A mortgage, on paper, is a secured loan used to purchase a home. In reality, it’s one of the biggest financial obligations you'll take on — and one of the most common ways Americans build wealth.

This guide walks you through the mortgage essentials, from what a mortgage is and how PITI works, to your borrowing options, to knowing when you're ready to apply, to how Monarch can help you save for and manage your home loan.

By the end, you’ll know what to look for in a loan, how to prepare for the application and approval process, and what to expect as you prepare to purchase your first home.

Key Takeaways

- A mortgage is a loan to buy a home, with the home as collateral; the borrower repays principal plus interest over 15 or 30 years.

- Monthly payments are made up of PITI: principal, interest, taxes, and insurance.

- Five main loan types exist: conventional, FHA, VA, USDA, and jumbo — each with different minimum down payments and credit-score requirements.

- The median down payment in 2025 was 19% for all buyers and 10% for first-time buyers (NAR).

- As of May 20, 2026, the average 30-year fixed mortgage rate is 6.36% and the 15-year is 5.71% according to the Freddie Mac Primary Mortgage Market Survey.

- Monarch helps members track every part of the mortgage journey — from saving for a down payment, to running scenarios in the Mortgage Calculator, to monitoring when refinancing or cancelling PMI would save real money.

What is a mortgage?

Mortgages are key tools for building wealth and establishing homeownership. According to the U.S. Census, in 2024, 60% of all homes in the United States were owned through a mortgage. With 82% of Americans believing homeownership to be a core part of the American dream, according to a Bankrate survey, a mortgage can be a stepping stone to growing your net worth and building stability for you and your family.

A mortgage is a loan used to purchase a home that’s paid off over a fixed number of years, with the home as collateral for the loan. If the loan is paid off in full, you have full equity (or ownership) of your home. On the other hand, if you fail to make payments, the lender can foreclose on the home and sell it to make back the balance of the debt.

With a bit of preparation and knowledge about how the mortgage process works and how to choose the right loan for you, you can use your home loan to your advantage and take one step further to becoming a homeowner.

How does a mortgage work?

Before you start applying for a mortgage, there are a few key mechanics behind mortgages you should know about.

Amortization

The process of paying down a mortgage is known as amortization, which allows you to pay off your loan in a series of fixed, consistent monthly payments that guarantees the interest will never grow to a point where you’re making perpetual payments.

For example, let’s say you purchase a $400k home with 10% down and a 6.36% interest rate on a 30-year mortgage. For the first six months, your principal and interest payments will look something like this:

Total Payment | Interest | Principal | Balance Remaining | |

Month 1 | $2,242.40 | $1,908.00 | $334.40 | $359,665.60 |

Month 2 | $2,242.40 | $1,906.23 | $336.17 | $359,329.43 |

Month 3 | $2,242.40 | $1,904.45 | $337.96 | $358,991.47 |

Month 4 | $2,242.40 | $1,902.65 | $339.75 | $358,651.72 |

Month 5 | $2,242.40 | $1,900.85 | $341.55 | $358,310.18 |

Month 6 | $2,242.40 | $1,899.04 | $343.36 | $357,966.82 |

Notice how the interest payments are much larger than the principal payments. This is because your balance is at the highest point it will be in the loan’s lifetime. You are also obligated to pay the lender the interest owed, which means that the interest payment takes priority.

While this may seem worrying, it’s not the case for the entire duration of the loan. Eventually, your principal payments will overtake your interest payments, to the point where, in the final six months of the mortgage, your payment breakdown will look like this:

Total Payment | Interest | Principal | Balance Remaining | |

Month 1 | $2,242.40 | $70.00 | $2,172.40 | $11,035.92 |

Month 2 | $2,242.40 | $58.49 | $2,183.91 | $8,852.00 |

Month 3 | $2,242.40 | $46.92 | $2,195.49 | $6,656.52 |

Month 4 | $2,242.40 | $35.28 | $2,207.12 | $4,449.40 |

Month 5 | $2,242.40 | $23.58 | $2,218.82 | $2,230.58 |

Month 6 | $2,242.40 | $11.82 | $2,230.58 | $0 |

Your mortgage payment goes beyond your principal and your interest. You also have to add in your insurance and taxes, which we explain below.

PITI explained

Your mortgage payment is made up of four essential parts – principal, the interest, taxes, and insurance (PITI) – which are bundled into one bill that you pay each month.

