The phrase “for richer or for poorer” rings true when it comes to tying the knot. Managing your finances can help strengthen both your relationship and your future together as a couple, which is why planning ahead and planning together is critical.

Over three in four (78%) of couples who have regular money discussions together say that money isn’t the greatest point of conflict in their relationship, according to the survey by Fidelity. On the other hand, one in three (34%) partnered Americans say that money is a key point of conflict in their relationship, according to an Ipsos survey.

Avoid letting finances get in the way of your relationship. Before the wedding bells ring, it’s crucial to have a financial plan in place, not just to budget your wedding, but so you can head into your marriage with a unified financial vision and be ready to tackle the challenges along the way.

Here’s how you can draft a financial plan that works for your marriage, and how Monarch can help you build a budget and financial scaffold for success with your spouse.

What Financial Planning for Marriage Means

Financial planning goes beyond budgeting. A financial plan is a long-term forecast for where you want your money to go, how you want it to work for you, and how you plan to achieve your goals and financial vision.

For married couples, this means having a unified front on your finances. Since marriage combines many of your assets, you’ll likely be combining your finances one way or another, whether by sharing a mortgage payment, groceries, and utilities, or paying for your first child together.

Planning your financial life together shouldn’t take place the day after you get married. Instead, you should begin before you even choose your venue.

Why Financial Planning Before Marriage Matters More than the Wedding Budget

While your wedding budget should be part of your shared finances, your long-term financial plan will go beyond your special day. Being in financial harmony with your spouse will help you build your wealth faster, pay off and avoid debt, and manage your household even during tough times.

Having a financial plan before you get married also helps you build expectations and understanding with your partner. Getting on the same page now means that, once you return from your honeymoon, you can begin confidently and start with your financial plan and goals right away.

Here’s how to begin.

8 Financial Questions to Ask Your Partner Before the Wedding

Money talks, and you should listen. It’s important to start with a discussion about finances before the wedding so that you can be on the same page financially, address problems before they arise, and build trust in one another before you combine your finances. Despite this, two in three (67%) of engaged Americans found it difficult to have a money conversation with their partner, according to a survey by NerdWallet.

Instead of leaving it to the last minute, tackle your money conversation early on. Here are the key questions to ask when you have your money discussion.

What is Your Attitude Toward Money?

You and your partner’s feelings around money will set the tone for how you structure your budget, your financial goals, and what parameters you want to set around your spending. If your partner has a relaxed attitude toward money, you may want to set up a flex budget that allows for both flexibility and solid boundaries around how much to save and spend.

If you or your partner have had problems overspending, however, you might want to go for a stricter budget structure.

Be sure to also touch on what anxieties your partner has about money, such as worries over it running out, stress over “missing out” on experiences that lead to overspending, or a lack of knowledge around finances. If needed, seek counseling from a certified financial advisor or therapist.

2. What are Your Debts and Credit Balances, and Who is responsible for them?

Being aware of your partner’s debts will help you both figure out how to fit payments into your budget, and how you want to direct your income toward it.

While you don’t have to automatically become responsible for your partner’s debt upon marriage, it will impact your finances moving into the future. It’s also good to be transparent about what you owe, and how it has impacted your credit score. This will be especially important if you apply for a mortgage or loan together in the future.

3. Have You had Any Money Issues in the Past?

It’s important to be transparent about if either partner has had struggles with money in the past, whether it’s anxiety over not having enough, overspending that resulted in credit card debt, missed loan payments, or otherwise. That way, you can work through these problems together and create a financial plan with the appropriate boundaries.

4. Besides Essentials, What is the Most Important Thing in the Budget to You?

This will tell you a lot about both your partner’s priorities and attitude toward finances. While essentials like rent/mortgage, utilities, and otherwise of course take priority, it’s important to know what items your partner wants to prioritize in the future, whether it’s saving for a house, paying down debt, or building their investment portfolio.

5. Where do you Want to be Financially in One Year? In Five? In 20? In 40?

Visualizing a vision for your financial future is an important step in figuring out your financial goals. Use this question as an opportunity to draw a (rough) map of your financial roadtrip, and what destinations you want to have on it. Do you want to have a house in a year? Go on vacation with your kids in five? Pay off your mortgage in 20? Retire in 40? This will inform you of what goals you need to set – and where you see yourselves together on the financial road.

