Every dollar matters, which is why it’s crucial to know where every dollar is going. If you have an irregular income and you want to make sure you’re keeping strictly to your means, or if you want a high amount of detail into your spending and don’t want any of your hard-earned cash to go astray, zero-based budgeting might be for you.

Zero-based budgeting is a strict budget style that assigns a destination for every dollar you make, from saving to spending. While it’s not the style for everyone, and can come with downsides, the structure and boundaries it provides to your spending can help you accomplish your goals and get disciplined about where your money is going.

This guide covers what a zero-based budget is, the pros and cons, who it works for, and how Monarch can help you build one.

What is Zero-Based Budgeting (ZBB)?

Zero-based budgeting is a budget style where your total income minus saving and spending equals zero. ZBB assigns a specific purpose to every dollar that comes in. With this method, you’ll justify and track each expense. This is a highly precise method of budgeting that sacrifices flexibility.

Zero-based budgeting can be a powerful tool not only for managing your spending, but helping you reach your financial goals. You can prioritize your savings, pay down debt by budgeting for extra repayments, and manage your overall financial picture in a detailed way that can help you grow your net worth and making sure your money is going where it has the most impact.

A Brief History of ZBB

Author Peter Pyhrr created zero-based budgeting in the 1960s. Also known as zero-dollar budgeting, he developed it for business use while working as a manager at Texas Instruments in Dallas. Then-governor of Georgia Jimmy Carter later adapted it for government and public sector use, eventually adapting it to the federal United States budget when he was elected president.

Radio personality Dave Ramsey later popularized the method for personal use, especially for individuals with overspending habits or who needed more structure to their budgeting.

How to Build a Zero-Based Budget: A Step-by-Step Guide

Building a zero-based budget requires attention to detail and a good pulse ona clear picture of your monthly expenses. We’ll break it down for you in six simple steps.

Step 1: Figure Out Your Take-Home Pay

To start, add up all of your regular take-home income, including salary, disability or Social Security, and retirement disbursements.

If you happen to make more or less than your usual income for the month, then you can adjust your budget later on (more on this later.)

Step 2: Figure Out Your Expenses

Next, list out your expenses for the month. Calculate the totals of what you typically spend, and divide out your expenditures into categories, such as groceries, utilities, entertainment, subscriptions, and so on.

Step 3: Divide Your Pay Out

Once you have your categories and your rough expense totals, assign each of your categories a dollar amount. Take into account both your income and your usual monthly expenses when you do this. For example:

- Rent: $1,580

- Insurance: $65

- Auto payment: $250

- Student loan payment: $200

- Groceries: $400

- Entertainment: $50

- Savings: $100

It can be helpful to assign out your essential expenses first, so that you can prioritize having enough funds for those, and dedicate the remainder to less-critical categories.

As well, be sure to include a “buffer” category for when your expenses are more than expected, like getting a bigger-than-expected electricity bill after a heat wave.

Step 4: Make Sure Your Math Works

Once you’ve assigned out your categories, make sure that you haven’t gone into the negative or the positive. The key goal is to make sure you hit zero.

If you have some money left over, you can either redistribute it among your categories, put it towards savings/investments, or add it on to an existing debt repayment.

If you need to reorganize your expenses, you may want to “freeze” certain categories if you can’t or don’t want to change the amount you’ve already assigned. Then, organize your spending around the remainder.

Step 5: Keep an Eye on Your Spending

If you need to make adjustments because of a lower income, be sure to account for spending that you’ve already done in each category, and if there are any “frozen” categories that you can’t change. If you’ve gone over, then pull from your buffer category, or from categories you haven’t yet spent the limit on to make the difference.

If you need to pull from your savings for a non-monthly expense or an emergency expense, consider your withdrawal a one-time “salary” bonus, and assign the expense appropriately.

Step 6: Review Your Month and Start Anew

Once the month is over, it’s time to rebuild your budget. You can use last month's budget as your starting point as a baseline for your expenses, especially for fixed expenses that don’t change from month to month.

The key with rebuilding your budget is making sure that every single dollar is accounted for. This is especially key if your salary changes from month to month, or if your expenses tend to be variable. By tracking every single dollar, you’re making sure you know where your money is going and that you don’t rack up debt, miss on savings goals, or overspend your income.

Zero-Based Budgeting Example

Here’s an example of how a zero-based budget gives every dollar a job.

This zero-based budget is based on a monthly income of $4,840.

Rent | $1,350 |

Utilities | $250 |

Car payment and insurance | $500 |

Student loan repayment | $450 |

Groceries | $400 |

Gas | $150 |

Subscriptions | $40 |

Clothing | $50 |

Restaurants/Eating out | $150 |

Gifts | $100 |

Savings | $700 |

Investment | $500 |

Buffer | $200 |

TOTAL | $4,840 |

Zero-Based Budgeting with Irregular Income

If your income varies from month to month, a zero-based budget is ideal for making sure you’re not spending too much in one month and not leaving enough for your lean months.