Principal

This part of the payment goes to your actual loan balance. When you start making payments on your loan, your principal payments will start out small, and will usually be less than your interest payments. This will increase over time with amortization, until the majority of your payment is going toward your principal.

If you make an extra payment beyond your minimum mortgage payment, it will go toward your principal, which will help you pay off your loan faster and save you on interest.

Interest

Your interest payments will be based both on your interest rate and the remaining balance of your principal. When you start out paying your loan, your interest payments will be larger. As you pay down more of the loan, your interest payments will shrink.

You can lower the amount you pay on your PITI by lowering your interest rate, typically by refinancing or purchasing points.

Taxes

Property taxes are charged by the town or city you reside in, and are based on a percentage of the home’s assessed value, which is known as the mill rate. The tax assessment of the house doesn’t always strictly align with the appraised value, as tax assessors have different standards for evaluating home value than appraisers.

If you fail to pay your property taxes, the town can put a lien on your home or legally foreclose on it.

Insurance

Insurance covers both your homeowner’s insurance and, if you have less than 20% equity, private mortgage insurance (PMI). PMI premiums are usually 0.5% to 2% of your mortgage total per year. Once you’ve reached 22% equity, your PMI will be removed by your mortgage servicer, and you will no longer have to pay the premium. (You can also request for your PMI to be removed when you reach 20% equity, though this may require an additional appraisal and incur extra costs.)

Homeowner’s insurance is required by most lenders, as it will reimburse you (and, by extension, the mortgage company) for the cost of repairs and the loss of the home if it is destroyed in a covered event. Your premium will be based on the value of the home, its age, the area you live in, and certain features like a pool. Some insurance companies will offer discounts if you bundle with an auto insurance policy or if you have a security system in place.

Escrow

The taxes and insurance part of your PITI aren’t paid directly to your insurance company or town. Instead, they’re paid into an account held by the mortgage provider, which in turn pays the bills when they come due.

The amount of escrow you pay is based on your previous bills, which means your escrow won’t always exactly align with how much you actually need to pay. If there’s too much in your escrow, it’s known as an escrow surplus, and you’ll be given a refund by your mortgage servicer. If there’s too little, however, it’s known as an escrow shortage, and the amount short will be added to your next mortgage bill.

How much does a mortgage cost in 2026?

Mortgage costs comprise of interest and insurance rates, and how much your closing costs will total to. While how much each of these costs will depend on your balance, your credit score, and the area you live in, these updated averages will give you an idea of where to start.

Current interest rates

Mortgage interest rates are based on the Federal funds rate, which dictates how much interest banks and lenders are charged for borrowing and lending money to one another, and is one of the ways the Federal Reserve manages inflation. When the Fed rate goes up, mortgage rates increase. Conversely, when the Fed lowers their rate, mortgage rates go down.

Here’s a table of current rates in the Freddie Mac Primary Mortgage Market Survey as of May 2026.

30‑Year Fixed Rate | 15-Year Fixed Rate |

6.36% | 5.71% |

For context, here’s how much each interest rate will cost you per year per $100k of mortgage (not accounting for compound interest or amortization).

30‑year fixed rate mortgage | 15‑year fixed-rate mortgage | |

$100,000 | $6,360 | $5,710 |

$200,000 | $12,720 | $11,420 |

$300,000 | $19,080 | $17,130 |

$400,000 | $25,440 | $22,840 |

$500,000 | $31,800 | $28,550 |

$600,000 | $38,160 | $34,260 |

$700,000 | $44,520 | $39,970 |

$800,000 | $50,880 | $45,680 |

Closing costs

Closing costs are additional fees you pay in order to close on the loan and on the house. You’ll be expected to pay them with your down payment on closing day (when you sign off on the loan and the house purchase agreement), usually through a check or a wire transfer.

Typically, closing costs amount to 3% to 6% of your total loan amount, and while buyers and sellers both pay some closing costs, the buyer is responsible for the bulk of them. Closing costs vary from lender to lender, and can include, but aren’t limited to:

- Origination fee

- Underwriting fee

- Processing fee

- Appraisal

- Application fee

- Title fees

- Title insurance

- Recording fee

- Attorney fee

- Closing fee

- Courier fee

How much down payment do I really need?

Your down payment helps you get equity in your home early on, as it’s essentially paying off some of the principal of your mortgage before the term begins. It also indicates to the lender that you are serious about the loan and are diligent and have cash saved before taking out the loan.

How much you put down will depend on your goals. While loans have minimum down payment requirements, there are pros and cons to putting down more than the minimum.