6. Do You Want Kids, and How Do We Manage the Expenses Around Them?

Children are one of the biggest deciding factors in maintaining a partnership, as well as one of the biggest expenses. If you and your partner decide you want kids, discuss how you want to handle not only the general costs (clothes, food, gear, and so on) but also how you want to pay for childcare. Should one spouse stay home? Which one? Do you want to move closer to your family? Or will you opt for daycare or a nanny?

7. What Do You Think Constitutes a Financial Secret?

Financial secrets, such as secret credit cards or undisclosed debt, can quickly sow distrust and conflict in your relationship. Also known as financial infidelity, 43% of Americans believe keeping financial secrets is as bad or worse than having an affair, according to a Bankrate survey.

What counts as a financial secret can vary among partners. Whereas one partner may not care if the other has a “secret” account, the other might want transparency. The same goes for debt, credit cards, and other financial accounts. While there is no right answer, it’s important to be on the same page about what you need to be transparent with your partner about, and if you are comfortable with that transparency.

8. Should We Get a Prenuptial Agreement?

A prenuptial agreement (prenup) outlines how you will divide your assets in the event of a divorce, with provisions for debts and other financial factors that may come into play. It is a legal document, typically presided over and executed on by an attorney, and it must be established before you are married.

A prenup highlights which assets are considered strictly yours and your spouse’s, so they aren’t defined as “marital” (combined) property in divorce court. It can establish one spouse as liable for the other’s debt, or absolve them of this liability. It can also provide provisions for alimony; for example, one spouse may not be eligible for alimony if they are discovered to be committing infidelity.

Prenups are also helpful for drawing outlines around ownership during the relationship. For example, a prenup can include clauses for pet custody, house equity if both you and your spouse only started paying in equity together 10 years into the mortgage, tax liability if one spouse owes taxes,

Some couples forgo having a prenup, since they feel it is unnecessary if they choose not to divorce. However, a prenup can be helpful in establishing your financial boundaries, and figuring out what is at stake in the case of separation. And career sacrifice compensation if one spouse opts to quit and stay home or support the other spouse.

Your Pre-Wedding Financial Checklist: One Year to "I do"

The months leading up to your wedding will likely be filled with licking envelopes, tasting buffet options, and choosing flowers for your centerpieces. It should also be filled with touch points for your big financial picture, from figuring out your budget to finalizing your wedding expenses.

Here’s our one-year timeline, and what to expect.

One Year

A year before your wedding, you’ll probably be shopping around for venues and vendors, if you haven’t already done so. Now is the time for big picture discussions: What you want your wedding budget to look like,

- Start with big money discussions. Go over your philosophy on your finances, what you want your budget to achieve, and what your financial goals are.

- Figure out how much you want to spend on your wedding. If you haven’t done so, set your thresholds, figure out your headcount, and start selecting your venue and vendors.

- Discuss what goals you want to achieve before your big day. Besides saving up for the wedding itself, see if you want to start on your emergency fund or get a house down payment fund going.

- Figure out your combined budget. Choose your budgeting style, your categories, and your goals. Even if you haven’t fully combined your finances, it can be a good “dry run” to start as you save for the wedding.

- Discuss if you want to open a new card or joint account for wedding expenses. Many couples will use a credit card to finance their wedding to take advantage of rewards, which can be a good option so long as you can pay off the balance on a monthly basis.

- Discuss financial boundaries. Establish whether you’re okay with receiving financial help from family in paying for the wedding, and what limits you want to set around that.

Six Months

In the half-year before your big day, you probably already have some big decisions already made. You’ve probably decided on your venue, sent out the invitations, and are narrowing down the buffet and vendor options. Take this time to check in on your goals and narrow down your financial vision.

- Check in on your budget. See how your saving journey is going, if there are any issues, or if there are any adjustments you need to make.

- Go over your guest headcount and vendor expenses. While you don’t have to have the final numbers now, this will give you an estimate as to what your final bill is.

- Find a lawyer for your prenup. Start sketching out your agreement, what conditions you want to have on it.

- Discuss how you want to structure your finances. Do you want to go with separate accounts, joint accounts, or a combination of the two?

- Check in with your financial goals. See how you’re progressing, and if you need to make adjustments to your savings.

Three Months

Three months out, you’ll likely be finalizing your plans with vendors and refining your financial goals. Here’s what you should focus on.

