When it comes to planning out your financial future with your partner, a budget is a great way to get on the same page. Creating a roadmap for your spending, saving, and financial goals will help you in the long run, and help you avoid staying in the dark about your financial health.

Wherever you are in your relationship, being on the same page financially is crucial. According to a survey by NerdWallet, two in three (67%) of engaged Americans found it difficult to have a money conversation with their partner.

A budget is the first step to forming a unified strategy to manage your finances as a couple, which is why it’s important to create one early on. Here’s how you can create a budget with your partner, and how Monarch can help you create a financial roadmap that works for you and your relationship.

A Quick Guide to Budgeting as a Couple

Short on time? Here’s a quick summary of the essential steps to creating a budget.

1. Start with a money conversation. Discuss your overall goals and your money philosophies so you’re on the same page.

2. Choose your account structure - joint, separate, or hybrid. Figure out how you want to structure your accounts and move forward from there.

3. Calculate your combined income and expenses. This will give you a framework for your budget and determine how you need to adjust in order to achieve your goals.

4. Pick a budgeting method that fits your couple style. Whether it’s a flex budget with no categories, a zero-based budget with strict limits, or something in between, it’s crucial to pick a budget that works for you.

5. Handle the hard stuff — debt, income gaps, and financial secrets. Being transparent and avoiding money secrets will help you in the long run.

6. Set shared financial goals (and track them together). Shared goals like building an emergency fund, paying down debt or saving for a vacation will help build your financial unity and long-term planning.

7. Schedule your money dates (and a budget meeting agenda). Review your budget regularly, revisit your money goals, and check in on how you’re feeling about your overall financial picture.

8. Choose the right tools. Digital tools like Monarch can combine your income and expenses without the need for manual tracking, making your budgeting process fast, accurate and unified.

Why Budgeting as a Couple Matters More than You Think

Couples that budget together have less conflict. According to a Fidelity Survey, 78% of couples who have regular money discussions together say that money isn’t the greatest point of conflict in their relationship. According to another study by Ramsey Solutions, 94% of couples in a self-labeled “Great” relationship said they regularly discuss their financial dreams and goals with one another.

Being able to talk about your finances is crucial to building a relationship together, especially as you combine assets, purchase a home together, pay down debt, save for retirement, or choose to grow your family. A budget is the first step to getting your finances in order

1. Start with a Money Conversation

Before you start logging into your bank accounts and adding up expenses, you’ll want to sit down and discuss your broader financial philosophy. This will basically set the stage for how you approach your budget and your finances as a couple, and keep you both aligned for how you approach your budget.

When you have your money conversation (drinks and mood lighting optional), ask yourself and your partner these questions:

- What is your goal with budgeting? Do you want to save more, manage spending, pay down debt, or all three?

- How do you want to share and pay down individual liabilities, like student debt?

- Do you have a positive relationship with money? What financial habits do you have that may impact the budget or spending plan?

- What is your spending and budgeting philosophy? Does every dollar need to be tracked? Is saving a higher or lower priority than spending money on “fun” things?

- Should partners run large purchases by one another?

- Do you have any hard limits on expenditures, such as not using Buy Now Pay Later, or opening new credit lines without checking in?

- How do you feel about sharing financial information and transactions? Are there some accounts you feel need to be kept separate?

- How do you want to handle emergency expenses? What do you consider an emergency expense, and when is it an appropriate time to draw from the emergency fund?

- If either one of you receives a windfall, like an inheritance, how do you want to handle it? Should it be kept separate, or shared, and to what degree?

You don’t have to answer all of these questions immediately. However, they are something that you should keep in mind, and revisit as you develop your budget and your financial plans over time and your relationship.

2. Choose Your Account Structure

Once you have a shared idea of how you want your financial roadmap to look like, the next step is to discuss how you want to structure your accounts and your bills.