Can I buy a house without a 20% down payment?

The short answer: Yes. Conventional mortgages only require a 3% down payment as a minimum for qualifying for a loan, and many government-backed loans have 0% down payment options.

Many realtors and financial influencers throw around the “20% rule” for a few reasons. First, a 20% down payment helps you avoid paying PMI. It can make your loan more attractive to lenders and give you a higher chance of being approved. It's also the typical minimum for cash-out refinancing, which gives you more options if home values rise. Finally, more of a down payment means you have less of a principal balance to accumulate interest on, which saves you money in the long run.

On the other hand, more of a down payment isn’t always to your advantage. Saving up a large down payment takes time, during which the market prices or interest rates may increase. In the time you’re saving for a down payment, you aren’t building home equity.

Many first-time home buyers put down less. According to the National Association of Realtors, in 2025 the median down payment was 19%, with first-time buyers putting down 10% and repeat buyers putting down 23%.

How your down payment impacts your mortgage

Here’s a quick breakdown of how different down payments can impact the total interest and monthly payment of a $400k, 30-year mortgage with a 6.36% interest rate.

Down Payment | Down payment amount | Principal | Monthly payment | Total interest paid |

3% | $12,000 | $388,000 | $2,417 | $482,052 |

4% | $16,000 | $384,000 | $2,392 | $477,082 |

5% | $20,000 | $380,000 | $2,367 | $472,112 |

6% | $40,000 | $360,000 | $2,242 | $447,264 |

7% | $80,000 | $320,000 | $1,993 | $397,568 |

The more down payment you put down, the more you save on total interest, and the less of a monthly payment you have. Even though a 10% down payment will cost you $28,000 more than a 3% down payment at closing, it will save you $175 a month in monthly payments and $34,788 in total interest over 30 years.

Down payments by loan total

To give you an idea of how much a down payment you’ll need to save by loan amount, we’ve crunched the numbers for you.

3% | 4% | 5% | 10% | 20% | |

$100,000 | $3,000 | $4,000 | $5,000 | $10,000 | $20,000 |

$200,000 | $6,000 | $8,000 | $10,000 | $20,000 | $40,000 |

$300,000 | $9,000 | $12,000 | $15,000 | $30,000 | $60,000 |

$400,000 | $12,000 | $16,000 | $20,000 | $40,000 | $80,000 |

$500,000 | $15,000 | $20,000 | $25,000 | $50,000 | $100,000 |

$600,000 | $18,000 | $24,000 | $30,000 | $60,000 | $120,000 |

$700,000 | $21,000 | $28,000 | $35,000 | $70,000 | $140,000 |

$800,000 | $24,000 | $32,000 | $40,000 | $80,000 | $160,000 |

PMI thresholds

Private mortgage insurance is required for mortgages with below 20% equity (ownership) of the home. This insurance protects banks in the early stages of the mortgage, and in the event of the borrower failing to make payments, will reimburse the lender for the balance owed. PMI usually costs between 0.5% and 2% of the mortgage, depending on which insurance company the lender goes with.

You can avoid paying PMI by putting down a 20% down payment, or by putting down as close to 20% as possible so you only have to pay the premium for a few months. Once you reach 22% equity, your PMI will be removed.

Using Monarch to track equity

If you have PMI, tracking your equity is essential to seeing when you can stop paying the premium. You can use Monarch’s pay down goal toolset to track your equity and see when you reach your equity threshold – and how much it will take to pay it down faster.

How to know you're ready: The affordability check

Being ready for a mortgage goes beyond finding your dream home. Here’s what to consider before you submit an application.

Hard qualifications

Mortgage companies have hard-and-fast rules when determining whether you can afford a loan based on your income, credit score, current debts, and your down payments.

- Credit history: The minimum credit score needed for most mortgages is 620. Non-conforming loans, like jumbo loans, often come with higher requirements, while government-backed loans often have lower requirements. Having a higher credit score will snag you a better interest rate. As well, lenders will look for red flags on your credit history such as previous foreclosures or bankruptcies, which may prevent you from getting approved.

- Debt-to-income ratio: This is how much overall debt payments, including your student debt, auto debt, credit card debt payments, and your potential mortgage payments, you have in proportion to your income. For example, if you make $3,000 a month and you pay a total of $1,080 to your debts each month, your DTI is 60%. Ideally, your DTI will land at or below 36%, but a DTI as high as 50% may still work depending on your credit score.

