Key Takeaways

- Flex budgeting combines flexibility and structure by organizing your expenses into three buckets: Fixed, Non-Monthly, and Flexible

- Your Flex Number determines how much you can allocate into your flexible expenses category, allowing you to prioritize big purchases and monthly essentials while giving you wiggle room

- Flex budgeting works well if you don’t want to intensively plan out multiple categories each month or are having trouble following a traditional budget

- Monarch supports Flex Budgeting on the platform and offers tools for estimating expenses, managing spending, and integrating your budgeting with your overall financial plan

Giving yourself a budget is one of the best things you can do financially. It can keep you on the same page with your partner. It can help you be intentional about where your money is going and confident that you’re reaching your goals. Finding a budget that fits your style plays a big part in sticking to your financial plan – and sometimes, a traditional budget with dozens of categories just doesn’t cut it.

There’s a simpler way to build a budget that can help you manage your expenses and help you contribute toward your goals. Flex budgeting gives you the structure to prioritize your needs and manage irregular expenses, with enough wiggle room to spend on what matters to you.

Flex budgeting is one of Monarch's core budgeting types, and it's helped thousands of people manage their finances on the platform and build a holistic financial plan that meets their long-term goals. Here’s how you can make it work for you.

What is Flex Budgeting?

Flex budgeting is a way to simplify your finances by focusing only on your flexible spending. These are the expenses that go up and down each month, like groceries, entertainment, and restaurants whether they’re necessities or just for fun.

Other expenses, like monthly bills and goals you’re saving for, you can set and mostly forget, because for the most part, you decide in advance how to spend on those.

For everyday spending, you get one high-level number to track. We call this your “flex number.” All you have to do is check your progress toward your flex number throughout the month, and you’ll know if you’re on track or if you might want to adjust your spending.

This is unlike traditional budgeting, also known as “category budgeting.” With that method, you assign every expense category a budget and track your spending toward each budget. This includes all your expenses, not just the ones that go up and down each month.

Flex Budgeting in One Formula

Your flex number is the key to your flex budget, acting as one of the core “buckets” of spending outside of your fixed and non-monthly expenses. Depending on those expenses, your flex number will change month to month, so you will want to re-calculate appropriately.

To calculate your monthly flex number:

Subtract your fixed expenses, non-monthly expenses, and goals from your income.

Income - Fixed Expenses - Non-monthly expenses - Goals = Monthly Flex Number

Let’s put it into an example. Say your monthly household income is $6,400. You have $2,000 in fixed expenses for your mortgage, utilities, subscriptions, and so on. You plan on spending $1000 on replacing your car’s tires. You’re also putting aside $200 to save toward your vacation fund.

With this, your monthly flex number would be $3,200 ($6,400-$2,000-$1,000-$200=$3,200).

It’s also helpful to break down your budget week by week by having a weekly flex number. This helps you manage your spending in a more gradual way, and helps you keep a pulse on the trajectory of your budget and cash flow.

To calculate your weekly flex number:

Simply divide your monthly flex number by 4.3. This is because 52 weeks divided by the 12 months in a year is 4.33, which will give you a more accurate idea of a month’s length than dividing by four.

Monthly Flex Number ÷ 4.3 = Weekly Flex Number

Using our previous example, $3,200 ÷ 4.3 is about $744.19.