Account Structures

Establishing boundaries around how you want to structure your finances is crucial to preventing conflict and keeping the lines clear. Whether you decide to combine your accounts, maintain separate finances, or have a mix of the two, be sure you both have the same idea of how you want it to go.

Also keep in mind that you don’t have to stick to one account structure forever. You may start out with separate accounts and later open a joint account or two later down the line, or decide to merge your accounts and finances when you get married.

Joint Finances

Joint finances are shared between a couple, with each person having access to transaction details, withdrawals, and deposits. This can also include a shared credit card. Two in five (40%) of all couples maintain their finances jointly, according to the Census Bureau.

Joint finances can make sense when you pool your money as a whole and don’t see a need to split bills or keep transactions separate. This can simplify your finances and budgeting since you have fewer accounts to keep track of. You also have maximum transparency, as you can see each other’s transactions.

However, there is an element of risk to this approach. If one partner goes overboard with spending, or is facing bankruptcy, then the other’s money is put as risk. If you share a credit card, each partner risks the other racking up the balance beyond what you can pay. There’s less privacy around your transactions, and separating out your finances if you decide to split can be messy.

Joint finances can bring a lot of simplicity and transparency to a couple’s finances. However, you’ll need to have a high amount of trust in one another and a unified financial vision in order to make it work.

Separate Finances

Keeping your finances separate is a starting point for many couples, with nearly one in four (23%) of couples maintaining separate accounts, according to the Census Bureau.

Running your finances separately provides a fair amount of security and privacy, since each partner is responsible for their own spending and savings. It’s also easier than ever, with tools like Monarch allowing couples to combine their account information on one dashboard without the need to merge accounts. This approach can work if you have greatly different incomes, different saving and spending habits, or if you’re still building financial trust in your relationship.

However, it can be complicated to track bills and transactions across multiple different accounts, and may provide a psychological barrier to having a unified vision for your finances as a couple. Splitting bills can take some coordination, as does budgeting your individual expenses.

Hybrid (Both Joint and Separate)

This approach provides the best of both worlds, with the couple maintaining one or more joint accounts while still maintaining separate personal accounts for their own use. According to the Census Bureau, 17% of couples have both joint and individual accounts in this fashion.

The hybrid approach can be helpful if you want to merge some or most of your finances, while still maintaining some privacy with your own individual accounts. For example, if one partner stays at home, they may choose to keep a separate account for their own spending, especially if they work part-time or have a side hustle.

Another approach is that each partner receives their paychecks to their own personal account, and an agreed-upon amount is deposited into a shared account.

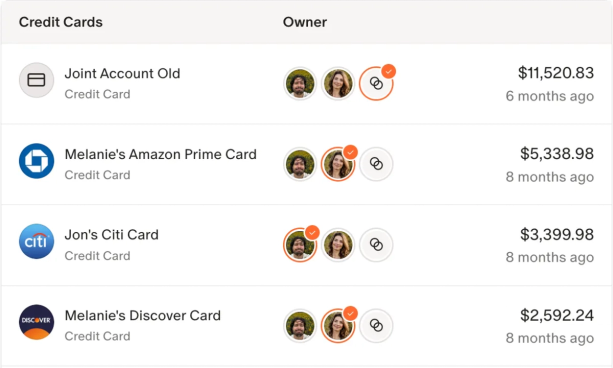

Monarch Pro Tip: Linking your accounts in Monarch can bring all your information to one place. You can assign ownership to different accounts based on whether they’re separate or joint, and review transactions and balances.

Splitting Bills

After you’ve figured out how you want to manage your accounts, you’ll want to discuss how you want to split bills. Your account structures will influence how you manage this. If you have separate accounts, you may choose to split bills proportionally. If you have a mix of accounts, you may choose to pay some bills from the shared account and others individually.

Here are a few ways to split bills, should you choose to do so.

- 50/50 split. Bill payments are split down the middle, with each partner being responsible for their half. This is the most simple way to split bills, and works well for couples with a similar income.