- Down payment: While you can put down as little as 3% depending on the loan, having a higher down payment will save you on interest and having to pay PMI. As well, a larger down payment can make you more attractive to lenders.

- Consistent income: Lenders will want to see that you have a steady stream of income for the previous two years, usually in the same industry or with the same company. While freelance and business income can count, you will have to provide proof through your tax forms and/or client contracts.

Documents required for a mortgage loan

When you apply for a loan, you’ll be required to provide documentation to provide proof of income and loan eligibility. While exact documentation will vary depending on the lender and the loan, in general you’ll be required to provide:

- Copies of the applicant’s ID

- Social Security card or Tax Identification Number

- Proof of income, such as pay stubs or business income statements

- Bank statements from the past few months

- Employment information from the last two to three years

- Proof of assets, including 401(k) balances and investment vehicles

- Rental history

- History of addresses/residence for the past two to three years

- Credit history and score (this can be pulled with the Social Security Number or Tax Identification Number)

- Loan statements for any other loans you may have

- Gift letters for any significant cash gifts you have received

The loss of income test

Besides the hard requirements, you’ll want to make sure you’re financially ready to manage a monthly mortgage payment. Just because a lender approves you for a certain loan amount doesn’t mean you should take out the maximum possible.

Ask yourself: If you suddenly lost your income, how long would you be able to pay off your mortgage without taking out a loan or putting it on your credit card?

While popular recommendation is three months, Monarch's guidance is that new homeowners should target six months or more, since a house comes with surprise costs the loan doesn't.

Missing mortgage payments is a high-stakes situation, since you run the risk of losing your home if you go into foreclosure. Take a look at your budget and your larger financial picture and consider how comfortably you can handle your new monthly payment, keeping in mind that you’ll have to factor in closing costs, immediate maintenance on the house, and ongoing maintenance for emergencies and upkeep.

As such, not only should you have a robust emergency fund, but you should also make sure that your mortgage payment isn’t going to squeeze your budget to the point where you can’t pay for regular monthly expenses.

If you’re applying as a couple, you have an extra question to ask yourself: If one of you lost your job, how long would we be able to manage the mortgage?

This question is especially important if you plan on having children, since one parent may want the option to stay home. Some couples manage this by getting a mortgage based on one partner’s income. This way, you can dedicate the other partner’s income to savings, and if one of you loses your job, you won’t have to dig into your emergency fund.

When deciding to buy a house, make this a money date question with your partner so you’re on the same page about how you’ll structure your budget and financial plan around your decision.

Applying for a mortgage as a couple

If you’re applying for a mortgage with a partner, you have the option of applying for a mortgage jointly or separately, and can do so whether or not you’re married. In either case, it’s critical to have a budget and financial plan together so you're on the same page about saving for and paying down your mortgage.

Joint applications consider both your credit histories and incomes, which can be helpful if both of you have a strong credit profile and want the ability to borrow more with both of your incomes. With a joint application, you are both responsible for the mortgage payment, and will both be impacted on your credit report if you miss payments or go into foreclosure.

Separate applications consider only one spouse’s credit history and income, which can be helpful if one spouse has a stronger credit report, or if the other spouse has a large amount of debt they don’t want to have considered as part of the DTI.

Only the applying spouse’s name will appear on the title and mortgage agreement, which means they have full ownership of the house. Keep in mind, however, that if you divorce or if the title-holding spouse dies, the courts will generally grant the other spouse at least part of the estate. As well, mortgage payments will only count toward the paying spouse’s history.

Do I need to be married to apply with a partner?

You do not need to be married to purchase a house with a partner. However, purchasing a house together before getting married does come with a few considerations.

- Married couples have more protections in place. If one spouse dies, the property generally automatically will go to the surviving spouse, even if their name is not on the title. If you are unmarried, you will have to file a title agreement of tenant survivorship or joint tenancy in order to establish who has the rights to the home. As well, in the event of divorce, the courts will rule the property value can be split evenly between spouses based on payments and ownership.

- If you apply jointly, you are both 100% responsible for the repayment, even if you split up. If both spouses fail to make payments, then the missed payments and foreclosure will appear on both your credit reports.

- Leaving a mortgage agreement isn’t easy. If you decide to part ways and want your name removed from the mortgage, you will have to refinance the loan, have the other owner assume liability, sell the home, or negotiate a release with your lender, all of which can come with fees and risks.

What are the main types of mortgage loans?

