for seven to ten years, so be sure to seriously consider other options before opting to file.

What Happens to Your Credit Score as You Pay Off Debt

As you pay off your credit card debt, you can expect your credit score to change over time. While you might expect your score to improve, the process isn’t quite as straightforward.

The Good

Paying down credit card debt improves your score in a few key ways. Firstly, paying off your balance improves your utilization ratio, which will increase your score. Making on-time payments will improve your payment history, and keeping your old cards open will increase your pool of available credit and boost your average age.

In a nutshell, you’ll boost your score by:

- Paying down balances

- Making payments on time

- Keeping old lines of credit open

The Bad

Depending on how you go about it, paying down your balance may drop your credit score. The biggest impact is if you decide to close a card after you’ve paid the balance. Not only will this increase your utilization ratio, since you’ll have less available credit, but you’ll also lower the average age of your accounts.

If you miss any payments, if any of your payments goes to collections in the process of settlement, or if you file for bankruptcy, your score will take a big hit, which can stick around for seven to ten years.

Finally, if you apply for a consolidation loan or a balance transfer card, expect your score to drop by a few points from the hard inquiry. Fortunately, this should drop off of your report after a few months.

In a nutshell, you’ll reduce your credit score by:

- Closing old accounts

- Missing payments

- Conducting hard inquiries for loan or card applications

- Filing for bankruptcy

The Misconceptions

Since credit scores have multiple factors that go into them, there are a few common misconceptions that can hurt you in the long run. We’ll clear up some of them here.

- Avoid closing old cards unless you absolutely need to. Closing cards won’t boost your score and can instead hurt it. Keep old cards open either by using them and paying off the balance, or keeping a small subscription on it and paying it off monthly. You can freeze your card if you are worried about anyone fraudulently using the available credit.

- You don’t need to carry a balance to maintain your score. Paying off your balance in full each month will boost your score and save you on interest.

- Missed payments can stick around even after you’ve closed the card. Closing a card or paying off the balance won’t erase any missed payments on your report.

Paid off debt balances will still stick on your report. This means you can benefit from the positive payment history for a few years.

How to Stay Debt-Free After Paying Off Your Cards

Once you’ve paid off your debt, staying ahead of your spending so you can avoid debt in the future is vital. Here are a few tips.

Stick to Your Budget

The key to avoiding overspending is to stay within your means and to curb your expenses before they get out of hand. This is where a budget comes in handy: By planning out how much you can afford to spend ahead of time, you can put a cap on your purchases before they go over your limit and leave you in debt.

If needed, go with a budgeting style with stricter limits and parameters, like a zero-based budget or the envelope method. You can even set limits on your cards and charge accounts that prevent further expenditures if you go over the threshold.

Check in on your budget frequently, and make sure you’re staying on track throughout the month.

Monarch Pro Tip: You can take Monarch on the go with the Monarch mobile app, allowing you to check your balances, budget limits, and transactions from anywhere.

Have an Emergency Fund

An emergency fund is a vital lifeline against debt, since you can draw on your fund instead of your credit cards should an unexpected expense or loss of income arise. According to a Bankrate survey, 29% of Americans have more credit card debt than emergency savings.

While you should have a small emergency fund of about one month of take home pay on hand during your debt repayment journey, once you’re finished with repaying debt, focus on increasing your emergency fund to have at least three to nine months of average monthly expenses.

Monarch Pro Tip: You can use save up goals to establish a saving goal for yourself, track your contributions, and watch your balance grow.

Remove the Temptation to Spend

If you find that credit cards and charge accounts cause you to go beyond your means:

- Pay in cash or debit only. Having a hard limit will help you pull back on purchases.

- Block retail and shopping sites. Physically removing the temptation to shop can help you keep your spending in line.

- Set alerts and limits on your card. You can request that the credit limit on your card is lowered, or set notifications if your spending goes over a certain threshold.