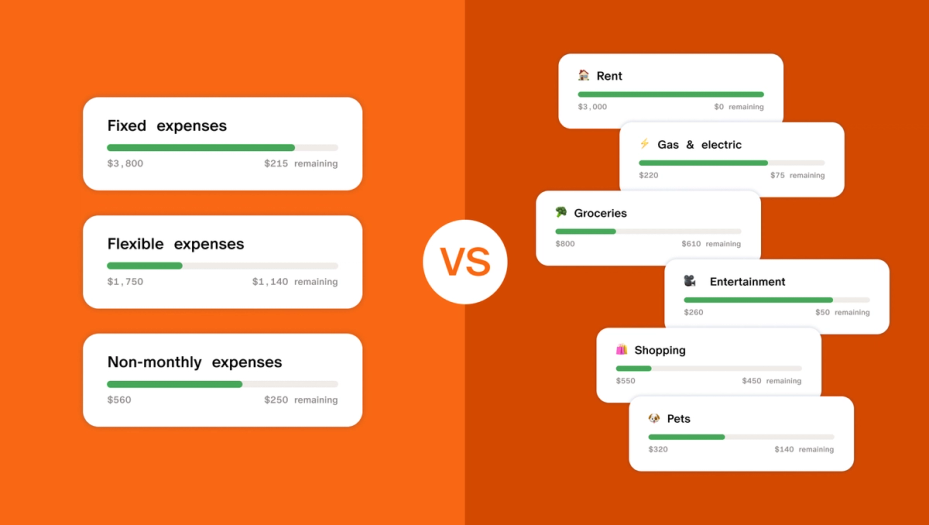

The Three Buckets and Your Goals

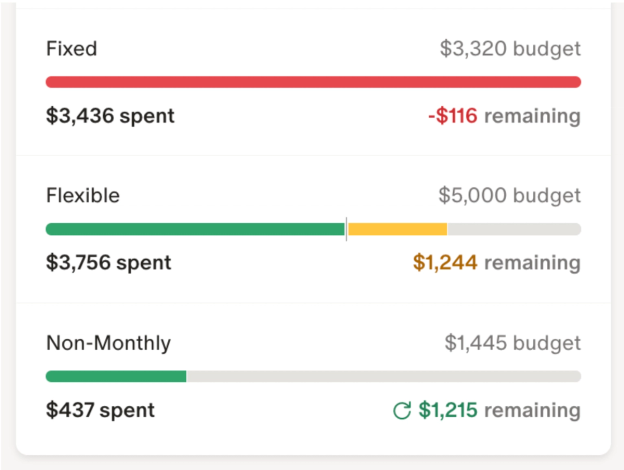

Flex budgeting is defined by the three buckets you set up for your expenses. Here’s the breakdown of what goes into each bucket.

Fixed Expenses

Your fixed expenses are your most predictable, since you pay them each month. The amounts might vary a little like electricity, phone, or subscription boxes or stay the same, like your rent or mortgage.

- Rent or mortgage

- Monthly insurance premiums

- Minimums on your loans or other debts

- Gym memberships

- Subscriptions of all kinds

- Utilities

- Phone

- Automatic monthly donations to charity

- Childcare

Non-Monthly Expenses

These are the bigger expenses. You know they’ll come at least once a year, but they either don’t happen every month or vary widely from month to month. They’re also often known as “sinking funds” or “irregular” or “periodic expenses.” Common non-monthly expenses include:

- Taxes

- Gifts

- Getting your car worked on

- Home repairs

- Travel

- Annual donations to charity

- Annual subscriptions

- Annual or semiannual insurance

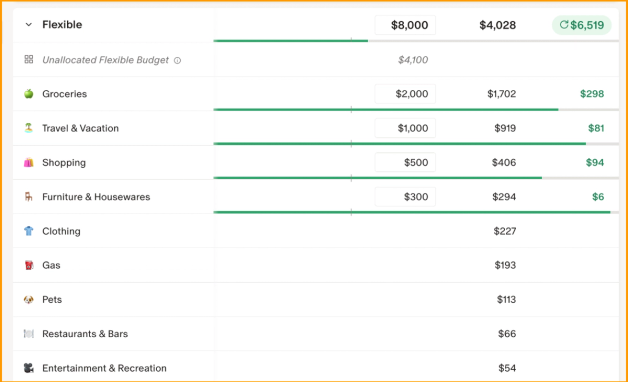

Flexible Expenses

These are the expenses that are hardest to predict, but easiest for you to control. You could pay more or less for them in a week or month; or you can even go without some of them.