- Review your health insurance plans. See how much a combined premium would cost you, and what benefits you want to have. Keep in mind that premiums and coverage can change from year to year, so you aren’t stuck with one plan forever.

- Discuss life insurance options. See what kind of life insurance plan you want to have, and factor the premium into your budget.

- Start narrowing down your wedding costs. See what your headcount is, confirm your vendors, and make any big changes before it’s too late.

- Do an emergency fund audit. See where you are with your emergency fund, and make it a goal to bulk it up if it falls short.

One Month

One month before the wedding is a busy one. Besides all of the normal pre-wedding preparations, here are some important things to get done before the big day.

- Apply for a marriage license. You will need to do this in the town or city where you are getting married, and you will need to do so before the ceremony, especially since most municipal buildings are closed on weekends.

- Finalize and sign your prenup. Make sure that everything is set, and that you both agree on the terms and conditions. Have a lawyer review it if you prefer, and be sure to have a notary or attorney present when you sign.

- Review your wedding budget. See what vendors still need to be paid, how much cash you need to have on the day of, and if there are any outlying costs.

- Review your honeymoon budget. Agree on what your spending threshold is and finalize your budget, so you don’t have to worry about checking numbers when you’re on vacation.

- Discuss what you want to use the wedding gifts for. Many couples opt for cash in order to pay for a house or the honeymoon. Figure out what you agree on using the funds for, and where they’ll go. As well, take 10% to 20% for yourselves to use on what you want, whether it’s your honeymoon, personal expenses, or just for fun.

The Newlywed Financial Checklist

Once you’ve signed the marriage certificate, you can enjoy all the benefits of being a married couple. As you begin your new life together, be sure to stay on top of your budget, have regular money discussions, and keep things transparent.

In addition, be sure to take care of these administrative tasks once you’ve officially tied the knot:

- Request an official copy of your marriage certificate

- Deposit any cash gifts from the wedding

- Change your name on your financial documents (if you plan on changing it)

- Join your spouse’s health insurance

- List yourself as a beneficiary on your spouse’s life insurance and retirement accounts

- Set up your joint bank account, if you wish to do so

- Iron out your tax strategy if you plan on filing jointly

- Finalize your budget together and start working toward your goals

- Update your wills, trusts, and power of attorney documents

How to Build a Married Budget that Works for You

Building a budget together is more than just combining your spreadsheets and calling it a day. A unified budget not only combines your finances, but is geared toward your personalities, financial philosophies, and shared goals. Here’s Monarch’s quick guide to a newlywed budget.

Establish Your Financial Goals

To begin, discuss the goals you want to achieve with your budget. Do you want to save up for a house? Contribute to a retirement fund? Save for a baby? Or simply get your spending in line?

The key to setting financial goals as a couple is to use the SMART system. SMART stands for Specific, Measurable, Attainable, Relevant, and Time-bound, which will help you form a framework for goals that you can reasonably reach.

Here’s an example of how you would make a goal of establishing an emergency fund together in a SMART framework.

Specific | Establish an emergency fund of $10,000 |

Measurable | Save $400 each month |

Attainable | We can save $400 if we cut down on subscriptions and avoid eating out |

Relevant | An emergency fund will help cover unexpected expenses and prevent us from going into debt |

Timely | We want to have the emergency fund stocked by the end of two years |

Using this framework, you can work toward a goal together that gives you a clear vision of what you want to accomplish, and have a more united front on how you manage your finances.

Choose Your System: Joint, Separate, or Hybrid Finances

Once you’ve figured out your goals, it’s time to discuss how you want to combine your finances. There are a few ways to manage it.

- Separate accounts have you retain your personal bank and charging accounts, and not mix your money at all. While this allows for some privacy and security, it means you may have a less unified outlook to managing your finances as a married couple, and make budgeting more complex.

- Combined accounts merge your money, which makes budgeting and managing bills easier, at the expense of some privacy and making you more liable for your partner’s spending and financial decisions.

- The hybrid approach involves maintaining separate accounts for things like personal expenses while maintaining joint accounts, which offers the best of both worlds.

You’ll also want to discuss how you manage bills and expenses. Some couples will merge finances for the sake of paying off shared expenses like a mortgage, shared groceries, and utilities, while leaving individual subscriptions and personal expenses to the individual.

How you choose to approach combining your finances is up to you. Keep in mind that you’ll be managing your combined finances for the long run, and that you can retool your approach or merge your finances as your circumstances change, such as one spouse losing their job.

