No matter what your background is, your financial situation, or how much money you make, you have the power to pay off your debt in a timely manner. While debt can happen to anyone, with some planning, smart strategy, and a few handy tricks, here’s how you can pay off debt the smart way with digital planning tools like Monarch.

Your Debt Repayment Action Plan

Starting off on your debt repayment journey can happen as soon as today. With some forethought and planning, you can be well on your way to getting your debt under control with a payment plan, a timeline, and an end in sight as you pay off your balance. Here are the steps in a nutshell.

- Figure out your debt balances

- Choose a strategy that works

- Build your budget around debt payoff

- Manage your payoff plan

- Put extra funds toward your payoffs

- Celebrate your wins and milestones

Here are the steps in more detail, and how Monarch can help you in your debt repayment journey.

Know Exactly What You Owe

According to the Federal Reserve, at the end of 2025, Americans owed a collective $18.8 trillion in debt, or $105,056 on average. Getting a handle on your balances is the first step to figuring out what your debt action plan is, since it will tell you what your monthly payments will look like and what you need to prioritize.

Your debt inventory should include debts such as:

- Credit card debt

- Retail credit

- Medical debt

- Student debt

- Personal debt

- Lines of credit

- Auto debt

- Buy Now Pay Later (BNPL) balances

- Mortgages

When building a debt inventory, it’s also important to list important information such as:

- The name of the creditor/collector

- The age of the debt

- The APR (also known as the interest rate)

- The current balance

- The minimum monthly payment

- The debt term

- Number of minimum payments remaining

- Payment due dates

This information will come in handy when it’s time to choose a debt repayment strategy.

Monarch Pro Tip: Staying on top of multiple balances and payments doesn’t have to be complicated. With Monarch’s tracking feature, you can link your balance accounts into the Monarch platform so you can see exactly what your balance, interest rates, and monthly payments are.

2. Choose Your Debt Payoff Strategy

Instead of simply making the minimum payments and hoping for the best, using a debt repayment strategy can help you pay off your balances more quickly and save you on interest in the long run. Here are some of the most popular methods to consider.

Debt Snowball Method

Best for: Quick wins as you pay off your debt balances

The debt snowball method has you ordering your debts from the smallest balance to the largest, and focus-firing any extra payments toward the debt with the smallest balance first while making minimum payments on all other debts. Once the first balance is paid off, you roll the payments you’ve been making into the next-smallest balance, “snowballing” your payments until all the debt is paid off.

Debt Avalanche Method

Best for: Maximum efficiency and speed in paying off debt

The debt avalanche method works similarly to the debt snowball method, where you roll payments from each paid-off balance into the next one. The key difference is that you order your debts by interest rate, paying off the highest-interest debts first.

In particular, Monarch recommends tackling debts in the following order of interest rates and aggressiveness with your payments:

- Level 0 (Highest priority): Debts at 25% interest or higher

- Level 1 (Middle priority): Debts at 10% to 25% interest, which you should try to refinance if possible

- Level 2 (Lowest priority): Debts at 10% interest or lower

While this method is faster in the long run, and will save you more on interest, it may take more time to pay down each debt individually, which takes away a bit of the reward and motivation the snowball method provides.

Debt Consolidation Loans

Best for: Simplifying payments and possibly saving on interest

Consolidation loans allow you to bundle payments by creating a new, singular loan, the money from which is used to pay off your other balances and creating a singular debt with one balance and interest rate. This can be helpful in not only simplifying your payments into one, and can even save you on interest if you manage to get a competitive rate compared to your other debts.

Use a debt consolidation calculator to see how much you may potentially save if you decide to go with this route. Keep in mind that you’ll be charged administrative, origination and closing fees on the consolidation loan, and you may be charged prepayment penalties on your other debts if it is part of your terms and conditions.

A quick word of warning: Do not use a debt consolidation loan to refinance credit card debt if you are still actively using the cards, since this can often lead to increased debt and endless debt paydown cycles.

Balance Transfer Credit Cards

Best for: Saving on interest with credit card debt

If you have a good credit score, you may qualify for a balance transfer card. Balance transfer cards allow you to transfer the balance of one or more credit cards to a new card, which comes with a low or 0% introductory APR. This introductory rate often lasts only for a few months before the standard APR kicks in, which means you have a limited amount of time to pay down the debt or transfer it to another card. However, it can be a good way to save on interest and maximize your payments while the introductory rate is in place.

