The average wedding in 2025 cost between $34,000 and $36,000 in the United States, with about two in three (67%) of couples relying on a personal loan or credit card to help them cover the balance, according to LendingTree.

You don’t have to borrow to pay for the wedding you want. Really, it boils down to figuring out how much you can pay from your savings and sinking fund, figuring out your priorities, budgeting out your categories, and tracking your expenses and adjusting as needed to stick to your limits.

While weddings may feel pricey (and complicated) to plan, with the right framework, you can build a budget that works for you and your partner, stick to your limits, and start off your newlywed life with the right skills and mindset to handle your finances as a couple.

How much does a wedding actually cost?

According to The Knot’s 2026 Real Weddings Data Study, the average wedding in 2025 cost about $34,200 for a ceremony and reception with 117 guests. According to the same study, on average, couples spent:

- Venue: $12,900

- Photographer and videographer: $5,300

- Planner: $2,100

- DJ: $1,800

- Florals: $2,800

- Dress: $2,100

- Cake: $540

- Catering: $80 per guest

- Transportation: $1,100

- Favors: $480

- Invitations and stationery: $510

- Officiant: $2,600

- Alcohol: $2,800

- Rentals: $2,000

While these numbers can give you a starting idea of how much you can expect to spend on these categories, how much you spend on your wedding will depend on your guest list, location, wedding date, and priorities.

That said, if the numbers are giving you sticker shock, there are a few ways to have a more budget-friendly wedding.

How to have a wedding for $1,000

If you’re looking to get married for minimal costs, a budget wedding allows you to celebrate without breaking the bank. This breakdown assumes a guest list of 25 people.

How to do it | Cost | |

Venue | Use a local park or backyard for a venue | $0 |

Rentals | Borrow chairs, tables, and linens from friends and family | $0 |

Music | Borrowed speakers and a mixtape or playlist | $0 |

Catering | Have a local restaurant cater the wedding with drop-off platters | $18 per guest |

Cake | Get a cake from the grocery store | $150 |

Photography | Rely on a friend or family member to take photos | $0 |

Florals | Get florals from a grocery or wholesale store and stick to one bridal bouquet ($50) with five centerpieces (5 at $30 for $150) | $200 |

Attire | One tux rental ($100) and a hand-me-down gown with alterations ($50) | $150 |

Hair and makeup | DIY makeup and hair | $0 |

Invitations/Stationery | Emailed invitations and RSVPs | $0 |

Transportation | No transportation needed for guests | $0 |

Miscellaneous | $100 for the marriage license and officiant fee | $100 |

TOTAL | $1,000 |

This brings your wedding total to $1,000. While actual costs may vary based on your guest list, area, and preferences, you can use this as a starting point to have an affordable wedding that works for you.

How much a courthouse wedding costs

If you’re looking to keep wedding costs at an absolute minimum, consider a courthouse wedding, which you can have for as little as $50. Often couples do this when they wish to have a wedding with few or no guests and minimal wedding costs.

With a courthouse wedding, you, your partner, and at least one witness have an officiant perform the ceremony and sign your marriage license, typically at a government office, though you can opt for somewhere more scenic if your officiant and witness are willing to travel.

At a baseline, a courthouse ceremony will cost you between $50 and $300, depending on the state and jurisdiction you opt to get married in. Your marriage license, which you’ll have to get before the ceremony, will cost between $25 to $50, and the officiant fee will usually run between $25 to $250. You may have to pay additional fees if you have been previously married and need to provide copies of your previous spouse’s death or divorce.

Wedding budget breakdown

Here are some sample wedding budgets based on total budget, guest list, and categories. The estimated amounts are based on vendor costs in The Knot’s 2026 Real Weddings Data Study. While you don’t have to strictly stick to these numbers, this will give you an idea of how different tiers of wedding spending can impact your overall budget.