- Proportional splits based on income. With this approach, bills are split based on how much each partner makes, which can be helpful for couples with large incomes disparities. For example, if one partner makes $2,000 a month and the other makes $8,000 a month, the partner with the smaller income would pay 20% of the bill, and the other 80% of the bill.

- One pays, one saves. One partner pays the bills, while the other deposits the bill amount in a shared account. This can be a quick way to build up savings, and gives you some wiggle room in terms of living on one income.

- Shared bills are merged, others are separate. This approach works if you have a hybrid account. Shared bills such as the rent, utilities, and other shared expenses are paid for out of a joint account, while more personal bills, such as subscriptions, individual loans and car payments, and pet bills are paid from your separate accounts.

3. Calculate Your Combined Income and Expenses

After you’ve picked out an account and bill-paying style, you can start tracking your income and expenses.

While you don’t have to combine your incomes if you choose to keep separate accounts, it is a good idea to see how much combined income you make so you have an idea of your general money pool, which will dictate how much you’re comfortable spending on housing, utilities, groceries, and so on as a couple.

When combining your income, be sure to include income streams such as:

- Regular salaries/paychecks

- Side hustle income

- Rental or investment income

- Trust fund dispersals

- Retirement withdrawals

- Social Security or disability payments

After you’ve calculated your income, it’s time to calculate your expenses. You can choose to do it by each partner, or to combine your expenses into one bucket. When doing so, broadly categorize your expenses (such as housing, utilities, subscriptions, clothing, etc.) so you can get an idea of where your spending tracks the most heavily.

Finally, it’s time to compare your income to your expenses. Ideally, you want your income to be able to cover your expenses and leave some for saving and investing. If it doesn’t, or if your spending isn’t aligning with your goals as a couple, then it’s time for a reevaluation. This is where your budget comes in.

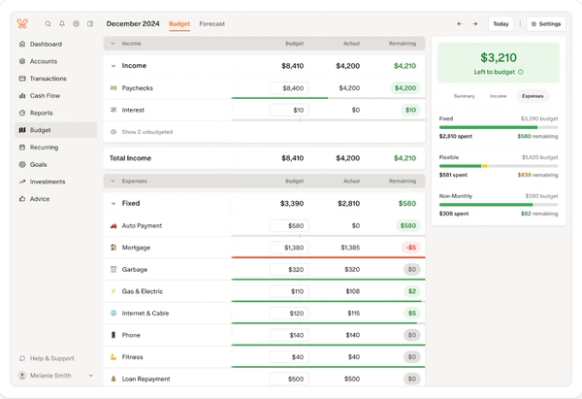

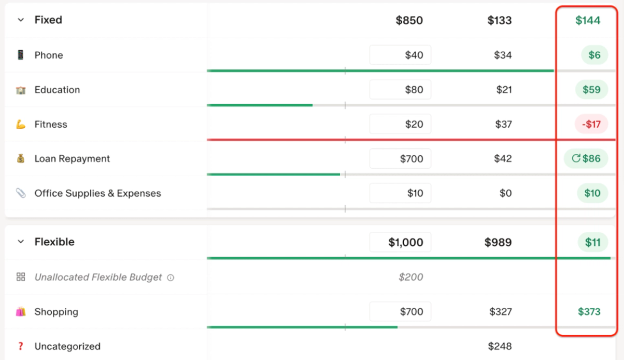

Monarch Pro Tip: Monarch automatically categorizes transactions based on the rules you set, allowing you to quickly track your budgeting groups and see what your expenditures are like at a glance.

4. Pick a Budgeting Method that Fits Your Couple Style

How you budget needs to reflect your financial priorities and style as a couple. Choosing a budget that works for you will help you in the long run, instead of trying to conform to a style that doesn’t align with your values. Fortunately, there are many ways to budget in a range of flexible and more strict ways, all of which provide you the structure to save and spend responsibly.