Debt Management Plans Through Nonprofit Credit Counseling

Best for: Getting a handle on debt that feels overwhelming

If you have a large amount of debt and you don’t know where to begin on paying it down, you might want to consider talking to a certified credit counselor. Credit counselors can help you manage your debt by creating a debt management plan (DMP), where you pay a single amount each month to the credit counseling organization, and they use the payment to pay off your balances. The credit counselor will provide you with basic financial education and offer resources to help you manage your payments and build a budget. However, be aware that DMPs often require you to close any lines of credit that are included in the plan, which could hurt your credit score and take away some wiggle room in case of financial emergencies.

While credit counseling can come with fees, many organizations will waive them if you are below a certain income level, or offer free initial counseling sessions so you can see if the service is best for you. Working with a nonprofit credit counseling company will typically have the lowest fees and most free resources available.

Debt Defrost

Best for: High-interest credit card debt

Debt defrost works well with credit card debt. With this method, you start with either the snowball or avalanche method to pay down all of your credit card balances to 30% or less of your available credit limits.

Then, once your credit score has increased enough with a positive payment history and a good utilization ratio, take out a 0% or a low-interest balance transfer card or loan for the rest of the debt, saving you on interest as you pay out the remainder of the balance.

Choosing the Right Debt Repayment Method for You

When selecting a debt repayment strategy, consider the following factors:

- The type of debt you have. If you have mostly credit card debt, you might want to consider the defrost/balance transfer method.

- The number of balances you have. If you’re juggling multiple payments and want to simplify your monthly payments, then you may want to take out a consolidation loan.

- The interest rates on your current balances. Multiple high-interest debts could mean the avalanche method is the way to go.

- Your credit score. If your credit score is in good shape, then you may be able to get a better rate with a consolidation loan, or qualify for a balance transfer card.

- How you’re managing your monthly payments. If you can put extra money toward your payments, then consider the snowball or avalanche strategy.

- How much extra help you need. If you’re in need of extra guidance or education, consider working with a certified credit counseling organization.

- How motivated you are. If you’re in need of extra motivation or a mental boost, the snowball strategy may work well for you.

3. Create a Budget that Makes Debt Payoff Automatic

Your budget and your debt repayment strategy should go hand in hand. Once you have an idea of what your monthly payment(s) will look like, you’ll want to make it a top priority each month so you stay on track. Making your payments automatic will both make the process easier and seamlessly integrate your payments into your budget – so long, of course, as it aligns with your cashflow.

As such, integrating your payments into your budget will depend on your budget type. If you use a category budget, then your debt repayments should fall under your “needs” and take precedence over your “wants” category.

Another approach to take is the flex budget, where instead of dividing your budget into needs and wants, you divide your budget into fixed monthly expenses, one-time expenses, and a flexible spending category. Debt repayments would go under fixed monthly expenses, allowing you to adjust your spending in the flex category accordingly in order to accommodate your payments. This simplifies your budget and makes it easier to organize your spending, instead of having to track and set limits on individual categories.

Monarch Pro Tip: Monarch offers both Category and Flex budgeting. Simply select which mode works for you on your dashboard, and set your rules and transactions accordingly. Monarch can automatically classify your transactions based on the rules and parameters you set.

The Emergency Fund Question

If you don’t have an emergency fund in place, or if yours is seriously depleted, then you may be wondering if you should prioritize paying down your debt or building your emergency fund.

While paying down debt is important, your emergency fund still matters, especially in the long run if you’ll be paying off debt over a course of several months or years. Not only can your emergency fund help protect you when you face an unexpected expense, it can help support your debt repayments if you experience a loss of income.

As such, Monarch recommends saving either $1,000 or one month’s worth of take home pay (whichever is greater) before focusing on paying down debt. Once you’ve paid off your debt balances, you can focus on fully stocking your emergency fund with the recommended three to twelve months’ worth of expenses.

Monarch Pro Tip: You can use a Save Up goal to set up an emergency fund savings goal, which seamlessly integrates with your budget and allows you to track your progress.

4. Stay on Track and Stay Flexible with Your Payoff Plan

Once you have your payment plan in place, stick to it. Manage your budget and prioritize your payments accordingly. Stay motivated by keeping your end goal in mind, and by tracking and celebrating your milestones (more on this later.)