Some of your flexible expenses are needs (like groceries) you'll probably have to buy each month. Others could be things you want but didn't budget for anywhere else. If you have a big unplanned expense that isn’t an emergency and can't be covered by savings, try to cover it with flexible spending. Common flexible expenses:

- Groceries

- Gas

- Medical copays

- Shopping

- Restaurants

- Entertainment

- Hobbies

Goals

While goals and non-monthly expenses can both be big and unpredictable, they’re different. You know you’ll have non-monthly expenses at least once a year, but goals are typically the bigger life targets that you’ll need to save or invest toward for a while. Sticking to your flex number helps you save more every month toward your goals and your their targets faster.

Monarch recommends having these financial goals, in order of priority:

- Build your emergency fund to at least $1,000

- Add to your emergency account so it covers 3 to 12 months of expenses

- Maximize your retirement contributions to meet your employer match or higher

- Start aggressively paying off debt with over 25% interest

- Contribute to an education savings plan like a 529

- Save for a big purchase, like a home down payment or a vacation

How to Build a Flex Budget in Monarch

Flex budgeting is one of Monarch’s core budgeting types, making it easy to set up and maintain as part of your overall financial plan. Here’s how to do it.

Link Your Account and Transactions

Your first step is to link your spending and saving accounts, which will allow you to track your transactions and to keep an eye on your balances. Monarch can do this securely through the website or the app.

If you’re budgeting with a partner, you can add them to your household and have them link their accounts, allowing you to see both of your transactions and include both your incomes in your cash flow report.

Linking your accounts will also give you the first number you need to calculate your flex number: Your total income.

Sort Your Buckets

Next is to figure out which of your expenses go into your Fixed, Non-Monthly, and Flex. First, figure out which categories (e.g. groceries, housing payments, utilities) go in which bucket. Then, categorize your transactions so they are sorted into each bucket.

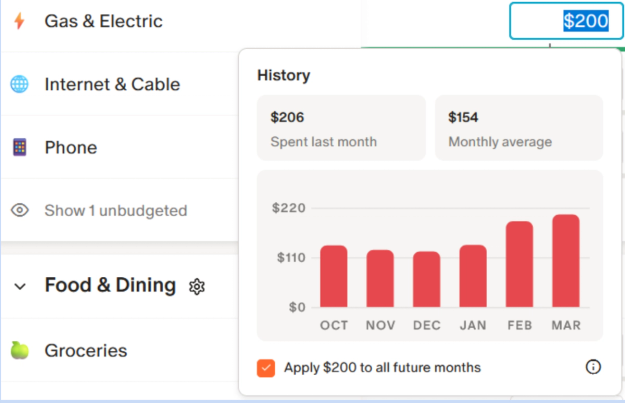

Monarch helps you save time on this in a couple of ways. Firstly, it automatically categorizes your transactions based on the merchant, allowing you to quickly sort through your transactions and put them in the appropriate buckets. It also suggests how much to budget for each category based on your spending history.

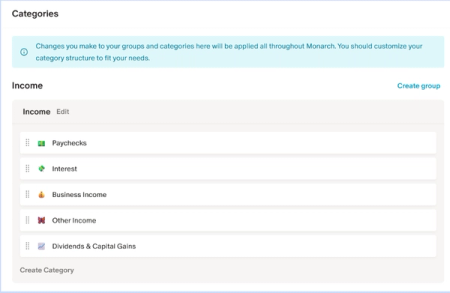

Finally, it will automatically sort your categories into your different buckets. You can re-order which categories go where by going into “Settings” and clicking on “Categories.” From there, you can also disable certain categories that you don’t use, or add a new category.

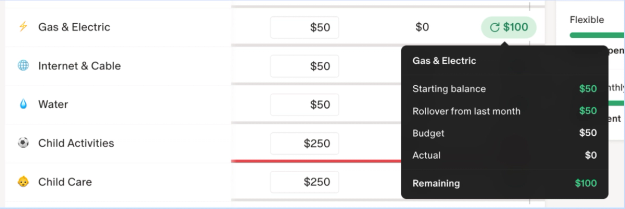

Once you’ve sorted your transaction buckets, you’ll be able to see what your fixed monthly expenses are, and budget out what your planned non-monthly expenses are. If you’re planning on saving over time for a large purchase, you can build a “sinking fund” by using the rollover option, which allows you to roll over any unspent funds into the next month if you enable it on the category.