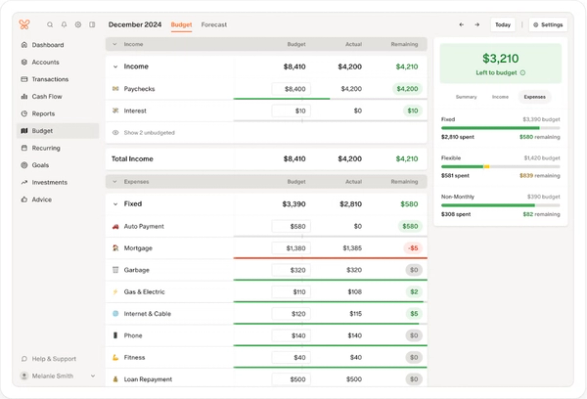

Choose a Budgeting Style

Your budget style should reflect your personality, financial philosophy, and your goals. Discuss with your partner how much flexibility they want in their budget, how much detail is necessary, and how they want to structure their spending.

You have a few options to choose from.

- Flex budgeting has you divide your expenses into Fixed, Flexible, and Non-Monthly, and set parameters around how much each bucket can go to. This is a flexible budgeting style that doesn’t involve as much work as a category budget. This is best for couples who don’t need a detailed budget and want more flexibility in their spending.

- Category budgeting has you divide your expenses into categories (such as Groceries, Housing, Gas, etc.) and determine spending limits from there. You can go broadly with your categories (such as designating Needs and Wants) or be extremely specific. This is best for detail-oriented couples who like to track spending on a granular level.

- Zero-based budgeting has you dedicate every dollar in your cash flow to a specific purpose, whether it’s saving or spending. This is a strict budgeting style that works well for those with irregular or limited income, or couples who like detail in their budget.

- Envelope budgeting has you earmark funds for specific categories (or “envelope”) with a hard limit on spending. Once the funds in the “envelope” run out, you have no more to draw on. Any leftover funds are rolled over to the next month or put into savings. This is a good style for setting hard limits while allowing flexibility to spend and save.

Set Your Categories and Limits

Once you’ve established your budgeting style, set your parameters based on your income and goals. Ideally, you should be setting aside some money each month for saving or investing toward one of your goals. How you structure your budget will allow you to forecast how much you’re saving, and whether you need to pull back on spending.

As always, be on board with your partner about your limits. Be ready to compromise on what you can cut, and remember that a balanced budget is your primary goal.

Check in Frequently

Once you’ve established your budget, be sure to review it on a regular basis. This can be a weekly or monthly occurrence, depending on your preferences. Make sure you’re sticking to your limits, reviewing your goals, ensuring you have enough for your essential expenses, and discussing big purchases as they come up.

How Marriage Changes Your Taxes, Insurance, and Benefits

When you get married, certain parts of your finances will change. From insurance benefits to tax breaks, here’s what to expect.

Life Insurance

Life insurance is considered a must-have for many married couples, as it can provide for the surviving spouse and their children in the event of one spouse’s death. Surviving spouses must have been named as the primary beneficiary in the insurance policy, which is why it’s important to name them in the documentation as soon as possible.

Many insurance companies will offer a discount for married couples, so be sure to inform your provider after you’ve tied the knot.

When applying for life insurance, you have the option of a single policy that pays out to a named beneficiary or set of beneficiaries.

You also have the option of joint policies, which both spouses enter into and pay a premium on.

- First-to-die policies will pay out when one spouse dies, with the surviving spouse receiving benefits.

- Second-to-die policies, usually used for children and estate planning, pays out only when both spouses die.

Medical Insurance

When you get married, it’s considered a qualifying life event, which means that you can change your insurance outside of the open enrollment period. You or your spouse may choose to switch to the other’s plan, especially if one has more benefits, a better deductible, or a lower overall premium. Compare plans and see which one fits your needs best, and how much you’ll be paying with the combined premium.

Make sure you apply for a change as soon as you have your marriage certificate, as you’ll have a limited amount of time. Be sure to supply your marriage certificate or other proof.

Retirement

Marriage can make you eligible to receive your spouse’s retirement benefits depending on the length of the marriage and when the contributions were made.

Any contributions made to your 401(k) or IRA accounts during marriage are considered marital assets, which can be on the line for division if you decide to get divorced.