There are a few methods for budgeting as a couple, which we’ve summarized here. Check out Monarch’s budgeting guide for more detail on the different budgeting types.

Budgeting Types | How it Works | Best for |

Flex budgeting | Your budget is divided into three categories: fixed, flexible, and non-monthly. You set the limits based on what your fixed expenses (e.g. rent and subscriptions) are and what you expect for monthly and non-monthly expenses. | High flexibility with solid parameters for saving and spending limits, without the need for detailed categories |

50/30/20 rule | Allocate 50% of your budget to needs, 30% to wants, and 30% for savings and investments | Broad-category spending that doesn’t require a ton of detail |

Zero-based budgeting | Allocate every dollar to a saving or spending category | Strict budgeting that helps you achieve goals quickly and caps spending, with lots of detail |

Envelope method | Allocating exact dollar amounts to “envelope” categories for spending | Strict allocation of spending with some flexibility for rolling over leftover funds |

Pay yourself first/Reverse budgeting | Saving a portion of your income first before allocating the rest to spending | Quick saving with flexible allocations to spending |

60% Solution (Richard Jenkins) | 60% of spending is allocated to committed and essential expenses, and the remaining divided out between savings and “fun” money | Flexible spending and saving without the need for budgeting categories |

WECU Conscious Spending Plan | Budgeting that aligns with your personal values for spending instead of categorizing based on needs and wants. | Personalized budgeting that lines up with your values instead of an arbitrary number |

No-budget budget | Automatically save 10% your income, set essential payments such as rent and utilities on auto-pay, and freely spend the rest | Maximum flexibility with relaxed saving goals and no need for categories |

When selecting a budget, be sure to discuss your shared goals and financial styles with your partner, as this will impact which budget you decide to go with.

A few things to consider when selecting a budget are:

- Your need for flexibility. If your spending varies from month to month, or you don’t want to set any hard caps and instead give yourself more wiggle room, then you may want to go with a more flexible budget.

- Your spending habits. If you need to put a hard cap on your spending or keep a close eye on your transactions, then you’ll want to aim for a more structured budgeting style.

- How much detail you want in your budget. Category budgeting can help you keep a closer eye on your spending, while flex budgeting doesn’t require as much work or detail.

- Your monthly income and wiggle room. If you have a limited or unpredictable income, or little wiggle room, you’ll want to have a stricter budget structure.

- Your financial goals. If you want to save up toward a goal or pay down debt, then using a saving-oriented budget will help you more.

- What works both for you and your partner’s financial philosophies. If you want to keep spending in check and keep parameters around spending for non-essentials, then a category budget might work better for you.

5. Handle the Hard Stuff

Full transparency is crucial to managing a shared budget with your partner. While you don’t need to know the exact details of every single one of your transactions or accounts and transactions if you don’t want to, it’s essential that you’re aware of major liabilities that can impact your financial picture.

According to a survey by Bankrate, more than two in five couples (38%) believe that keeping a financial secret is as bad as infidelity. Yet, nearly one in 10 (9%) have kept a secret such as debt, income, or credit lines from their partner. Keeping financial secrets can not only betray trust, but skew your budgeting decisions in a way that can hurt you in the long run.

When discussing your budget with your partner, be sure to cover:

- How much debt each partner has and what the repayment timelines are

- What lines of credit (including credit cards) you both have open, and what balances (if any) there are on them

- If either of you have had any previous bankruptcies or major errors on your credit reports

- Your credit scores and history

- If either partner has any bills or balances in collections

- Major gaps in income month to month, and how you want to address them

- If either partner has had any struggles with overspending or racking up credit cards in the past

When going through this sort of conversation, be sure to keep things clear and nonjudgemental. Remember that your goal is to create an accurate and workable budget, and that you should work to achieve that goal together. You may want to consider talking to a financial therapist together if you need further help.