Decide on Your Goals

Next is to decide on your financial goals and how much you want to contribute. Goals are their own budget category and bucket.

You can set a goal in Monarch for paying down debt or a balance, or for saving up for something. Once you’ve set your target number, you can link an account to your goal to track your payments, and link the goal to your budget, allowing you to track your goal spending in your budget and watch your goal progress in your goals tab.

Set Your Flex Number

Once you’ve figured out your income, buckets, and goals, it’s time to calculate your flex number.

Monarch will do this automatically for you once you’ve established your buckets and goals. However, if you want to do it manually, then you can use the flex formula below:

Income - Fixed Expenses - Non-monthly expenses - Goals = Monthly Flex Number

Set a Tracking Schedule

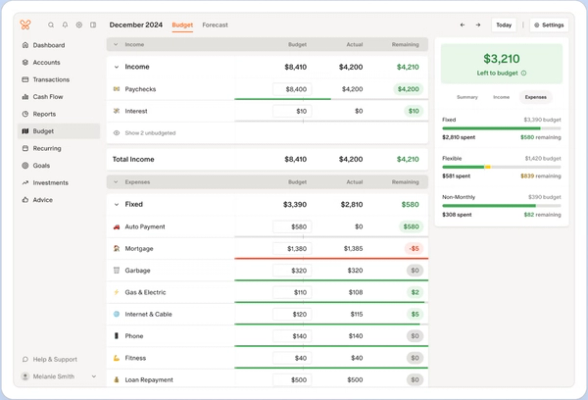

With your budget set, Monarch will automatically track your transactions and your thresholds so you can see how your spending lines up with your budget and your goals. In order to get the most accurate pulse on your finances, Monarch recommends checking in on your budget on a weekly basis, and offers a weekly view of your spending with your weekly flex number.

If you’re budgeting as a household, Monarch also offers separate flex numbers for each member.

Monarch helps make your budget meetings productive by giving you a quick overview of how your spending is tracking. At a glance, you can tell where your budget stands by the color: Green for spending under 50%, yellow for 50% to 99%, and red for 100% or over your budgeted amount.

Review and Adjust

Beyond weekly and monthly check-ins, it’s a good idea to review your budget on a quarterly and yearly basis. You’ll want to do this for a few reasons:

- Check in on your numbers. Make sure your income and fixed expenses are the same, and make adjustments as needed.

- Forecast your non-monthly expenses. Check on your annual subscriptions or big purchases you’re planning on, and add them to the appropriate month’s budget.

- Review your goal progress. Make sure you’re hitting your benchmarks and see if you need to contribute more. If needed, set new goals.

Flex Budgeting vs Other Methods

Trying to choose between flex budgeting and another method? Here’s a quick breakdown of how they compare.

Flex Budgeting | Category Budgeting | 50/30/20 Budgeting | Zero-based Budgeting | |

How It Works | Three-bucket budgeting where you categorize expenses into Fixed, non-monthly, and flex expenses | A budget of individual categories with a set amount allocated to each one | Expenses are divided into three categories: 50% of income is dedicated to Needs, 30% to Wants and 20% to Savings/Investments | Strict budgeting where every single dollar of your monthly income is dedicated to a purpose, whether it’s for spending or saving |

Key Features | Flexible spending structure that offers limits without intensive planning | Individual category limits that require more planning and offers more spending insight | Flexible style category budgeting that provides structure around spending amounts | Highly intensive in planning, with every dollar accounted for and strict spending limits |

Pros | Less intensive way of setting parameters around spending More flexibility in where your money goes Easy to follow and set up | More structure with individual limits on different categories More detail on spending plans Detailed budgeting with lots of insight with some wiggle room | Offers flexibility in exactly where your money goes Gives parameters around how much you spend on discretionary purchases Offers a structured way to save | Extremely structured with hard limits on spending Gives a solid framework for avoiding overspending High awareness of where your money is going |