If your workplace offers a pension plan, your spouse may also be qualified to receive your pension upon your death, depending on the benefit plan in question.

Finally, your spouse is considered the automatic primary beneficiary of your retirement accounts, which means that upon your death, they will receive the cash and assets in those accounts and have them signed over to their name. While this can be changed, it usually requires notarized consent from the spouse, depending on your state’s laws.

Taxes

One of the benefits of marriage is the tax advantages it provides. Here’s a quick breakdown of some of the tax benefits that come with marriage.

What it is | How it benefits you |

You can choose to file jointly | It simplifies the tax process, as there is only one return to full out |

You can file in a lower tax bracket with your combined income | You’ll be taxed at a lower rate, even if you make more, than if you were filing single |

You have eligibility for an Individual Retirement Account (IRA) if your spouse has earned qualifying income | You can contribute to an IRA even if you don’t make any income, which allows you to save for retirement alongside your spouse |

Eligibility for the Earned Income Tax Credit if one spouse doesn’t work and the other does | Your receive a direct cash from the government toward any taxes you owe |

Offsetting one spouse’s income with the other’s business losses | You can file in a lower tax bracket, paying less overall |

Have a higher threshold for the capital gains tax if you’re selling your house | You pay less taxes on any gains you made in your home equity when you sell your house |

Higher threshold for gift and estate taxes | You can receive more in gifts or inheritances and not have to pay tax on them |

Higher deductions for charity contributions | You can deduct more from your income based on qualified charity donations, lowering the amount of income tax you pay |

On the other hand, you can face a few tax disadvantages with marriage, depending on your circumstances. This includes:

What it is | What it means for you |

Lower combined threshold for the capital gains tax | If you and your spouse both have capital gains from selling stocks or assets, the combined amount will count more together than it would if you were filing single |

Phasing out of eligibility for the Earned Income Tax Credit if your combined income is over the threshold | You may not get the tax credit if you and your spouse make too much together |

Higher tax rates for those in the highest tax bracket | The highest tax bracket (37%) is less than double the tax bracket for combined income than if each spouse was filing separately, meaning you pay more taxes with a combined income |

Lower caps on Roth IRA contributions with combined income | You’ll be able to contribute less to your Roth IRA if you and your spouse make too much combined income |

In addition, if you marry filing jointly, your refund may be at risk if your spouse owes taxes or other payments. The IRS can take out part or all of your portion of your refund if your spouse owes back taxes, student loan repayments, child support, alimony, or unemployment benefit overpayments.

Welfare Benefits

Welfare programs like Social security, disability benefits, and veteran’s benefits all change when you get married, both in terms of how your income is calculated and what benefits you and your spouse are eligible for.

When you become married, the government will include your spouse’s income in your household income, which can put you over the income threshold for qualifying. These programs include:

- Supplemental Nutrition Assistance Program (SNAP)

- Supplemental Security Income

- Temporary Assistance for Needy Families

- Medicaid

- Section 8 Housing Voucher Program

- Child Care and Development Fund

- Women, Infants, Children (WIC) Program

What this means is that you or your spouse may receive fewer benefits, or be completely disqualified for benefits, if you make too much of a combined income. This is known as the “marriage penalty.”

The good news is that certain other welfare programs aren’t affected by your combined income, and can qualify your spouse for receiving the same benefits as you do (or vice versa). These include:

- Veterans benefits, including healthcare, Veteran Association loans, pension aid, life insurance, and more.

- Social Security benefits, including the ability to claim full or partial benefits upon retirement age, qualification under disability, or death of the spouse

- Medicare benefits, where if one spouse has earned enough work credits during their working years, the other is eligible for premium-free care.

Before marriage, be sure to review what benefits you are on or expect to receive, and see how your and your spouse’s eligibility will be impacted.

Debt Repayments

How you choose to repay your debt after you marry will be up to you. Any debts you had before marriage are considered your own, which means only your personal assets will be on the line if you declare bankruptcy or if your estate is used to pay off debt post-death. Debt that you take on jointly, however, like a jointly signed mortgage or a co-owned credit card, means that you are both responsible for the repayment, and the payment history will be reported on both your credit scores.

If you are on an income-based repayment plan, then marriage to your spouse can impact how much you pay, as both of your incomes will be used to calculate your repayment. Be sure to factor this in before combining your incomes, and adjust your debt repayment accordingly.