- Resist applying for new cards. Even if the sign-on bonus seems like a sweet deal, if you find yourself racking up charges on your new card, it might not be the best idea.

Monarch Pro Tip: You can set alerts on your budget that notify you if you’ve gone over a certain limit, keeping you accountable.

Set New Goals to Build Wealth

Once you’ve paid off your cards, use the money from your payments wisely. While it’s okay to splurge here and there, using your former debt repayments to build wealth will go a long way and help increase your net worth. You can do this by:

- Increasing your contributions to your 401(k) or IRA accounts

- Contributing to an education investment account like a 529

- Opening a brokerage account to invest for medium to long term goals

- Putting your cash into a high-yield savings account for short term goals

- Building equity by buying real estate or paying off your mortgage

- Starting a business that generates extra income

- Increasing your earning power through education or career coaching

The earlier you invest, the more money you’ll make over time, as you’ll be taking advantage of compounding interest.

Monarch pro tip: Keep track of your assets and accounts in the Monarch app, which updates frequently as your investments grow, allowing you to track your growth and your net work all in one place.

Using Monarch for Debt Repayment Success

Monarch helps you stick to your debt repayment plan with a dynamic budgeting system that works for your lifestyle and financial goals. No matter how much debt you have, or where you are in your repayment journey, Monarch is with you every step of the way.

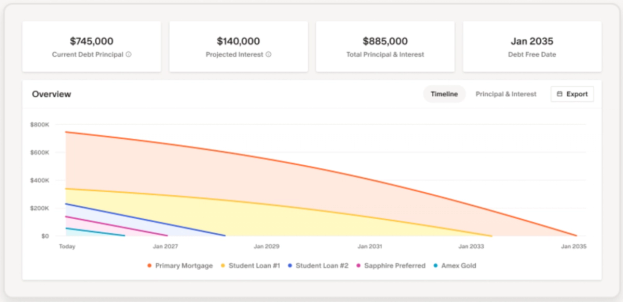

Monarch makes it easy to keep track of your debt and your repayments with the debt dashboard, which allows you to link your accounts and balances for dynamic updates as you pay down your balance. If you’re making extra payments, or want to see how much a one-time cash infusement will put you ahead of schedule, you can create a forecast for your timeline.

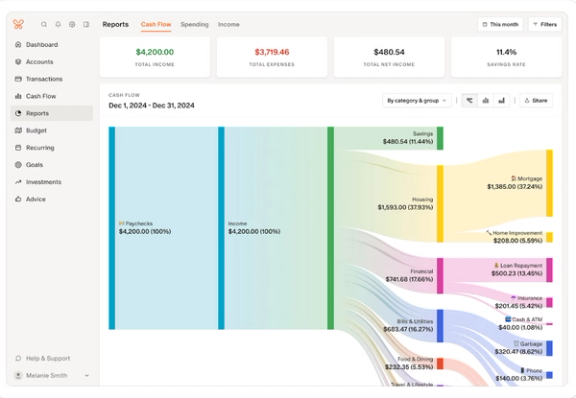

Monarch’s budgeting tools offer a seamless way to manage your finances, with account linking for automatic transaction logging. There’s no need for spreadsheets. Instead, simply set your rules for transaction categorizing, review transactions as needed, and watch your budget fill up.

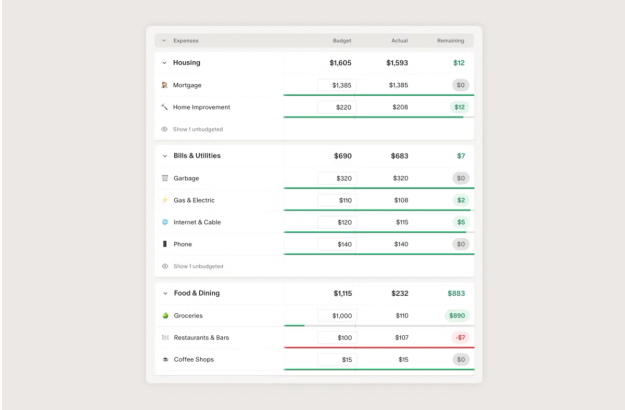

You can choose the way you want to budget with Monarch. If you prefer more detail, you can go by categories, with Monarch offering pre-set categories and options to add more.