If you need to adjust, realign your strategy accordingly. It might make sense to switch to the Snowball method if you’re feeling low on motivation, or use the Debt Defrost if you qualify for a balance transfer card.

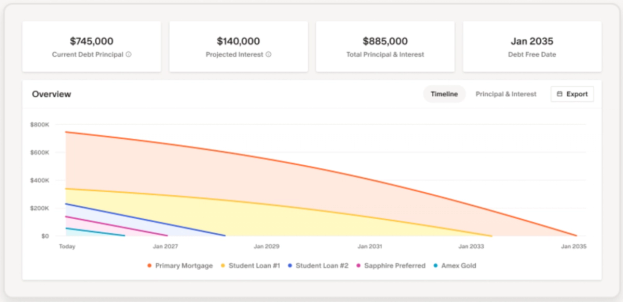

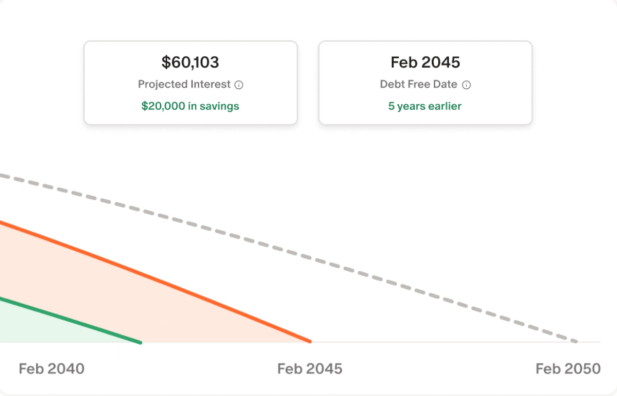

Monarch Pro Tip: Watch your debt progress with Monarch’s Debt Dashboard, which automatically tracks your payments and interest and creates a forecast based on your balances and payments.

5. Put Extra Funds Toward Your Repayments

A little can go a long way when it comes to paying down debt. Did you know that contributing an extra $20 to the $150 minimum payment on a $5,000 credit card balance with 26.5% APR can save you nearly $1,000 and a year’s worth of repayments?

If you want to find extra money to put toward your repayments, look at your budget and see which categories you can afford to cut down on or adjust for extra cash. Some examples include:

- Utilities. Cut down on water and electricity usage by running your thermostat lower or fixing leaky taps.

- Groceries. Shop smart by looking for deals, using coupons, and buying in bulk.

- Subscriptions. Cut back on services you don’t use or need, or consider downgrading to a cheaper version.

- Restaurants. Set a hard cap for how much you eat out, and see if you can stay under it.

- Travel. Carpool to save on gas, and consider having a staycation or going somewhere local instead of taking an annual trip.

Besides reducing your spending, you can also increase how much you’re contributing to your repayments by bringing in additional income. You can do this by:

- Taking on a side hustle. Ride sharing, food delivery, or tutoring on the side can bring in some extra income.

- Sell your creations. If you’re a hobbyist, or can make a mean batch of cookies, consider hitting up some craft fairs to sell what you make.

- Rent out your space. If you have a room to spare, or are away on the weekends, consider listing your home or apartment on a vacation rental site.

- Sell your old stuff. Go through your closet and your bookshelves and see if there are any old clothes, books, toys, or appliances you can sell for cash.

Monarch Pro Tip: If you’re adding extra payments, check your Debt Dashboard. Once logged, your forecast should have been updated, telling you how much closer your extra contribution has brought you to the finish line. You can also run simulations and see how far your additional payments can take you.

6. Celebrate Your Wins

With every payment you make, and with each debt you pay off, take a moment to pat yourself on the back for taking another step in your debt repayment journey. Paying off debt takes dedication and discipline, and with every step you are getting closer to achieving the financial freedom that comes with being debt-free.

Celebrating your progress will not only keep you motivated, but help you remember and acknowledge that your hard work will truly pay off in the end. You can use tools like the Monarch Pay down calculator or a fundraising-style thermometer if you want something hard copy to make it even more visual. Pick a small treat for yourself to celebrate as you hit each milestone, such as your favorite cheap meal out or a new music album or your favorite ice cream.