Cons | Can lack structure Doesn’t offer detail into where your money is going Can be too open-ended for some | Requires more work to build Can be cumbersome to follow with the strict limits Overly rigid and strict if you want a more flexible budget | Can be too open-ended 50/30/20 proportions may not work for your lifestyle Leaves definition of “Needs” and “Wants” open-ended | Highly rigid Requires a large amount of planning May not fit with your financial style or goals |

Category Budgeting

Category budgeting involves categorizing your transactions by type and setting individual limits for each category. This means that it’s more intensive, since you have to set categories and limits for each type of transaction. On the other hand, it tends to offer more detail into your spending, and can be a good way to set hard limits around certain categories you want to cap expenses on.

How It Compares to Flex Budgeting

Category budgeting requires more work than a flex budget, since you have far more “buckets” to account for and portion out. It doesn’t have as much flexibility, and requires you to be more aware of your spending habits so you can build out and budget for your categories. For some, this is a plus, since it offers more detail.

When It’s Right for You

Category budgeting is best if you want more structure to your budget and keep a cap on expenses for certain categories. While it does require more work, if you want a detailed budget, then it might be right for you.

Monarch Pro Tip: You don’t have to stick with one budgeting style if it isn’t working for you. Monarch allows you to switch between category and flex budgets in the budget settings, so you can see which one works best for you.

50/30/20 Budgeting

50/30/20 budgeting is when you allocate 50% of your income toward your needs, 30% to your wants, and 20% to savings and investments. This kind of budget can work well if you aren’t sure where to start or need a basic structure for your spending and saving without having to categorize every transaction. Because of the set percentages, however, it can be a bit inflexible for certain lifestyles. If you live in a high-cost-of-living area, or if you have a low income, you may not be able to keep your needs to 50% of your income. Additionally, there may be times you want to allocate more than 20% of your income to savings, like when you’re trying to catch up on retirement contributions.

How It Compares to Flex Budgeting

50/30/20 budgeting can be a more structured kind of flex budget, offering more rigid parameters around the percentages of your spending while giving you flexibility in exactly where your wants and needs spending goes toward. It does require a bit more work in terms of defining your needs and wants categories, though you don’t necessarily need a category for everything.

When It’s Right for You

This type of budget can work best if you’re looking for a flex budget with a bit more structure to it. By setting parameters around how much you’re saving and spending on needs and wants, it can be a good “starter” budget if you’re not sure about where to start or how to set your savings goals. It also works best if you’re able to keep to the percentages.

Zero-Based Budgeting

Zero-based budgeting offers a strict budget plan by allocating every single dollar of your income toward a specific purpose, whether it’s spending, saving, paying off debt, or otherwise. It’s a highly intensive type of budgeting since it needs every dollar to have a “job,” which requires a fair amount of planning and detail.

How It Compares to Flex Budgeting

Zero-based budgeting is almost opposite of flex budgeting in terms of the work required and the limits set. It requires a high amount of planning and doesn’t offer much flexibility in where your money goes, while offering a high amount of detail into your cash flow and expenditures.

When It’s Right for You

Zero-based budgeting can work well if you need a budget with a large amount of detail and if you want to set strict parameters and limits around your spending. It can work well if you have an irregular income, or if you’re trying to set strict limits on your spending.

Common Flex Budgeting Mistakes (and How to Fix Them)

While flex budgeting offers simplicity, there are a few mistakes you can make that can throw your plan off. Here’s what to know, and how you can fix it.

Forgetting Irregular Expenses

Sometimes you get lost in the bustle of the day-to-day and forget your irregular expenses, which can throw your monthly budget off when your annual subscription renews or when your tax bill comes due.