$15,000 | $30,000 | $60,000 | |

Guest count | 50 | 75 | 100 |

Venue | $3,500 | $10,400 | $23,000 |

Rentals | $1,100 | $1,700 | $3,200 |

Catering | $60 per guest | $70 per guest | $130 per guest |

Cake | $300 | $500 | $800 |

Photography | $1,500 photographer $1,000 videographer | $2,300 photographer $1,500 videographer | $4,000 photographer $3,000 videographer |

Florals | $900 | $1900 | $3800 |

Attire | $1,460 | $2,310 | $3,610 |

Hair and makeup | $200 | $300 | $400 |

Invitations/Stationery | $130 | $245 | $260 |

Transportation | $750 | $1,125 | $1,500 |

Miscellaneous | $1,160 | $2,470 | $3,430 |

How to budget for a wedding

Budgeting for a wedding is similar to planning out your household budget, with a few extra considerations. Here’s how to build a wedding budget.

Step 1: Determine your total wedding budget

Budgeting for a wedding begins with looking at how much you have to work with. If you want to avoid borrowing money, or going over your budget, setting your expectations from the beginning will help you avoid long-term financial snarls.

Before you begin, it’s critical that you don’t entirely empty your savings account or sacrifice your long-term savings goals in order to pay for your wedding. When looking at how much to budget for your wedding, Monarch recommends that you don’t touch:

- Debt repayments

- Fixed monthly payments such as your mortgage/rental payments, utilities, and subscriptions

- Retirement contributions (which should be, at minimum, up to your employer’s match and up to 6% of your gross income)

- Retirement savings

- FSA or HSA contributions

- Insurance payments

- Emergency savings (which should be, at minimum, three to six months of monthly expenses, or 9 to 12 if you are self-employed)

Once you’ve set aside your essential funds, you can start focusing on what you can spend for your wedding. This includes both your and your partner’s savings, any family contributions you expect, and your wedding sinking fund.

How to save for a wedding with a sinking fund

A sinking fund is a savings fund you set up to cover for a planned expense in the future with monthly contributions. You can incorporate a sinking fund into your monthly budget, which will give you a solid idea of how much you’ll have saved by your wedding date.

Your sinking fund amount will be dictated by how many months you have until your wedding and how much you plan to save each month. For example, if you have 20 months until your wedding, and you plan on setting aside $1,000 each month, then your sinking fund will give you $20,000 toward your total wedding budget.

Step 2: Set your priorities

Before you start allocating your budget, sit down with your partner and go over what you want to prioritize in the wedding. This will set the stage for what elements you’re willing to compromise on, what you’re not, and what you don’t need or want to have. It also makes sure that how much you’re allocating from your budget is based on your shared vision and priorities for your wedding, and not vendor pressure for “must-haves.”

Your priorities can include:

- Guest list. How many “must invite” guests are on your lists? Who in your family will expect to be invited? If your parents are contributing, will they dictate certain people be invited? How many guests you have will dictate what venues you can go with and how much you’ll spend per person.

- Venue and location. Where you hold your wedding will dictate how many guests you’ll be able to invite, if you need to add periphery services (such as transportation and equipment rentals), and how much vendors in the area will cost you.

- Decorations. Some couples like to go all-out with the flowers, balloons, centerpieces, and so on. Others prefer to keep it more minimal, or go with the venue’s included decorations.

- Entertainment. As a baseline, many weddings will have a DJ or master of ceremonies to help manage the flow and provide music throughout the event. You may also want to include add-ons like a photo booth, party games, or live musicians.

- Food and drink. For some couples, a plated dinner and an open bar is non-negotiable. For others, a buffet and a cash bar is worth saving some money.

- Level of planning. While an all-inclusive venue might be more expensive than a more DIY venue, for some couples, having fewer moving parts to coordinate is well worth the extra costs. You can also manage this by hiring a wedding planner.

Just as important as recognizing your priorities is organizing them. Sorting out your levels of importance will help you when you need to make cuts to accommodate for something.

When organizing your priorities, it can be helpful to sort your categories into four buckets.

- Non-negotiables. These are your top priorities that are your hard-line fixed costs. Establishing these first will set the structure for the rest of your spending.

- Essentials you can compromise on. These are things you want to include, but are willing to have some wiggle room for, such as limiting an open bar with drink tickets or having less showy centerpieces.