Debt Repayment Plans for Different Debt Types and Circumstances

Choosing how you want to build out your debt repayment plan will depend not only on the type of debt you’re in, but also your income and your individual life circumstances. Here are a few tips for different types of debt and repayment scenarios you may want to consider.

Credit Card Debt

Credit card APRs tend to be high and variable, which means they adjust with the market rate from month to month. As such, time is of the essence. Paying off credit card debt as quickly as possible – especially if you’re using the avalanche method – is key to saving on compounding interest.

- Pause spending on the card immediately. Trying to repay a fluctuating balance will throw off your timeline. Ideally, any new balances you accumulate you should be paying in full each month. If you’re having trouble, try literally freezing your card by putting it in a container of water in the freezer and removing the card info from your electronic wallet. That way, if you truly need it in an emergency, it’s still there, but much harder to get to.

- Look into consolidation or balance transfers. If you have a credit score above 670, a consolidation loan or a balance transfer card can give you some breathing room with a lower APR.

- Pay attention to the APR. As many credit card companies will charge a variable rate, how much you’re paying in interest will change from month to month. Stay on top of these changes so you can stick to your strategy and adjust your monthly payments as needed.

Student Loans

Student loans are one of the most common types of debt, and one of the most pernicious. Since they aren’t dischargeable in bankruptcy, you’ll want to focus both on repayments and on possible forgiveness plans you may qualify for.

- Be aware of grace periods for repayments and interest rates. While you may not be required to pay off your loans immediately after graduation, depending on the loan type, you may be charged interest during the grace period.

- Look into income-based repayment plans. Depending on how long you’ve had your debt, you may qualify for an income-based repayment plan through the federal government for federally-backed loans.

- Explore forgiveness and employer repayment options. Many companies offer loan repayment plans as part of compensation packages. If you work as a public servant, you may also be eligible for forgiveness for certain types of federally-backed loans.

Medical Debt

Medical debt can happen to anyone, especially if a medical emergency quickly outstrips your emergency fund or isn’t covered by insurance.

- Ask the creditor if they have a repayment plan available. Many hospitals and medical groups will have no-interest repayment plans for initial bills.

- See if you can settle the debt with the creditor. If your income is too low to cover the payments, contact the debt holder and ask if they would be willing to forgive part of the balance in exchange for prompt repayment of the remainder.

- Apply for financial assistance. Many hospitals, non-profit and government agencies offer charity aid if you are struggling with financial hardship.

Auto Loans

Car loans, while secured by the car, can be tricky to navigate. If you wreck the vehicle, or if depreciation results your vehicle being worth less than the loan, you’ll still be on the hook for the remaining balance.

- Consider downgrading your car if the payments are overwhelming. Trade-in options can allow you to pay off part of your debt for a smaller, less expensive vehicle.

- See where you can save on insurance. You may be able to get a discount if you have a good driving record or a high credit score. Shop around for car insurance at least once a year to make sure you’re paying the lowest rates.

- Stay aware of prepayment penalties. If you’re thinking of refinancing, consolidating, or trading in your vehicle, be sure to read the terms of your loan so you don’t get hit with an early repayment fee.

If You're Paying Off Debt on a Low Income

Feeling squeezed for cash with your loan repayments can be stressful. If you’re struggling to make loan payments with your current income, you have a few options.

- Work with a certified credit counselor. Many non-profit credit counseling companies will offer free or reduced-fee credit counseling services and debt management resources, especially if you fall below a certain income threshold.

- Look into income-based repayment plans. Some types of debt offer these, which allows you to adjust your payments based on what you make.

- Request a hardship waiver. If you’re going through a period of lost income or other type of crisis, you may be able to request a payment forbearance from the lender while you get back on your feet.

If You're Tackling Debt as a Couple

Managing debt with a partner or a spouse means having a unified front for managing your finances and payments. While you don’t necessarily have to be responsible for your partner’s payments if you don’t want to, it’s still a good idea to understand where your responsibilities lie and how you want to handle it as a couple.

- Stay on the same page about tackling debt. Discuss who is responsible for what debts, how you want to share the load of repayments, and what strategies you want to pursue.

- Be aware of payment adjustments with marriage. Some types of debt will account for both of your incomes, should you get married, with income-based repayment plans and minimum payments.

- Be transparent about what debts you have. Trying to hide debt from your partner will only cause distrust and financial issues down the line. Instead, be open about what debt you have, and how you plan to pay it off.