There are a couple of ways to do this. If you get paid at the end of the month, you can base your “salary” for your budget of the previous month’s income, ensuring you don’t spend more than you’ve already made.

The other way is to calculate your average monthly earnings based on the previous year, and to pay yourself a fixed “salary” for yourself each month, with a rigid budget that reflects that. In months where you make more than your “salary,” you earmark the remainder for savings. In leaner months, you would draw upon your savings to bring you up to mark.

Pros and Cons of Zero-Based Budgeting

Zero-based budgeting isn’t for everyone. It’s generally best if you’re struggling to stop overspending, if you have irregular income, or if you generally want a lot of structure in your budget. Looking at the pros and cons can help you decide if ZBB is right for you.

Advantages of Zero-Based Budgeting

- Accounts for every dollar you spend

- Can be helpful for irregular incomes

- High amount of structure

- Can help you pay down debt

Disadvantages of Zero-Based Budgeting

- Inflexible

- Takes a lot of work

- Easy to go off track with variable expenses

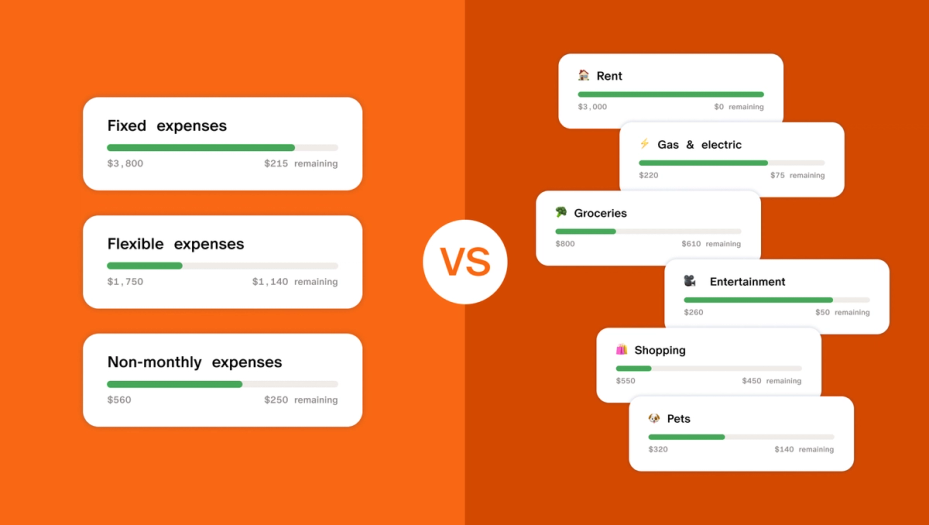

Zero-Based Budgeting vs. Other Budgeting Methods

Zero-based budgeting is only one of many budgeting strategies available. If you’re considering ZBB, here are a few ways it compares to other methods.

Zero-Based Budgeting vs. the 50/30/20 Rule

The 50/30/20 rule is when you assign 50% of your income to needs, 30% to wants, and 20% to savings and investments. While you can assign individual categories a dollar amount, in general, it’s less detailed than a zero-based budget.

Zero-Based Budgeting | 50/30/20 |

Strict allocation to designated categories | More open-ended with how you allocate funds |

High amount of structure and detail | Less structure and detail |

Requires a high degree of planning | Requires a lower degree of planning |

Best for managing overspending or an irregular income | Best for structure with some flexibility |

Zero-Based Budgeting vs. the Envelope Method

The envelope method is similar to the zero-based budget in that you divide out your income into categories with set limits. In the envelope method’s case, each “envelope” receives a set amount, with a hard limit on how much you can spend out of the envelope once the funds run out. The envelope method does allow for a bit of flexibility, as you can move funds between envelopes as needed.

If there are any funds left in the envelope after the month, instead of being dedicated to a “job” like the zero-based budget, they can be rolled over into next month’s envelope or put into savings.

Zero-Based Budgeting | Envelope Method |

Highly structured with hard caps on spending | Highly structured with hard caps on spending |

Strict allocations for where money goes | More flexible allocations for where money goes |

Leftover funds are assigned a category | Leftover funds can be moved, saved, or rolled over |

Best for managing overspending or an irregular income | Best for managing overspending |

Zero-Based Budgeting vs. Reverse Budgeting (Pay Yourself First)

A reverse budget, or the Pay Yourself First System, is the ultimate flexible budget. With this budgeting system, you pay yourself first by setting aside money for savings and investments, and then allocate the rest to your usual bills and expenses.