The Fix: Plan out your budget not only for the month, but for the year. Mark out which months you are planning on a big expense, and either set it up in your budget or set a reminder for yourself on your calendar. Even if you don’t know the exact numbers, it’s good to bookmark it so you can set it aside ahead of time.

Planning ahead will help you set your budget and financial plan trajectory for the year to come. You can set up your monthly irregular expense amounts up to two years ahead in Monarch.

Mixing Up Your Frequencies

Sometimes expenses aren’t on a strict month-to-month or yearly basis. For example, you might have a subscription that renews every three months. This falls into a bit of a middle ground, where your expense isn’t necessarily irregular, but doesn’t fall into the neat lines of a monthly expense.

The Fix: Set up your budget on a monthly basis and make sure to include recurring expenses ahead of time. If you know when they’ll be renewed, set them up in your budget ahead of the fact.

When setting up your non-monthly budget in Monarch, when adding an item, you can set the frequency to “variable” so you can manually set aside how much you need each month instead of it automatically renewing.

Setting Your Flex Number Too High

While flexibility is great, it is possible to set your flex number too high and not leave yourself enough room for your essential expenses or saving for your goals.

The fix: Review your goals and your overall financial plan, and make sure you’re achieving your long-term goals. If your retirement account isn’t where it needs to be for your age, if your emergency fund needs an update, or if you haven’t got a life insurance policy in place, then it’s time to adjust your flex number and make some room for your goals.

Not Separating Your Flex Money

If you’re drawing from one bank account for all your expenses, it can be easy to lose track of how much of your flex fund you have left, leaving you at risk of running out before the end of the month.

The Fix: There are two approaches you can take. One is physically separating your flex money in a separate account or card, and transferring (or setting a balance limit of) your flex number for the month. If you’re using a financial management platform like Monarch, you can set notifications for when you reach certain thresholds on your flex spending, such as when you have spent 50% of your flex funds.

Not Updating for Life Changes

While flex budgeting can be great for planning ahead, forgetting to factor in changes in your income or fixed expenses can throw your budget off.

The Fix: Make sure your flex number is still reflective of how much your income is and what your fixed expenses are. If your income changes, or if your fixed expenses go up or down permanently, then it’s time to recalculate.

Trying to Force Flex Budgeting When It’s Not Your Style

Everybody has a different style of managing their finances. While there are many perks of flex budgeting, for some, the open-ended nature of this budget doesn’t provide the parameters they want, or offer details into their spending.

The Fix: Try a different budgeting style and see if it works for you. If you want more detail into your spending, you might want to try a category budget. If you want to path out every dime of your income to a purpose, then try zero-based budgeting.

FAQs

What is flex budgeting?

Flex budgeting is a type of budgeting that categorizes your spending into three buckets: Fixed expenses, non-monthly expenses, and flexible expenses. The last category is set by your flex number, which is how much you have left of your income after allocating money toward your fixed expenses, non-monthly expenses, and goals.

How do I calculate my flex number?

Take your monthly income and subtract your monthly fixed expenses, non-monthly expenses, and goal allocations.

Should my flex number be weekly or monthly?

While your monthly flex number will set the tone of your overall monthly spending, a weekly flex number can help you keep an eye on your spending trajectory and make sure you’re keeping your flexible spending in check. You can calculate your weekly flex number by dividing your monthly flex number by 4.3.

Is flex budgeting the same as a flexible budget in accounting?

Not quite. A flexible budget in accounting terms is usually applied to businesses, and is used to build a budget that adjusts to the business’ month-to-month or quarter-to-quarter expenses. Flex budgeting, on the other hand, is for individual, personal budgeting.

What expenses belong in the flexible bucket?

Any expenses that don’t fall under your fixed or non-monthly expenses. This can include groceries, entertainment, and restaurants.

How do I handle non-monthly expenses in a flex budget?

You can put them in the “Non-monthly” bucket of your budget. It helps to plan ahead of time if you know you have a large purchase coming up.

Does flex budgeting work with variable income?

It can, though it will take a bit more work. You’ll want to re-calculate your flex number each month, using your expected income as the baseline.