- Nice to have, but you can do without. If you have room in your budget, it’s great to include these. If you need to make cuts, however, these are the first to go.

- Don’t need it, don’t want it. These shouldn’t be on your budget at all. While it may be redundant, being on the same page with your partner about what you don’t want will help you avoid certain vendors and venues and have a unified front when saying “no.”

If you’re having a hard time deciding what to prioritize, ask yourself and your partner: If you had to cut 20% of your budget, what would be the first to go, and what would be the last?

Step 3: Allocate your budget by category

Once you have your budget set, you can start allocating amounts based on the categories and your priorities. Here’s a quick breakdown of each category, how much each one you can expect to spend on with your wedding budget, and some handy ways you can save on costs.

Venue

Cost: $3,500 to $24,800

Your venue will be one of the biggest costs to account for. On average, couples spend $12,900 on the venue, according to The Knot’s wedding survey, with a range of $3,500 to $24,800.

There are a few things to consider when choosing a venue. All-inclusive venues, which include catering, decorations, and other services such as a photographer and a wedding planner, cost more upfront but can save you time and effort, since most of the coordination will be done by the venue.

If you choose to go more of a DIY route, be sure that your vendors are able to coordinate with your venue and to account for extra costs such as vendor travel, insurance, and additional equipment rentals.

Finally, while venue costs tend to be fairly set, the date you pick will affect the final price. Spring, summer, and fall weddings on Saturdays or holiday weekends tend to be more expensive, while “off-season” (January to March) weddings on Sundays or weekdays will tend to be cheaper.

Chairs, tents, and rentals

Cost: $1,100 to $3,200

Depending on your venue and ceremony locations, you may have to rent chairs, tables, a ceremonial arch, a dance floor, table linens, food trays, bathrooms, and other equipment. This can include the labor of setting up and breaking down everything along with delivery, though some couples opt to save money and rely on friends and family to set up. Depending on what you rent and where your venue is, rentals will cost $1,100 to $3,200, according to The Knot.

Catering

Cost: $60 to $130 per guest

Catering is another large cost you can expect for the wedding. According to The Knot, couples spend $80 per guest (for an average of $9,360 with the average number of 117 guests) with a range of $60 to $130 per guest.

It’s also one of the more flexible costs you can account for, as many caterers offer different tiers and add-ons. Buffet dinners tend to be cheaper, while plated catering tends to be more expensive. Some couples, when opting for a more affordable option, will have a morning wedding with a catered brunch, or a noon ceremony with cake and punch instead of a full meal.

While an open bar offers the most selection for guests, some couples opt for a cash bar, a drink ticket system, or a beer and wine bar with one or two signature cocktails, which can save you some money.

Just be sure to communicate what guests can expect on the invitation, and time the ceremony so guests aren’t expecting a dinner and drinks when you’re serving only finger foods.

When choosing a caterer, be sure to check requirements for water and electricity, as some caterers may require access to running water separate from bathrooms and electricity in order to prepare food, which may incur additional charges if you need to rent additional equipment.

Cake

Cost: $300 to $800

Cake or dessert is often a separate charge from catering, and will run you between $300 and $800 depending on the size and complexity of the cake, along with delivery fees from the baker, according to The Knot.

While the cake is often considered the centerpiece of the wedding, some couples opt to save by having a small cutting cake for the cutting ceremony and offering a different dessert for guests, such as cupcakes, donuts, or a cookie table.

Photography and videography

Photographer costs: $1,500 to $4,700

Videographer costs: $1,000 to $3,300

Professional photography will run you between $1,500 to $4,700, according to The Knot, depending on the experience of the photographer, how long you hire them for, and whether you hire a second photographer (also known as a second shooter.)

Many couples also opt for a videographer in order to capture the ceremony and highlights of the reception, which can run you between $1,000 to $3,300, according to The Knot.

Wedding photography is one of the costs you don’t want to skimp on, since wedding photographers tend to be specialized in their skill and great at capturing those don’t-miss moments and have specialized photography and editing equipment. That said, if you’re looking to save and are willing to take the risk, you can hire a photographer starting out in the business who is willing to give you a good deal in exchange for gaining some experience.