Compared to a ZBB, reverse budgeting is extremely flexible and doesn’t require as much structure or planning. While this can be great if you want a more open-ended budget, if you find yourself overspending or not having enough to cover your bills at the end of the month, then a ZBB might be better for you.

Zero-Based Budgeting | Reverse Budgeting |

Focused on managing overspending | Focused on prioritizing saving |

Highly rigid and structured categories and caps | Highly flexible in where you allocate your spending |

Requires intensive planning | Requires fairly minimal planning |

Best for managing overspending or an irregular income | Best for flexibility and saving/investing |

Tips for Sticking to Your Zero-Based Budget

Staying on track with a zero-based budget takes discipline and a bit of forethought. Here are our top tips for keeping to your budget.

- Track in real time. Use platforms like Monarch to track your transactions as they happen, giving you live information on your spending.

- Set alerts for overspending. Set threshold alerts on your card and budgeting apps that will notify you if you’re getting close to your category limits.

- Review your budget weekly and monthly. Frequent check-ins will help you keep an eye on your income and categories and allow you to readjust as needed.

- Limit yourself to physical cash. If you’re having a hard time managing expenses on your card, consider bringing physical cash when you go out, which will present a physical limit on your spending.

- Build a support system. Let your friends and family know that you’re keeping your spending in check, and advocate for activities that will help you stick to your budget, like a picnic in the park instead of eating out.

- Have an emergency fund in place. An emergency fund will give you a buffer that you can draw upon when you face an unexpected expense, leaving your categories and plan intact.

- Give yourself room for fun things. Even on a strict budget, it’s important to give yourself a fund to have fun. Managing your spending in this way is better than trying to get rid of it entirely.

How to Build a Zero-Based Budget in Monarch

Monarch can help you build a zero-based budget with ease. Here’s how.

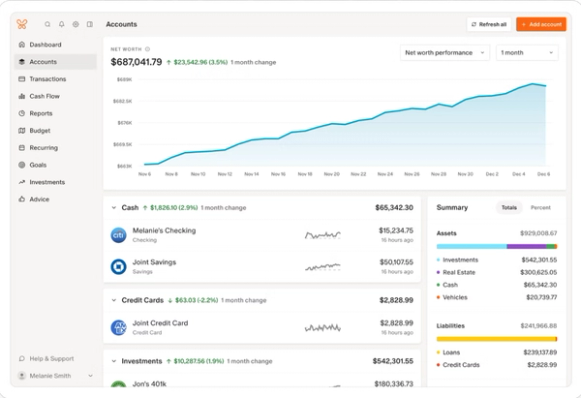

Link Your Accounts

Your first step is to link your bank and card accounts. Be sure to link your charge accounts and the accounts where you receive your pay. Monarch will track your transactions and log them, automatically applying them to your budget.

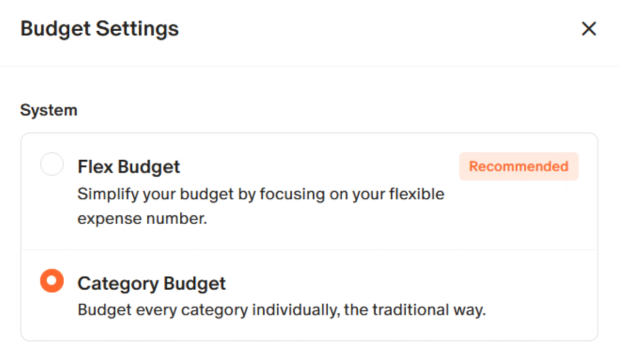

2. Select the Category Budget Option

Next, go to your budget tab, select Settings (the little gear in the top-right corner) and select the option for category budget.

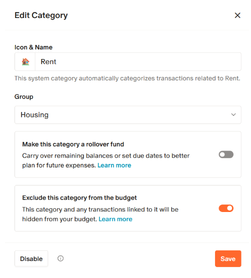

3. Select Your Categories

Next, choose the categories you want to budget for. Monarch has 60 default categories to choose from , with options to edit the names and icons. You can also add custom categories.

If you don’t want to use a default category, you can remove it from your budget by clicking on the gear next to the name.

Monarch will assign categories based on your transaction merchants. You can review transactions by clicking on each category, and change the category and rules by clicking on the transaction.

4. Assign Dollar Amounts

Once you have your categories set, you can assign your budgeted amount to each category by clicking on the text box next to the category name.

Depending on your transaction history, you can get historical data of how much you have spent on each category in the past to help inform you.

As you budget out your categories, Monarch will inform you of how much you have left to budget, allowing you to track how much you have left to allocate.