Managing Debt as a Team

Many couples enter their marriage with both individuals carrying debt. Even if you and your spouse are debt-free, it’s likely you’ll take out a loan for a house or a car during your marriage, or have to pay off a large bill or balance over time.

Managing debt as a couple is crucial for financial success. Here’s how to do it.

Determine How You Want to Manage Individual and Shared Debt

While, on paper, debts that you bring into your marriage will remain your own, you will want to sit down and discuss how you handle your balances as a married couple. Whether you choose to help pay off your spouse’s individual balance, leave the repayments solely to them, or contribute proportional to income, it’s key to be on the same page about how you tackle it.

In terms of prioritizing debt, try to tackle your balances with the following hierarchy:

- Level 0 (Highest priority): Debts at 25% interest or higher, which you should focus on first and most aggressively with your payments.

- Level 1 (Middle priority): Debts at 10% to 25% interest, which you should try to refinance or transfer to a low interest balance transfer card.

- Level 2 (Lowest priority): Debts at 10% interest or lower, which you can focus on paying off last, after reaching any other more important financial goals. More specifically, debts below 7% you should focus on only if they’re weighing on you emotionally.

Choose Your Repayment Strategy

Strategizing your repayments will help you pay off your debt faster and save on more interest than simply making the minimum payments. Here’s a quick guide to a few debt repayment strategies.

- The debt snowball has you paying off debts in order of the smallest to largest balance, “snowballing” each payment from each closed balance into the next. This is a good strategy if you want to fuel yourself with the motivation and “wins” of paying off balances quickly.

- The debt avalanche has you tackling debts in order of interest rate, from highest to lowest. This is the most efficient way to pay off debt, and will save you the most on interest.

- The debt defrost has you paying down your debt with either the snowball or avalanche method until you qualify for a 0% balance transfer card, then moving your balance and paying it down during the introductory period. This method works well for high-interest credit card debt, and if you have a 700 credit score or higher.

Whichever method you choose will depend on your needs, though all three can help you pay down your balance quickly.

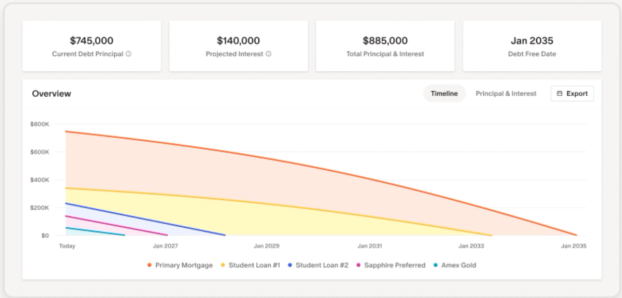

Manage Your Progress and Payments

Keeping an eye on your progress is crucial to staying motivated. As you structure your budget to make room for your repayments and work toward the shared goal of paying off your debt, seeing how your payments are progressing is a huge part of keeping you on track and helping you see the impact of your shared efforts.

Estate Planning Essentials for Newlyweds

While it’s not pleasant to think about the end of your life,it's essential to plan your estate after getting married. Estate planning can save your spouse and your family time and effort in sorting out your affairs, and will ensure that your final wishes are fulfilled as you want them to be. Be sure to consult an experienced attorney when planning out your estate, as they can offer guidance for what you need to file.

Writing a Will

Your will and testament will outline how you want your estate to be distributed, as well as the guardianship of your children should your spouse die as well. A will doesn’t have to be complicated, though the more assets you have, the more detail you’ll have to put into it.

In general, a will contains:

- How your assets are to be distributed

- The beneficiaries of your assets

- Guardianship of children

- Directions for handling logins and accounts for social media and personal devices

- The executor who will handle the proceedings

Once you have written your will, be sure to update it as your assets change, and as you add or remove beneficiaries from the will.

Figuring Out Life Insurance

As mentioned above, life insurance is essential for couples, as it can provide a vital financial cushion for your spouse and family should you pass away.

Besides basic life insurance, which provides a lump sum of cash upon a spouse’s qualified death, you may also want to consider add-ons that pay for a house’s mortgage balance or other loans remaining after death. Be sure to update your beneficiaries to reflect your marriage.

Establishing a Trust

If you plan on leaving behind a large amount of money, investments, or property to a child, relative, or organization, you may want to consider establishing a trust. The grantor (person establishing the trust) gives management of their assets to a trustee, who will distribute it to the beneficiaries based on the grantor’s wishes.