Florals

Cost: $900 to $4,800

For some couples, florals are a must-have. For others, they’re optional. This means you have some flexibility. Couples usually spend a range of $900 to $4,800 on florals, according to The Knot.

At minimum, you’ll have a bouquet for the bride and each of the bridal party members.

From there, you can choose whether you want to have floral centerpieces on the tables, or as decoration for the arch and ceremony. Some couples opt for doing florals themselves by buying the flowers in bulk or from the grocery store instead of from a florist. Others skip live flowers entirely and go with wood, plastic, or silk flowers, or alternative centerpiece decoration such as candles.

If you choose to have a florist do your flowers, be sure to factor in delivery fees and whether you need to rent and return the vases/containers, or whether you can keep them.

Music

Cost: $800 to $2,700

For most couples, a DJ is the main way to provide music and emceeing. Besides playing songs, a DJ also provides lighting and helps announce the first dance, speeches, the cake cutting, the bouquet throw, and other parts of the reception. They also provide a sound system and microphones for speeches and announcements. For this, you’ll spend somewhere in the range of $800 to $2,700, according to The Knot.

DJs will generally charge you based on the time hired and the equipment needed, with some offering tiers based on lighting and display add-ons.

Live musicians are another popular option, often playing for the ceremony or reception before the DJ opens the dance floor, or replacing the DJ entirely. Like a DJ, musician charges will depend on how long you hire them for, along with how many musicians and sets you have playing.

Attire

Total cost: $1,460 to $3,610

Generally, the largest attire cost will be for the wedding dress, which can range from $1,200 to $3,200. Some brides opt to save money by going with a simpler dress style or material, or by going with a used or hand-me-down dress from a friend or relative. Keep in mind it may cost you extra to restore or alter a dress so it fits.

Groom attire, on the other hand, tends to cost $260 to $410, with options for renting or buying a suit or tuxedo.

Something else to factor in is whether you cover wedding party attire. Some couples have their bridesmaids and groomsmen cover their own outfits and alterations, while others opt to cover it.

Hair and makeup

Total cost: $200 to $400

If you have a bridal party, it will be expected for you to cover makeup and hair for the bride and the bridesmaids. Hair and makeup crews will charge both for the styling and for the travel involved, which means more remote venues will cost you more if you want the team to travel to you, or if you want to keep them on-call for touchups after the ceremony.

Invitations/Stationery

Cost: $130 to $260

Usually, couples will send out a save the date card, an invitation and RSVP card, invitations for the rehearsal dinner, and thank you notes after the wedding. You’ll also want to have a program for the wedding ceremony, a table seating chart, note cards, signage, and a menu. This will run you about $130 to $260 depending on material and guest list size, according to The Knot.

Stationery costs can be flexible depending on how fancy you want it. Printing companies will typically offer different cost tiers for different types of material and additions such as foiling. Some couples opt to hire a calligrapher to write out the addresses and signs, while others opt to hand-write or print out labels. Mailing invitations will also cost you postage, typically at the rate of one Forever Stamp ($0.78 as of 2026) per envelope.

Transportation

Total cost: $750 to $1,500

If your wedding venue has limited parking or traffic flow issues, or if you want to offer your guests a sober ride service, you may want to hire transport. This can run you $75 to $300 per hour per vehicle, depending on whether you hire a car or a bus, the location, and your number of guests.

Miscellaneous

Cost: Varies

Depending on your style of wedding, you may want to account for smaller, miscellaneous costs such as:

- Wedding party gifts

- Entertainment such as a photo booth

- Favors

- Bathroom amenities such as a bathroom basket

- Sending-away props such as confetti, rose petals, bubbles, or sparklers

- Add-ons like pre-ceremony refreshments or late-night snacks

- Overtime or additional time fees

Hidden wedding costs to account for

Be sure to include these costs in your budget so you don’t get any surprise charges.

Vendor gratuities

Cost: 15% to 20% of vendor charge

Vendors such as servers, your photographer/videographer, bartenders, musicians, your florist, and your DJ will generally expect tips for good or excellent service. While some will have tip jars directly facing guests (such as the bartender) others you’ll tip through your contract or after the event.