Monarch Pro Tip: You can add a partner or spouse to your Monarch account for free, allowing you to add their accounts and debts to your dashboard and creating a seamless experience for managing your finances together.

The Psychology of Staying Motivated Through Debt Payoff

Debt can feel overwhelming. When your balances keep creeping up from interest, when collectors call, and when your payments just don’t seem like they’re making a dent, it’s not uncommon to feel like giving up.

If you’re struggling mentally because of debt, you’re not alone. According to a study by Bankrate, 43% of American adults cited debt as a cause of mental distress.

As such, staying motivated isn’t merely a matter of buckling down and muscling through the tough parts. Understanding the neuroscience behind debt repayment, goal progress and building an achievement system for yourself can help you stay the course. Here are Monarch’s science-backed strategies to keep you on track with debt repayment.

- Create a vision for what you want your debt-free life to look like. Studies have found that visualizing your end goal and its impacts builds anticipation as you work toward it, releasing dopamine as you make progress and encouraging you to stay on track.

- Visualize your progress. Having a visual cue helps you easily track your goals and helps your brain connect your efforts to your progress. Using a chart, a “debt thermometer” or a visual meter can help you with this.

- Fuel your dopamine with regular milestones. When you achieve a goal that you’ve been working toward, your brain releases dopamine. Making sure you achieve your goals regularly keeps the dopamine flowing, which is why it’s a good idea to divide your repayment journey up into regular goals (such as 10% paid off, 20% paid off, and so on) so you have something to look forward to.

- Gamify your experience. Gamifying your debt repayment with rewards, visual cues and “leveling up” as you reach your milestones can make debt repayment more fun, whether you turn each debt into a “boss” to defeat or create a character that receives upgrades with each level.

What to Do When You Slip Up

Getting thrown off course in your debt repayment journey can happen for a variety of reasons, whether it’s losing income, having to take on more debt because of an emergency, or simply missing a payment. Here’s what to do when that happens.

- Go back to Step One and take inventory. See what your debt totals are, where your interest rates and payments stand, and adjust your strategy and timeline accordingly.

- Address late payments as soon as possible. If you’ve missed a payment, focus your funds on covering those firstly, especially if you want to avoid being sent to collections.

- Ask if late fees can be waived. If you’ve only missed one payment and have otherwise paid on time, some creditors will waive the late fee and penalty if you catch it in time.

- Request hardship forbearance. While it won’t put your interest on pause, you can avoid late fees and penalties if you’re able to get a payment waiver.

- Use your emergency fund. If you have it, lean on your emergency fund to make payments. You’ll be better off avoiding late fees and the impacts of a late or missed payment.

- Don’t give up. While it can be discouraging, don’t let setbacks prevent you from paying down your debt. Take a pause if you can, re-evaluate your strategy, and pick up where you left off. Even if your timeline is moved back, it’s still better than making no progress at all.

How Paying Off Debt Affects Your Credit Score

As you pay off your debt balances, you can expect to see both positive and negative changes in your credit score. While paying down your balances can boost your score in certain aspects, it can lower it in others.

Don’t let this hold you back from paying off debt, since you’ll be better off in the long run paying down your balances and becoming debt-free, and your score will recover more if you aren't carrying bad debt. Here’s what to expect, and which factors will impact your score.

- Credit utilization. As you pay down revolving debt, your credit utilization will go down, boosting your score.

- Age of accounts. When you pay off a fixed debt, the account will close, which will lower your average age and your score.

- Positive payment history. With every on-time payment, you’ll contribute to your score positively.

- Hard inquiries (if using consolidation or balance transfers.) If you apply for a consolidation loan or balance transfer card, you’ll get a hard inquiry on your credit report, which can dip your score for a few months.

- Closing accounts. If you choose to close your credit card accounts after paying off the balance, your score will take a hit, both because you’ll reduce your available pool of credit with your credit utilization, and you’ll lower your average account age. If you close all of your credit and loan accounts, then you won’t have a score at all, which is why it’s a good idea to keep one or two of your older cards open and pay off the balance in full monthly.