There are different types of mortgage loans, some of which are privately backed and some of which are government backed. These loan types have different requirements, advantages, and disadvantages, which we dive into here.

The five main types of mortgage loans

Here’s a quick breakdown and comparison of the loan types.

Amount | Best For | Requirements | Interest rates | |

Conventional conforming | Up to $832,750 | Standard borrowers with good credit history | 620+ credit score DTI of 50% or lower 3% to 5% down payment | 5.9% to 6.8% |

FHA | Up to $541,287 | First-time borrowers with lower scores | Home must be primary residence 500+ credit score DTI of 43% or lower 3.5% to 10% down payment | 6.7% to 7.3% |

VA | Up to $700,000 | Veterans | Must be qualifying US military member, veteran or spouse 620+ credit score DTI of 41% or lower 0% down payment | 6.3% to 6.7% |

USDA | Depends on area | Low-income borrowers in rural areas | Must live in qualifying rural area 580+ credit score DTI of 41% or lower 0% down payment Income no higher than 115% of area’s median income | 5% to 6% |

Jumbo | Over $832,750 | Borrowers in need of an oversize loan | 700+ credit score DTI of 43% or lower 20% down payment or higher 6+ months of cash reserves | 6.2% to 6.8% |

Conventional conforming loans

Best for: Borrowers with a strong credit profile looking for low interest rates

Conventional loans are the most common types of mortgages, and are offered by private banks, credit unions, and lending companies. There are two main types of conventional loans: Conforming loans, which adhere to the standards of the Federal Housing Finance Agency, and non-conforming, which do not.

This difference is important because conforming loans can be purchased by Fannie Mae and Freddie Mac, which are government-backed agencies that purchase loans and sell them on the secondary mortgage market, making them less risky for the lender than non-conforming loans.

Conventional conforming loans are available to anyone with a good credit score, qualifying income, and below the DTI threshold, and offer some of the best interest rates for mortgages on the market.

To qualify for a conventional conforming loan, you’ll need:

- A credit score of 620 or higher. Having a higher credit score will get you better interest rates.

- DTI of 50% or lower. Lenders typically want to see a two-year employment history, which can include prior jobs in the same field.

- A minimum down payment of 3%. Many lenders recommend having at least a 20% down payment, as it will help you avoid having PMI on your loan.

There is an upper limit to how much you can borrow with a conforming loan, which is set by the federal government each year. For 2026, the baseline limit is $832,750 for standard, one-unit homes, and $1,249,125 for one-unit homes in designated high-cost areas, with the ceiling limit being $1,873,675.

If your loan needs exceed this amount, then you may want to consider a jumbo loan (more on that later.)

FHA loans

Best for: Borrowers with mid-to-lower credit scores

FHA loans are insured by the Federal Housing Administration and offered through FHA-approved lenders for borrowers with lower credit scores. They are backed by the federal government, and you can apply through an FHA-approved lender such as a bank, credit union, or mortgage broker.

FHA loans are generally accessible to anyone. While the bare minimum credit score to apply is 500, you’ll be required to put down a 10% down payment if your score is 579 or lower. If your score is 580 or above, you only have to put 3.5% down and will likely be offered a better interest rate.

The house you are purchasing must pass an FHA appraisal, and must be free of major safety issues, have a sound structure and foundation, and have functional heating, electricity, and plumbing. Because of this, FHA loans can take longer to close, which can be a disadvantage in a hot market.

VA loans

Best for: Qualifying active duty military members, veterans and spouses

VA loans offer competitive interest rates and 0% down payment options for members of the military, and are backed by the Department of Veterans Affairs. VA loans are offered through private lenders approved by the federal government, and offer interest rates based on the market rate.

To qualify, you must:

- Meet the VA's service requirements, which vary by era and service type – the full list is at va.gov – OR

- Be a spouse of a qualifying military member or veteran

In addition, lenders will require:

- A credit score of 620 or more

- A DTI of 43% or lower

In order to apply for a VA loan, you’ll have to obtain a Certificate of Eligibility, which you can typically do online at va.gov.

Similar to an FHA loan, the house you are purchasing must be free of major safety issues such as loose railings, out-of-code construction, and asbestos or flaking lead paint. It must also have functional utilities and no issues with the foundation. Since VA inspection standards are higher than standard inspection standards and take more time to process, they can be a disadvantage in a competitive market.

In addition, you’ll have to pay a 0.5 percent to 3.3 percent funding fee with your closing costs, which can be waived if you qualify for a disability exemption through the VA.