As a rule, you should set aside about 15% to 20% of your total vendor contract for vendor gratuities. When looking through your contracts, be sure to check for a gratuity clause or charge, as some vendors will factor gratuities into the total bill, or clarify that gratuities are not required.

Marriage license

Cost: $25 to $50

In order to get married, you’ll need a marriage license, which you’ll need to have in place before the wedding day. Marriage licenses usually cost $25 to $50, with additional fees for paperwork if you need to prove the death or divorce of a previous spouse.

Ceremony and officiant fees

Cost: $50 to $1000

Your venue or ceremony site may charge you for the ceremony on top of the site rental fee, which can run anywhere from $100 to $600.

Officiant fees can run anywhere between $25 to $500, depending on the location and the officiant.

If you choose to have a friend officiate the wedding, they can become ordained for free or for a small fee, depending on the organization offering the ordination.

If you decide to have a ceremony involving a physical object such as a sand ceremony or a handfasting ceremony, be sure to account for the costs of the items, which are often sold in kits or provided by the officiant.

Alterations

Cost: $150 to $1,000

Tailoring fees for wedding outfits, including the bridal gown, bridesmaids dresses, and tuxedoes will cost more than standard tailoring fees, since your tailor will want to make sure everything is perfect for the wedding day. The bridal gown will cost the most to alter, especially if the material is expensive or the design is complex.

Cake cutting fee

Cost: $1 to $3 per guest

If you’re bringing a cake from a service outside of the venue or caterer, such as a baker, you may be charged a cake cutting/serving fee. This can cost $1 to $3 per guest, along with additional fees for renting a cake stand and cutting implements. Be sure to check with your venue if they charge a cutting fee.

Hair and makeup tryouts

Cost: $200 to $400

On top of your standard makeup and hair, you’ll likely want to undergo a trial run of your look for the wedding day. This gives your hairdresser and makeup artist a chance to see what styles suit you best and ensure that you don't have a reaction to any of the products they use. Some stylists may offer a trial at a discount, especially if you travel to their location.

Emergency fund

Cost: 5% to 10% of total budget

Beyond your standard emergency fund, it’s not a bad idea to set aside 5% to 10% of your total wedding budget for any last-minute emergencies, such as last-minute guests, additional catering, emergency dress alterations, or a day-of tent rental if the weather changes. If you don’t end up spending your emergency fund, you can put it toward your shared savings or your honeymoon fund.

Banking and card fees

Cost: $5 to $30

If you’re using a credit card to pay your vendors, you may be charged a 1% to 3% card fee.

Some vendors may require you to pay with a cashier’s check, which is essentially a cash withdrawal from your bank in check form. Cashier’s checks cost $5 to $10 at most banks.

Others may require a wire transfer, which can cost $30 per transfer. Beware of email and phone scams from fraudsters pretending to be vendors, and always verify with the vendor directly that your money is going to the right place.

How to pay for your wedding

There are a few options you can choose when it comes to paying for the big day.

Savings

Using savings gives you the most flexibility in terms of deciding how you want your wedding to go, as well as the most freedom from debt and interest. According to a survey by U.S. News, 44% of couples paid for their wedding without relying on debt.

As mentioned above, you can start off with a combination of savings you already have on hand and a set-in sinking fund based on your incoming funds, which will give you a baseline for what your budget will look like.

If you haven’t already, consider setting up a separate, high-yield savings account for your wedding fund that doesn’t charge any fees. This way you can keep track of your savings and also rack up a bit of extra cash in interest.

Family contributions

Family contributions are common in weddings, with parents contributing 52% of the total wedding budget on average, according to a 2025 survey by Northwestern Mutual. If your family is giving you financial support for the wedding, be sure to sit down and outline expectations with your partner and the family members involved. While some families will contribute cash with no string attached, others may expect to have a say in the guest list, venue, and other aspects.

Boosting your income

Besides using your savings and setting up a sinking fund, increasing your income will help you increase your savings rate as you get closer to your wedding date. Three key ways to increase your income include:

- Taking on a side hustle. Working an extra job such as ridesharing, food delivery, or tutoring can boost your cash flow.