Certain types of trusts are protected from lawsuits, bankruptcies, and other legal orders that may otherwise seize assets, and cannot be accessed without modifying the original agreement. If you are interested in establishing a trust, contact an attorney and see what your options are.

Designating Power of Attorney

A power of attorney (POA) is an essential part of estate planning, as it can make it easier for your spouse to manage your assets and estate in the event of you becoming unable to manage your estate. Without it, your spouse may have a hard time accessing your bank account, selling your family home, or managing care for you if you are unable to make decisions for yourself.

You can draft a POA with the help of a lawyer, with both parties signing and agreeing to it. A POA order can be withdrawn at any point that the principal (person granting the power of attorney) is mentally able to contest it.

Designating End-of-Life Decisions

If you or your spouse end up in a condition that removes your power of decision, such as a coma or dementia, you’ll want to have someone who can make the decision to remove life support. Discuss what you want with your spouse ahead of time: How many and what level of interventions you want, what conditions you are willing to live with, and in what circumstances you would want a Do Not Resuscitate (DNR) or removal of life support order.

What if You're Planning a Second Marriage?

Second marriages are becoming more common, with 26% of all marriages in the United States being remarriages. Whether you and your former spouse decided to separate, or if you are the surviving spouse, there are a few considerations to take when you get married again.

Child Support and Alimony

If you are currently paying child support or alimony to a former spouse or the parent of your children, be sure your partner is aware of this. Since both types of payment can be garnished from your wages or tax refund if you fail to pay, it’s crucial that you are transparent with these payments and how they impact your budget.

If you are receiving alimony, be aware that getting married (or, in certain states, cohabitation) will rescind these benefits. Child support payments should continue as long as the paying individual is still alive, however.

Supporting Existing Children and Grandchildren

Many spouses will have children and/or grandchildren from their previous marriage when they marry for a second time. Even if your children are grown and have left the house, they are still an important part of your personal and financial life. Be sure to discuss these topics with your future spouse so you’re on the same page.

- How children and grandchildren fit into your will

- If there are any established trusts

- If you are funding education, house payments, or other forms of financial aid, and what boundaries you wish to have around that

- If you are willing to help raise any grandchildren if the parents are unable to

Combining Assets

Another point of discussion is how you want to combine your existing assets, especially if you have two houses, multiple retirement accounts, and other investments and assets. While there is no right answer, you’ll want to discuss:

- Where you’ll live, and whether you want to move into one house and keep the other, sell it, or sell both house and buy a new one

- Which assets you want to combine as marital property and which ones you want to keep separate

- Which assets go to whom in trust and will establishments

Trusts and Wills

Depending on the nature of your marriage and previous relationship, you or your spouse may wish to leave some money or assets to their ex-spouse or ex-spouse’s family.

It is crucial that you discuss this ahead of time to prevent confusion and possible conflict when a will or trust is executed. Be transparent with your spouse and your family about how and why you are distributing your assets, update your documentation, and ensure that your attorney/executor is aware of it.

How to Run Your Marriage Money Plan in Monarch

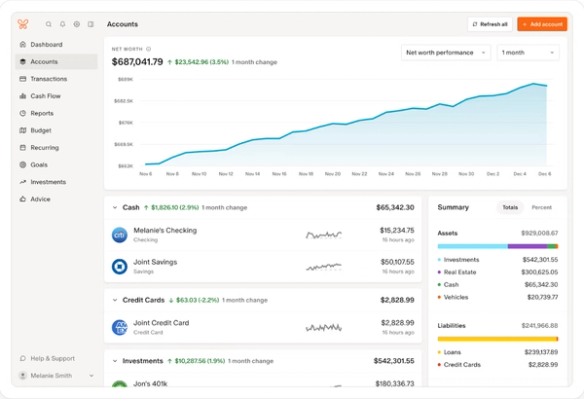

Monarch make financial planning and budgeting a cinch for couples. With shared views, a dynamic budgeting system, and transaction and asset tracking, you can make your weekly budget reviews a snap, help keep your money conversations frequent and productive, and make managing your overall financial picture a part of your day-to-day.

Monarch allows you to set up a shared view of your accounts, combining your transactions, balances, and other information that fuels your budget and your financial outlook. You can toggle between account owners so you can see one partner’s transactions, or view both at a time, and catch unauthorized or out-of-budget expenditures before they get out of hand.