USDA loans

Best for: Qualifying borrowers living in a rural area

USDA loans are backed by the US Department of Agriculture, and are meant to help low-income individuals purchase houses in rural areas with low credit scores and 0% down payment requirements. In order to qualify for a USDA loan, you must:

- Be purchasing a home in a USDA-eligible area

- Have an income of 115% or less of the median income for the area

- Have a credit score of 640 or higher

- Be purchasing a home for residential purposes, not commercial (such as commercial farming or renting it out)

Like with VA and FHA loans, your home will have to pass a USDA-approved appraisal and inspection.

Jumbo loans

Best for: Borrowers with extremely good credit and high borrowing needs

Jumbo loans are loans above the conforming limit ( $832,750 for standard homes and $1,249,125 for homes in designated high-cost areas). These loans are not eligible for purchase by Fannie Mae and Freddie Mac, which makes them riskier for lenders to accept. As such, they have much higher borrowing standards to meet. While requirements vary by lender, you can expect to need:

- A credit score of 700

- DTI of 33% or lower

- At least a 20% down payment

- Six to twelve months or more of cash reserves that can be used for mortgage payments

Lenders will want you to have both an extremely strong credit profile and highly consistent income. As such, expect the underwriting and income verification process to be thorough, with more documentation required than a conforming loan.

Fixed vs. adjustable interest rates

Something else to consider when selecting a loan is whether you’ll take out a fixed rate mortgage (FRM) or adjustable rate mortgage (ARM).

With an FRM, your interest rate will stay the same throughout the loan term unless you choose to refinance. An ARM, however, has a loan rate that will increase or decrease based on the market rate. ARMs often come with 3, 5, or 7-year “introductory” rates that are locked, which then switch to an adjusting rate once the period expires. The rate will then adjust based on the market every six months.

Most mortgages are FRMs, since they provide a consistent monthly payment that borrowers don’t expect to change. While ARMs can be advantageous if the market rate goes down, allowing you to save on interest without a refinance, if interest rates increase, your payment will increase.

15-year vs 30-year mortgages

When selecting a loan type, you will have the choice between a 15-year term and a 30-year term, which both come with advantages and disadvantages.

A 30-year mortgage term is the most common type of mortgage term. Key features include:

- A lower monthly payment. Since the term is longer, your monthly payments will be lower throughout the term of the loan, giving you more financial wiggle room.

- Higher interest rates. A 30-year term typically comes with a higher interest rate than a 15-year term.

- Higher overall interest paid. Since your interest rate is higher and your principal has a longer time to accrue interest, you’ll pay more in interest over the loan’s term.

A 15-year term’s key features include:

- A higher monthly payment. Because you’re paying off the debt more aggressively, your payments will be larger.

- Lower interest rates. A 15-year term typically comes with a rate 0.5 to 1.0 percentage point lower than a 30-year term

- Less overall interest paid. Since your rate is lower and your balance is being paid off more quickly, you’ll pay less total over the loan’s lifetime.

The key thing to consider when selecting your mortgage term is if you can afford the monthly payment. While a 15-year term will pay off your mortgage more quickly, if you’re struggling to make the monthly payment, it won’t do you or your finances any good – especially if you run the risk of missing a payment.

With a 30-year term, your minimum payment is lower, and you have the option to make a principal-only payment if you have extra cash, which can help you pay off your loan sooner.

You’re also not stuck with the same loan option forever. If you want to change your loan term, you can refinance the loan – though keep in mind this will come with refinancing charges and a new interest rate.

How the mortgage process works

While the mortgage process is straightforward, there are some key steps you need to take before you can sign off on your loan and take your keys.

How long does it take to get a mortgage?

The mortgage process can take anywhere between 30 to 45 days, depending on certain factors such as:

- The underwriting process. If lenders discover an issue in your credit history, are missing key information, or if you opt for manual underwriting, approval will take longer.

- The appraisal process. The lender will schedule an appraisal of the house in order to confirm the value. If the appraisal is delayed, if you request a re-appraisal, or if the home value doesn’t align with the requested loan, it will slow the process.

- Title issues. If there is a lien or title dispute on your property, it may stall the process.

- Changes in employment or financial circumstances. If you lose or change your job, open a new credit or loan account, make a large purchase, or have a large, unexplained deposit on your bank account, it may slow or halt the process entirely.

While some of these factors are out of your control, it’s important to keep a clean credit profile, have your documents and information ready, and respond quickly to any inquiries your bank or mortgage broker send to you in order to keep things quick.