6. Set Shared Financial Goals

Having shared financial goals can help you unify your financial approach and give you something to work toward together. Some examples of shared goals can include:

- Saving up for a mutual goal like a vacation

- Saving up for a house payment

- Capping spending on one particular category

- Paying down debt

- Building an emergency fund

- Saving up for retirement

- Building up an investment portfolio

When establishing shared goals, it’s important to decide how you’ll both contribute to your goal. Like the way you split bills, you may want to make equal contributions, or proportionally make payments based on your incomes.

Something else to keep in mind is tracking your goals. Having an idea of the progress you make will go a large way to keep motivated and informed as you work your way to your endpoint.

Monarch Pro Tip: Monarch’s Goals feature allows you to track your progress on saving up or paying down debt, with linked savings accounts features and progress reports on your dashboard.

7. Schedule Your Money Dates

Many relationship experts recommend keeping the spark alive with regular dates. We here at Monarch recommend that you also have regular money dates in order to keep the (financial) spark alive and stay aligned on your financial trajectory and goals.

While it’s a good idea to have weekly budgeting check-ins, having more in-depth conversations about your finances will help you in the long run.

When having these money conversations, ask yourselves the following questions:

- Are you on track with your budget? If you’re regularly overspending or spending under your budgeted amounts, you may want to either adjust your habits or adjust your budget.

- Are your expenses going to drastically change in the future? If rent is going up if you’re adding a new car payment, adjust your budget accordingly.

- Are you meeting your financial goals? Check in on your progress and see where you are, if you need to adjust, and how close you are to completing it.

- Is the way you’re splitting your expenses working for you? If your incomes have changed, or if you’ve decided to merge your accounts, you may want to adjust the way you split bills.

- Is your emergency fund stocked, or do you need to refill it? If your base expenses have increased, you may want to increase how much you have saved up.

- Are there any upcoming big expenses you need to plan for? If you do, then you’ll want to adjust your budget or determine how much to pull from your savings.

- Are there any potential issues you want to discuss? If you’re noticing a change in spending habits, missed payments, or other potential problems, then talk them through before they get bigger.

8. Choose the Right Tools

Managing finances as a couple means multiple accounts, multiple logins, and multiple streams of income and expenditures to keep track of. Using the right tools to build and maintain your budget will help you stay on track and maintain a unified front when it comes to managing your money.

While there are multiple digital apps available, Monarch is uniquely tooled to help couples take control of their finances and stay on the same page as they achieve their goals.

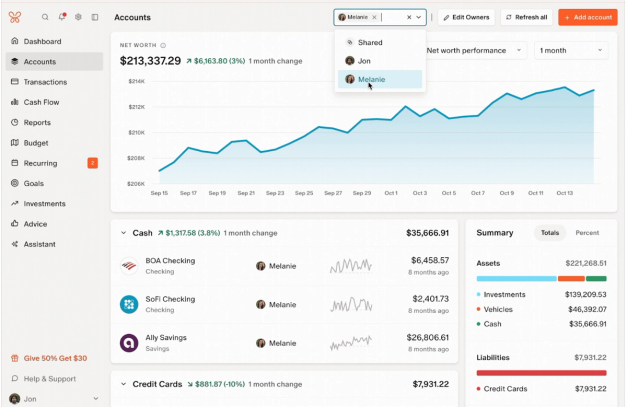

Monarch lets you add household members to your subscription, giving you the ability to create a shared budget and dashboard, which all users on the account can view. You can also link your accounts for easier tracking.

Monarch has built-in budgeting tools that can help you build your budget from scratch, with built-in categories and labels that are automatically added to your transactions. Want something more flexible? Monarch’s Flex Budget option has you covered.

Monarch’s shared views allow you to view transactions together with whichever accounts you choose to link, giving you a holistic way to track spending and connect it with your budget. You can assign owners to each account, so if any transactions need review, the account owner is in charge.

Monarch’s unified dashboard also allows you to see your net worth build over time as you save and invest as a couple.