Your budget should reflect your relationship style. Monarch gives you options, with a category budget mode for more detail and a flex budget for a less rigid structure. Monarch logs and automatically categorizes your transactions based on the rules you set, giving you more time for analysis and helping you find solutions to any cash flow issues you have.

Track your net worth and progress on your dashboard to see how your savings, investments, and assets are growing. This way, you can match your net worth to your goals and get a pulse on how your combined wealth is looking over time for a top-down view of your financial progress.

Got goals? Monarch has options for both saving up and paying down, allowing you to track your progress and payments in one place, giving you the momentum and motivation to keep going.

Finally, Monarch generates real-time reports based on your weekly and monthly spending, allowing you to get a pulse on your budgeting and giving you fuel for your money conversations.

If you and your spouse are looking for a way to simplify your finances, inform your money meetings, and get on the same page about managing your household finances, make Monarch a part of your money management plan today.

Build a Strong Financial Foundation as a Couple

Managing your finances as a couple is crucial to a successful marriage. You can set yourself up the right way by having money conversations early, planning out your budget and finances ahead of your wedding, planning your estate, and having a unified view on everything from tackling debt to saving for retirement.

Monarch can help you with shared viewpoint, dynamic transaction tracking, and an all-in-one dashboard that tells you at a glance where you and your spouse stand in your financial journey.

FAQs

Does my spouse's debt become mine after marriage?

Not strictly. If your spouse holds the debt in their name only before the marriage, it is solely theirs to manage. However, there are some risks. If they file for bankruptcy, any joint assets you own can be at risk for liquidation. As well, their minimum payments may change if your combined household income increases, since some creditors will account for both their and your incomes.

Does marriage affect your credit score?

No. Marriage alone doesn’t impact your credit score. What does affect it are any credit lines or loans that you own jointly. If your spouse is on your credit card, the age, utilization ratio, and payment history can impact their score (and vice-versa.) Any joint loans will be reported on both credit scores.

Should married couples have joint or separate bank accounts?

That will depend on how you want to organize your finances. Keeping your accounts separate will keep your finances private from the other spouse. On the other hand, having a joint account can make managing a joint budget easier and instill trust and unity in a couple. Many couples opt to have separate accounts for personal expenses, and one or two joint accounts for shared expenses.

How much should you save before getting married?

While the cost of your wedding will depend on you and your partner’s preferences, you should have enough to cover wedding expenses. In addition, you should have an emergency fund in place, with these amounts based on your lifestyles:

- Three months of expenses, if you don’t own your home, you don’t have an pets, children, or other dependents, your incomes are stable, you have reliable transportation to work, health insurance with deductibles less than three months of expenses, and non-financial safety nets (such as friends and family) who can help you out in an emergency

- Nine to twelve months of expenses if your income is irregular or if your job search, should you lose your job, would take a long time.

- Six months of expenses in all other circumstances.

Is it better to file taxes jointly or separately?

While it depends on your preference, married filing jointly offers many benefits, including a higher tax bracket threshold, higher deduction thresholds, and combined tax credits.

Do we need a prenup?

A prenup can be useful if you are combining assets and debts, or want to outline an alimony agreement if one spouse decides to quit working. A prenup can help you and your spouse get on the same page about where you want your finances to go, how you see yourself sharing assets and debt, and your forecasts for sharing and managing income.

What financial documents should I update after getting married?

In sum: Bank accounts, mortgage documents, life insurance, medical insurance, Social Security, and retirement accounts.

You will also want to update any personal accounts, along with your passport driver’s license, IDs, and Social Security numbers, if you decide to change your name.

How do couples manage money when one earns more?

Many couples choose to go the equitable route by splitting shared expenses, such as rent, proportional to income. Depending on your financial philosophy, you may want to simply combine your incomes and either split bills equally or pull from one general pool of cash.

What is financial infidelity?

Financial infidelity is when one spouse conceals financial information from the other, such as hiding debt, excess spending, or secret savings accounts. What constitutes financial infidelity may depend on your spouse’s definitions of it, since they may want more or less detail into your finances, or be more or less comfortable with you having accounts or cards they are unaware of. Financial infidelity can lead to a loss of trust, financial issues, and general conflict in your relationship if it goes unaddressed.

If you or your spouse has committed financial infidelity, seek counseling from a certified marriage or financial therapist.