With that said, here are the steps to applying for a mortgage.

Step 1: Evaluate your finances

To qualify for a mortgage, a lender typically looks at factors like your employment history, your credit report, your tax returns, and so on.

But despite the eligibility requirements outlined by a lender, it’s equally important for you as the prospective borrower to evaluate your own finances before applying for a mortgage.

“When you are trying to decide whether it’s the right time to get a mortgage, it’s not about nominal dollars,” says Braunworth. “It’s about how that compares to your financial picture.”

For instance, during the mortgage process, you’ll pay a down payment and multiple closing costs. But on top of these anticipated expenses, your home inspection could uncover repairs and maintenance needed on the house. These are all expenses to expect before you close on the loan! Once you have the keys, then you’re responsible for a monthly mortgage payment for the next 15-30 years!

“The right time to get a mortgage is when you’re ready to buy a house, and you can comfortably afford the payment,” says Braunworth. “If your income went to $0, how many months could you make this mortgage payment? As a rule of thumb, if your answer to that question is less than three, you should pause buying a house.”

In other words, a lender will do their due diligence — and you need to do the same.

Step 2: Obtain pre-approval

While you can apply for a mortgage when you decide to make an offer on a home, most buyer will get pre-approved for a loan. Getting preapproved for a mortgage makes your eventual offer on a property more competitive, because it signals to a seller that you’re capable of following through on that offer.

When you’re applying for a mortgage, it’s a good idea to shop around with at least three lenders to evaluate competing interest rates, closing costs, and other fees. A study by Freddie Mac in 2022 found that rate shopping can reduce your loan by up to $1,200 a year.

Just make sure you submit your applications within a span of 14 to 45 days, as multiple credit inquiries made in a short time are typically counted as one.

Prequalification vs preapproval

One distinction that’s important to know is the difference between preapproval and prequalification.

Preapproval is when a lender tentatively agrees to lend you a specific amount of money at a specific rate, based on details such as your income, debt, and credit score and the supporting documents. You have to submit an application for preapproval, and it’s the first step in the formal mortgage application process. It will also incur a hard inquiry on your credit report, and may take a few days or weeks to process.

Prequalification is more informal, and acts as a rough estimate of how much mortgage you can afford and what interest rate you’ll be offered based on your credit score. It entails a soft pull on your credit report, and is considered to have less standing and assurance of approval than a preapproval. As such, some sellers won’t accept an offer letter if you’re only prequalified, which makes it a better tool for rate shopping than getting your offer accepted.

Here’s a quick breakdown in summary:

Preapproval | Prequalification | |

Application timeline | Can take days or weeks | Can take less than a day |

Information needed | Income, debt, credit history, supporting documents such as W2s and ID | Income, debt, credit history, which is often self-reported |

Credit pull | Hard inquiry | Soft inquiry |

Strength in getting offer accepted | High | Low |

Best for | Beginning the formal mortgage process, establishing to seller your offer is serious | Low |

Step 3: Make an offer on a home

Preapproval letters are often valid for just two to three months, so as soon as you’ve received preapproval, you can use that time to house hunt.

When you find a home that meets your criteria, you can submit an offer letter to the seller through your realtor. Your realtor will help you determine an offer price based on comparable properties in the area, what terms and contingencies to include (such as the ability to rescind the offer if the inspection reveals major issues), and how much earnest money you want to put down.

Earnest money is a “good faith” contribution, typically 1% to 3% of the purchase price, that is held in an escrow account before closing. If you back out of the offer for a non-contingency related reason, the seller has the right to keep the money. Otherwise, if the sale goes through, it will be contributed toward your down payment and closing costs.

Step 4: Obtain final loan approval

Once your offer has been accepted, the mortgage is “into escrow” which means that it’s in the process of approval. There’s a lot that needs to happen before you get the keys to your new home.

- The lender will verify your original application and request additional information and documents, such as tax returns and pay stubs, to obtain final loan approval. This is known as underwriting.

- A title company will check the title of your home to make sure there are no issues, such as a lien or a contest on the title claim.

- You’ll schedule a home inspection to identify any potential repairs or maintenance needed on your home. If it’s a competitive market, you may choose to waive the inspection.

- Your lender will order a home appraisal, which confirms the home’s market value.

- Your lender will schedule a closing date, at which time you will finalize the terms and costs associated with your mortgage.