Finally, Monarch lets you track your shared financial goals with the goal dashboard. You can set up goals to save up or pay down, link your contributions, and watch your progress.

When it comes to budgeting as a couple, you don’t need to juggle logins, manually update spreadsheets, or manually crunch the numbers every week. Monarch makes tracking your spending, building your financial plan, and achieving your goals as a couple easier than ever, with digital tools for accessibility and a way to approach your finances as a unified front. Give Monarch a try today and see where it takes you on your combined financial journey.

Conclusion

Starting your financial journey together as a couple is an exciting time. By establishing a budget and a financial plan early on, you can figure out your overall financial goals and philosophy as a couple, manage how you merge your finances, figure out your spending limits, address problems before they come up, and reach your shared goals together in a style that works for the both of you.

Monarch is with you every step up the way. With shared views on your linked accounts, quick reports on your budgeting progress, and a framework for creating a budget that works for you, Monarch can help you achieve your financial goals and manage your finances as a couple easier than ever.

FAQs

How should a budget be split for couples?

That will depend on how you want to split your income and bills. If your incomes are similar, and you don’t want to merge finances, then you might want to split it 50/50. If you have a large disparity in incomes, you may want to instead split your bills proportionally.

What is the 50/30/20 rule for couples?

This 50/30/20 rule is when you dedicate 50% of your income to needs, 30% of your income to wants, and 20% of your income to saving and investments.

Should couples have joint or separate bank accounts?

That depends on your level of comfort. Joint bank accounts present more risk as both partners are sharing their finances, though it does simplify budgeting and helps couples have a unified approach. Separate accounts present more individual security at the cost of making budgeting less unified. Many couples go with a hybrid approach, having both joint and separate accounts for a mixture of convenience and security/privacy.

How do couples split expenses when one makes more?

You can split your bills proportionally. For example, if one person makes $2,000 a month, and the other makes $3,000 a month, then you would split your bills 40/60.

How much should a couple budget for groceries?

According to the USDA, the weekly food cost for a couple between 20 and 50 years old is approximately, based on the plan type:

- Low cost: $124 to $143

- Moderate cost: $151 to $179

- Liberal plan: $179 to $218

Based on this, you can approximate how much you spend on groceries each week. This number may be higher or lower depending on your spending habits, needs, and area you’re living in.

When should couples start budgeting together?

It will depend on your comfort level in the relationship. Many couples choose to start combining finances and bills when they move in together, as they’re sharing many expenses such as the rent, groceries, and utilities. Many couples also use marriage as a milestone for combining finances, as they will pay for the wedding together and are establishing a long-term commitment.

How often should couples review their budget?

Monarch recommends couples review their budget on a weekly basis in order to keep an eye on spending, track goals, and re-align on any large purchases or issues that may have cropped up.

What is the best budgeting app for couples?

A good financial app should allow you to seamless track your spending without the need for manual logging, offer the financial insights you need at a glance, and allow you to build and manage your budget as a couple without hassle. Monarch offers the tools to build your financial plan, automatically track and categorize your spending, and track your financial goals all in one place.

Can budgeting improve your relationship?

Budgeting gives you and your partner a game plan for your finances. Research shows that financial stress can prevent couples from discussing money issues openly, which can lead to small problems growing into bigger ones. Budgeting not only encourages transparency, but give you and your partner the comfort of a unified financial strategy, and knowing that you’ll have enough for your essentials, savings, and discretionary expenses.

How do I get my partner on board with budgeting?

Sit down and have a general discussion about your financial philosophy and future goals. Do you want to save up for a house down payment? Pay for your wedding? Take a vacation? From there, you can discuss how a budget can help you achieve your goals by giving you a solid plan for saving and spending, allow you to consistently put aside money and keep your expenses in check so you have a timeline. Be sure to mention how budgeting can help encourage transparency and honesty as a couple, and allow you to hold one another accountable for your finances.