- Cutting your spending. Comb through your budget and see what you can cut down on, whether it’s subscriptions you don’t use, saving on electricity by turning the thermostat up/down, or eating out less.

- Getting a raise. If you’ve been aiming for a promotion, improving your resume by getting certifications, or making headway on a big work project, consider asking your boss for a pay bump.

Personal loan or credit card

Instead of using savings, some couples opt to take out a loan or pay for their wedding with their credit card balance. According to LendingTree, 67% of newlywed couples used debt to cover their wedding expenses, with over half (52%) taking more than six months to pay it off, with 41% taking over a year to pay off their balance.

Using a card or a loan to pay for your wedding requires a serious conversation with your future spouse and a solid action plan in place for how you plan to pay off the balance. With credit card interest rates hovering around 24% as of June 2026, you may end up spending more on interest than you do your initial balance.

Starting off married life with debt can pose an extra challenge, so it’s critical you have the conversation with your partner about whether it’s worth it to pay for the big day.

How to stick to your wedding budget

Like your everyday budget, sticking to your wedding budget takes discipline and focus on your final goal. Here are a few ways you can stay on top of your budget and have the wedding you want.

- Figure out your vendors and costs as soon as possible. Knowing your costs as soon as possible will help you plan accordingly. As well, booking ahead will help you avoid a last-minute scramble, give you more options to shop around, and help you avoid price increases.

- Check in on a monthly basis. As part of your regular “money dates” with your partner, check in on where your wedding budget is, see how much your spending aligns with your planning, and check that your saving goals are on track.

- Run large purchases by your partner. Discuss what your threshold for a “big purchase” is (such as $500) and agree that you’ll get mutual consent before deciding if you’ll go through with it.

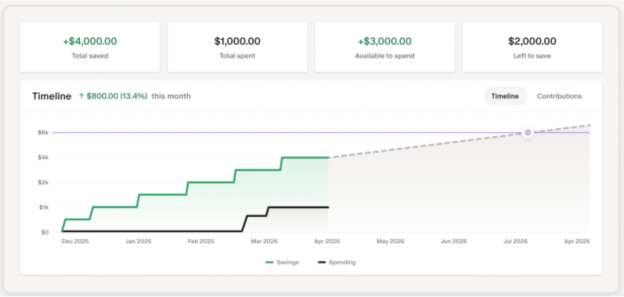

- Automate your tracking and savings. Tools like Monarch can help you track your saving and spending in the background, so you don’t have to manually track your cash flow and can get a unified look at where your budget is going.

What to do when you go over your wedding budget

Staying on budget for your wedding can be a challenge, especially as inflation can increase vendor prices in the months leading up to your wedding day. According to a survey by The Knot, 41% of couples went over budget, with 55% of couples reworking their wedding plan and cutting expenses in order to keep their costs in check.

If you find that you’re approaching — or have already gone over — the limits of your budget, here are a few steps you can take to manage your wedding expenses.

- Fall back to your priority list. As mentioned above, use your priority cascade to determine what you can cut first, and how much you can cut it down by.

- Tap in on friends and family. If they’re willing and able, you might be able to delegate some tasks to your network, such as picking up and arranging tables, designing invitations, or making decorations, instead of paying extra for those tasks.

- See where you can snag discounts from vendors. Some vendors may be willing to shave off some add-on services for a discount, such as having the DJ use fewer lights or cutting a buffet item with a caterer.

- Evaluate your guest list. Consider limiting plus-ones to married and long-term partners, or cutting out more casual friends you haven’t kept in touch with.

- Increase your sinking fund. The more you save, the more you can pay, especially if you make adjustments to your everyday budget.

After the wedding: Your first budget together

As newlyweds, starting your finances off on the right foot will set the stage for financial success throughout your relationship.

After the wedding

As soon as you can after the wedding, you should start planning your first money date together.

Just as marriage experts recommend you continue to “date” your spouse after the wedding, financial experts recommend you hold regular money dates in order to stay on the same page. Money dates should be regular (at least once a month), and include reviewing your budget, setting and checking in on financial goals, discussing large purchases, and making sure you’re sticking to your larger financial plan.