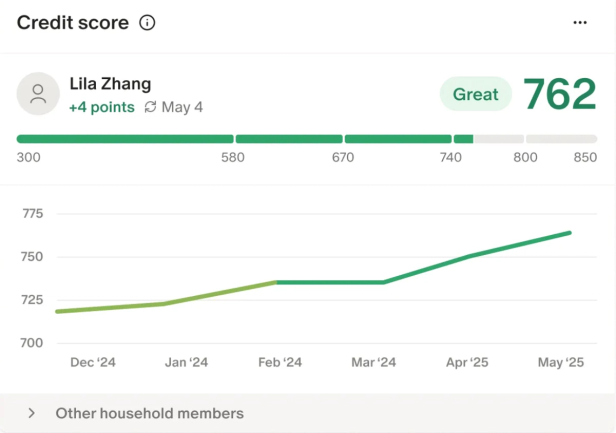

Monarch pro tip: You can view your credit score on your Monarch dashboard. Simply enable credit score viewing and keep track of how your score changes from month to month.

The Tax Implications Nobody Talks About

Paying down debt comes with certain tax implications, which can impact how much you can deduct and what you pay when tax season comes around. Here’s what to know.

Forgiven Debt and Taxable Income

If you have part of your debt forgiven through settlement, forgiveness, or discharge, then you may be taxed for the amount of debt that was forgiven, as it’s considered personal income. This can impact your tax bracket and how much you and your family pays overall, which can be unpleasant to deal with if you’re already unable to pay the debt in full.

There are a few ways you can avoid paying income tax on forgiven debt.

- Declaring insolvency. If you declare yourself insolvent (unable to pay back your debt in full with your current assets), the IRS can waive the taxes on your debt.

- Bankruptcy. Debt forgiven through the bankruptcy process is generally not taxable.

- Forgiveness through certain government programs. Some student loan forgiveness programs don’t consider the forgiven debt to be taxable.

- Debt canceled as a gift, personal bequest, or inheritance. This generally only applies to debt given on a personal basis, such as between family members.

Deductions on Debt

The good news is that some parts of your debt repayments can be counted as deductions on your taxes. While it will generally depend on the kind of debt, the payments, and the interest. Here’s a general overview of what you can deduct.

- Debt interest. You can deduct the interest payments on certain types of debts, including student debt and mortgages. Keep in mind that you can only deduct the interest – not the principal or fees. You can request a summary document from your lender for this purpose. There is also a cap for how much you can deduct.

- Prepayment penalties. If your mortgage agreement comes with a prepayment penalty, you can deduct this amount from your taxable income if you have paid the penalty. Note that this applies to mortgages only.

As always, it’s a good idea to consult a tax professional when figuring out your deductions and taxable income, especially if you’re paying off multiple types of debt.

Should I Use a Debt Relief Program?

You may have heard about debt forgiveness programs, which promise to help relieve some of your debt through a process called settlement. In this process, the debt relief company will negotiate with the debt collectors and holders in order to have a certain percentage of the balance forgiven, in exchange for prompt repayment of the remainder.

As such, debt relief companies will typically require you to pay a certain monthly amount toward the remaining balances, along with a fee to pay for the debt relief service. Many debt relief companies will set up a plan and timeline so you know how long you’ll be repaying the balance.

While debt relief companies might seem like a good deal, there are a few things to keep in mind before deciding to work with one.

- Debt relief companies will only work with certain kinds of debt. Typically, you can only use debt settlement service on unsecured, personal, private debt, like credit card debt, and not secured debt like auto loans, business debt, or federally-backed debt like federal student loans.

- Your credit score will take a serious hit. Since many debt relief companies will have you pause payments so the debt goes into collections, the missed payments will quickly sink your score, and stay on your credit report for up to seven years.

- You will still have to pay back some of your debt. Debt relief programs don’t relieve 100% of your debt, and the payments you make include the fee for services.

- You may not get your debt relieved. If negotiations fail, you can end up on the hook for your full debt balance, which may be in collections and have racked up late fees in the meantime.

Before considering debt relief, weigh your options. You may be better off building a debt repayment plan, working with a nonprofit credit counseling organization, or asking for forbearance from your creditors yourself.

What to Know About Bankruptcy

Something else you may have heard of when it comes to debt repayment is bankruptcy. Bankruptcy is a process in which some or all of your debt is discharged, in exchange for some or all of your assets (such as real estate, vehicles, and personal savings or investments) being liquidated (sold off) to pay off part of the balance, or when you reorganize your debts and create a payoff plan.