5. Track and Adjust as You Go

Once you have your budget and expenses set, you’re good to go. Monarch will track your transactions for you and alert you if you’ve gone over any of your parameters. You can access Monarch on your desktop or through the mobile app, and keep an eye on your categories to make sure you’re not going over.

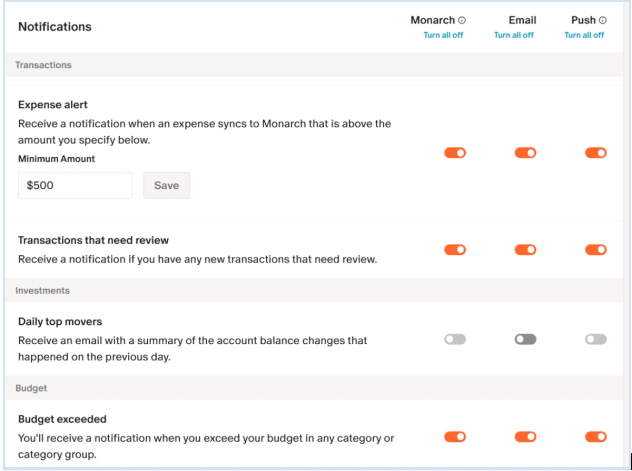

You can add custom alerts and notifications for when you exceed your budget, or when a transaction goes above a certain threshold, in the main settings option to the top left under “Notifications.”

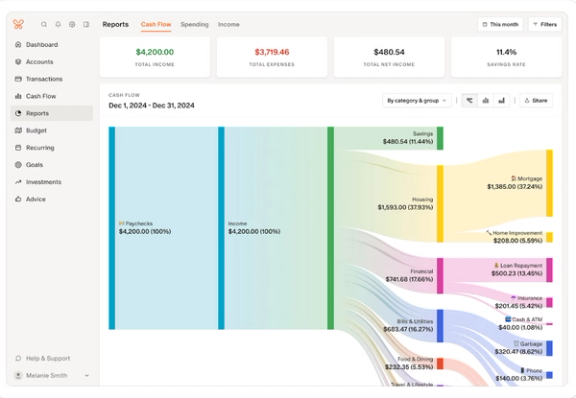

If you need to adjust a category, you can edit your budget any time from anywhere. For big-picture analysis, Monarch offers monthly reports and cashflow at a glance to keep you informed about how much you’re saving each month, and where your money is going. You can also project your cashflow and expenditures into the next month, allowing you to plan ahead.

If you want to make a zero-based budget backed by data, with dynamic tracking and tools tailored to your personal style, plug your accounts into Monarch, launch your categories, and see where it can take you.

The Bottom Line: Is Zero-Based Budgeting Worth It?

Zero-based budgeting, while work-intensive and highly structured, can be a good way of managing your finances when you need to make every dollar count. Because all of your income is accounted for, a ZBB can help you manage overspending and designate funds for essentials, savings, and the things that matter to you.

FAQs

Does zero-based budgeting mean I spend all my money?

Not necessarily. While you need to assign a place for every dollar, you can designate funds to savings or investments. In fact, it’s a good idea to set aside some cash each month to contribute toward your emergency fund or other financial goals.

How do you make a zero-based budget?

In a nutshell: calculate your monthly income, figure out your monthly expenses and categories, and distribute every dollar of your income to your planned expenses and savings, making sure there’s nothing left over.

What categories should a zero-based budget include?

While it depends on your needs, you should include categories for the expenses you plan on having for the month, including the mortgage/rent payment, utilities, groceries, gas, debt repayments, subscriptions, entertainment, and so on. You’ll also want to dedicate a category to savings and investments, as well as a “buffer” category in case you need to dedicate extra funds to a category.

Can I use zero-based budgeting with irregular income?

It’s actually well-suited to this, since you have to be aware of how much income you’re working with and make sure you don’t exceed what you’re bringing in. You can base your budget on the month’s previous income, the month’s expected income, or an average you calculate based on historical data.

How is zero-based budgeting different from the 50/30/20 rule?

The 50/30/20 rule has much looser categories and more flexibility in how you allocate your dollars, with more broad categories and no specific dollar amounts dedicated to any one purpose.

Is zero-based budgeting the same as the envelope system?

Not quite. While the envelope system does have hard limits on spending, it generally works with the assumption that you might have some funds left over, which can be rolled over into the next month or saved. Zero-based budgeting is much stricter, and with every dollar dedicated to a specific purpose, with nothing left over.

How does Monarch support zero-based budgeting?

With a robust category budget structured to help you track every penny of your spending, Monarch can help you build a detailed category budget that aligns with your zero-based budgeting strategy, with a category budget setting that tracks your spending against your parameters, and that allows you to put as much detail into your budget as you need to.