If you want a more flexible approach that doesn’t require as much oversight, you can choose the Flex budget style, which categorizes your expenses based on whether they’re fixed, variable, or non-monthly. With both styles, you can make your debt repayments a priority, ensuring you have enough cash to make them.

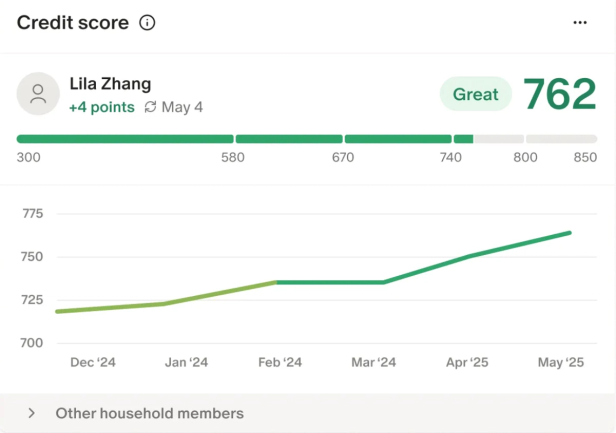

Finally, Monarch offers credit score monitoring, allowing you to keep an eye on your score as you make payments and pay down your balance.

Get Debt-Free Faster with the Right Plan and the Right Tools

While credit card debt can feel overwhelming, it doesn’t have to take over your life. Strategizing your debt repayments, building a budget that works for you, and staying dedicated to your repayment plan can help you make your payments on time, save on interest and pay off your debt sooner than you think. Using resources like credit counseling can also help you if you’re overwhelmed.

No matter where you are in your journey, Monarch is with you every step of the way. With dynamic budgeting, a real-time debt dashboard, and tools to help you make the most of your cash flow to pay off your debt, Monarch can help you become debt free.

FAQs

What is the best way to pay off credit card debt?

The avalanche method is the most efficient for paying off debt quickly and saving on interest. The snowball method is slightly less efficient, though it provides a bit more motivation as you’re paying off individual balances in quick succession. Which one you decide to go with is up to you.

How long does it take to pay off credit card debt?

It will depend on your balance, your interest, and how much you are able to contribute to your payments. With compound interest, making the minimum payments can take you months or even years. However, going beyond your minimum payment and using debt repayment strategies like the avalanche method can make the process much faster.

How much credit card debt does the average American have?

According to TransUnion, the average cardholder’s balance is $6,523.

Should I use savings to pay off credit card debt?

Be careful when doing this. If you have extra cash beyond your minimum emergency fund of one month of take home pay, you can use it to pay off your balances. However, don’t drain your emergency fund completely, or you may find yourself needing to take on debt again if you face an unexpected expense.

Should I close a credit card after paying it off?

Be cautious when doing so. If you want to avoid the temptation to charge on it, you can freeze the card online with your card company or literally, in a block of ice in the freezer. However, you’re better off keeping your account open, spending a small amount each month, and paying off the balance in full, since closing cards can drop your credit score.

Can I negotiate a lower interest rate?

You may be able to if you’re a consistent payer and good credit card customer. Contact your credit card company and see if you qualify for a lower rate. Otherwise, consider taking out a consolidation loan or a balance transfer card with a better APR.

What is the 7-year rule for credit card debt?

Payment history for your debt – include both positive and negative remarks – will vanish from your credit report after seven years. This can cause your score to change slightly, though, ideally, you have other accounts that will help you maintain your score.