Bankruptcy is a legal process. When you file, you will be required to pay filing and court fees, and to appear in bankruptcy court for the process. While you don’t have to retain an attorney, it can be helpful to have one to help guide you through the process, though the fees can start at $1,000.

There are two types of personal bankruptcy to be aware of.

- Chapter 7 bankruptcy is when you liquidate your assets to pay off the balance. These assets are typically auctioned off, and the revenue is used to pay off part of the debt. The remainder of the balance is then discharged.

- Chapter 13 bankruptcy is when your debt is reorganized into a payment plan you can afford over three to five years, with the remainder of the debt being discharged. While this allows you to keep your assets, you may end up paying more overall with the repayments and court fees, as the proceedings take longer and the fees tend to be higher. As well, the overall repayment process is slower than Chapter 7.

While bankruptcy can help you escape debt that you have no hope of paying off, there are a few things to keep in mind before considering it.

- Bankruptcy will stick around on your credit report for some time. It can take up to 7 to 10 years for it to fall off your report, and your credit score will take a massive hit. As such, you’ll have a harder time borrowing and getting good interest rates in the future.

- Some types of debt can’t be discharged in bankruptcy. These include alimony, child support, and student loans.

- Even if you don’t hire an attorney, you’ll still have to pay fees. These include court fees, filing fees, mandatory education fees, and other legal and administrative fees that will depend on the filing and length of court proceedings.

- The proceedings can be lengthy. Bankruptcy cases can take months to resolve, and you will be expected to be present for the hearings set by the court, especially if you don’t hire a lawyer.

Bankruptcy is a serious process that requires thought and research before you take the plunge. Consider other debt payoff methods before taking this route, and consult with either an attorney with experience in the field, or a financial advisor.

Your Path to Becoming Debt-Free Starts Today

Paying off debt is a bit like a marathon. You’re better off making steady progress and strategic moves instead of scrambling to pay off your debt all at once if you don’t have the funds to do so. The best way to pay off debt is by keeping track of your balances, choosing a smart strategy that works for you, and by staying on track by keeping motivated and setting realistic goals.

Monarch can help you every step of the way, with dynamic updates through your linked accounts, a live debt dashboard that tracks your progress, and goals that integrate seamlessly into your current budget. No matter where you are in your financial and debt repayment journey, give Monarch a try today and see if it works for you.

FAQs

What is the smartest way to pay off debt?

The most efficient strategy is the avalanche strategy, which prioritizes paying off high-interest debt. It’s faster and saves on more interest than the snowball method, at the expense of not having as much intrinsic motivation, since your final balance repayments are often more spaced out.

How to pay off $10,000 in debt fast?

Make more than the minimum payments by contributing as much as you can spare towards the balance. Focus-fire on paying it down, and stay ahead of the compounding interest.

Is it better to pay off debt or save money?

While paying off debt should be a priority, setting aside a small emergency fund with $1,000, or one month’s worth of take home pay, can be a helpful financial cushion if something goes awry.

How long does it take to pay off debt?

That depends on the type of debt, the balance, the interest rate, and how much you’re contributing. You can speed up the process by using the avalanche method, and by focusing any extra money you have on your repayments.

Does debt consolidation hurt your credit score?

It can, both a hard inquiry (which you’ll be required to have done when you apply for the loan), and with the fact you are reducing the average age of your accounts as you pay off the different loans during the consolidation process. If you close any credit cards, it will also lower your utilization ratio, which can cause your score to dip.

What happens if you only pay the minimum on credit cards?

While it won’t hurt your credit score or accrue late fees, making only the minimum payment can quickly cause your balance to balloon with compound interest. Moreover, it will take you a much longer time to pay off the balance than if you make extra payments.

Can you negotiate credit card debt?

You can, with the caveat that it can take time, effort, and multiple missed payments, which can hurt your credit score. If you can demonstrate to the lender that, with your current income, or due to financial hardship, you are unable to make payments, they may agree to settle and forgive a certain percentage of the balance. You will, however, be expected to pay the remaining balance, and you will need to demonstrate a legitimate need.

When should you seek professional help with debt?

If you’re feeling overwhelmed by your debt, or if you don’t know where to start with your payments, consider contacting a nonprofit certified debt counseling company. They can give you free and affordable resources for managing your debt and educating yourself on financial wellness.