Step 5. Close on your loan

Three days before your closing date, you will receive a closing disclosure form which outlines the final details of your mortgage. In this disclosure, you’ll get a detailed breakdown of your closing costs.

In addition to paying closing costs, on closing day you’ll sign several documents, including a promissory note, which acts as your written promise to pay for the home, and the deed, which officially transfers ownership of the home to you.

At the end of the meeting, you’ll receive the keys.

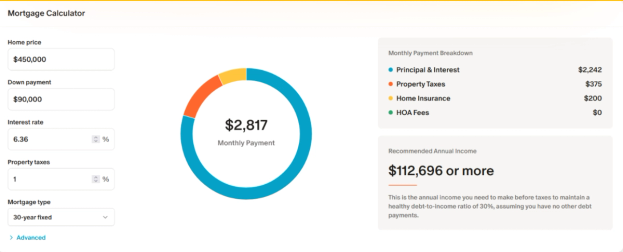

Run the math: Monarch's Mortgage Calculator

If you’re ready to take the plunge and apply for a mortgage, Monarch can help you every step of the way.

Your first stop is Monarch's Mortgage Calculator, which helps you figure out how much house you can afford and what your monthly payment will look like.

You can see not only how much you’d have to pay each month, but also how sustainable your mortgage would be based on your income.

If you want to see how your mortgage will impact your net worth, retirement, and overall financial plan, you can take the next step with Monarch forecasting as part of Monarch Plus. By adding a “Buy a Home” milestone, you can input your mortgage and monthly payment and see how your retirement and investment trajectory changes – with added growth of your home as an asset.

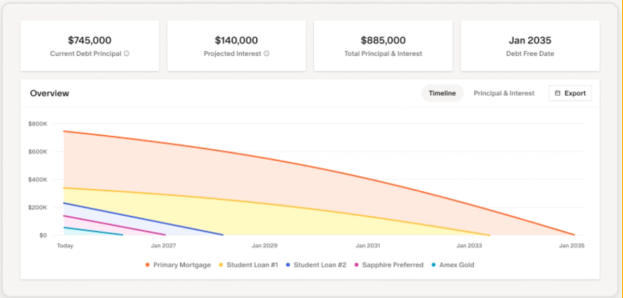

Finally, when you have your mortgage in place, you can track the progress on your payoff journey through Monarch’s Debt Dashboard, which tracks your amortization based on your payments and interest rates. As you make payments (and, hopefully, make an extra payment here and there), you can watch your debt shrink as your equity grows.

Across all of these tools, Monarch doesn't share your personal information with advertisers or third-party data sellers.

A mortgage is the first step. Make it the right one

Mortgages are powerful financial tools that help turn the money you once spent on rent into ownership. Your first house is more than a home — it's often the first real step toward building wealth. A mortgage is what makes that step possible.

FAQs

Will having a mortgage improve my credit score?

Making timely payments on your mortgage can be a good way to build your credit score, as you will have the loan for a long period of time and it can help diversify your credit mix. Initially, your score will take a dip due to the hard check from the application process and the fact your newer account will lower your average account age. However, with consistent payments, your score can rise meaningfully over the loan term as you build payment history.

Can I get a mortgage without a credit score?

You can through a process known as manual underwriting. This entails the bank going through your application and supporting documentation manually instead of an automated system like with the standard underwriting process, and thus takes longer and may come with extra fees. You will also have to provide additional documentation such as pay stubs, bank account statements, and rent and utility receipts.

What activities should I avoid during the mortgage underwriting process

When your application is being processed, you’ll want to avoid activities that will trigger a flag or large change on your credit report, bank account, or income stream. This includes:

- Quitting or changing your job

- Making a large purchase

- Receiving a large deposit without an explanation such as a gift letter

- Opening a new line of credit or loan

What happens if I can’t make a mortgage payment?

If you can’t make your mortgage payment, you can request a hardship deferment from your lender, which will allow you to temporarily pause your payments (though not your interest). Many lenders offer options for deferment if you are undergoing economic hardship or have faced a natural disaster. You can also see if you can lower your payments by refinancing if your credit score is still high. Mortgage lenders generally don’t like to foreclose on a house, as the process is costly, and will generally be willing to work with you so you can make your payments.

When can I refinance my mortgage?

It depends on the lender and loan type. Most lenders will require your loan be at least six months old and that you have at least 20% equity in your home. Government-backed loans like VA, FHA, and USDA can come with additional requirements for equity and on-time payments before you can refinance.