In the first 30 days

In the first month of wedded life, you’ll want to:

- Update your accounts. This includes updating your name (if you have chosen to change it), adding your spouse as a beneficiary on insurance policies, or adding yourself or your spouse to accounts or policies, should you choose to do so

- Set up a joint budget. While you can choose to keep some personal purchases separate, having a joint budget will give you a unified view of your shared finances, especially as you start thinking about your shared goals.

- Consolidate your financial view. Combine your incomes, expenses, assets, and liabilities so you get an idea of your unified financial view and net worth.

- Review your wedding budget. Make sure all your vendors are paid, that any card balances are paid off, check if you’re on, over, or under budget.

- Deposit cash gifts. Choose where you’ll put your gifts and how you plan to spend (or save them) and keep track of who contributed them so you can send thank you notes.

In the first 90 days

In the first three months, on top of creating a budget, you’ll want to build out your larger financial plan as a couple.

- Establish your emergency fund. Figure out how much you need to save based on your financial circumstances (Monarch recommends three to six months of monthly expenses for most couples, or 9 to 12 for couples with more variable income), and set up a goal and timeline for your savings.

- Set one to two shared goals. Besides your emergency fund, decide what other financial goals you want to tackle, whether it’s saving for a vacation, paying down debt, or contributing to an investment portfolio.

- Figure out your next milestone. After the wedding, decide what comes next for you and your spouse, whether it’s buying a house, starting a family, or launching a business together.

How Monarch helps you budget for the big day and beyond

Saving for your wedding shouldn’t leave you lost in spreadsheets and hunting down old receipts. Track your expenses, stay on top of your savings goals, and create a unified budget for your wedding and beyond with Monarch.

When you start out with your savings goals, you can add in a save up goal that adds your monthly savings amount to your monthly budget and tracks your savings progress.

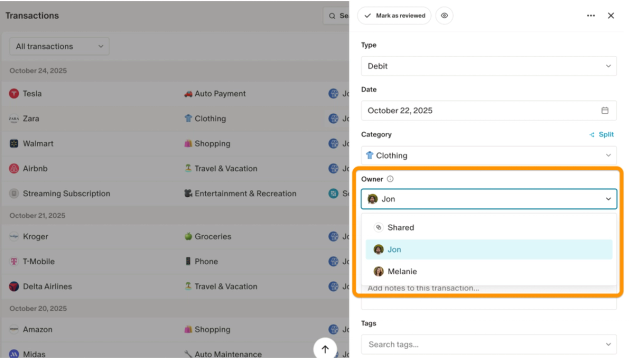

Your partner stays in the loop on your budgeting with shared household views, where both account members can see the same budget, goals, cash flow, and progress on mobile and web with only one subscription.

While your wedding budget is part of your larger budget, you can split out your transactions (which are tracked automatically) by creating custom categories for different wedding expenses. In category budget mode, you can allocate your overall wedding budget amount to different categories under one group, with rollover options to account for expenses you plan on paying down in future months.

After the wedding day, you can pivot your budget for both everyday expenses and long-term planning as you set up your emergency fund and plan for future shared milestones like saving for a house or starting a family.

Start your marriage on solid financial footing

Paying for your wedding is often the first big financial decision and milestone for couples, and planning it the right way can start you off on the right foot and help you avoid taking on debt.

While the cost might seem overwhelming at first, breaking down your spending, keeping your spending within your parameters, and saving over time aren’t just crucial to paying for your big day — they’re the critical skills you’re building with your partner that will come in handy when you buy your first home, have children, save for retirement, or handle financial emergencies together.

FAQs

How much should a couple save for a wedding per month?

Take your total wedding budget, subtract the savings you plan to use and any family contributions you expect, and then divide the remainder by how many months you have until the wedding. For example, if you’re planning a $35,000 wedding and have $10,000 saved with $5,000 in family contributions coming, you’ll have $20,000 left to save. Over 20 months, you’ll need to save $1,000 per month.

What percentage of income should a wedding cost?

That depends on your priorities. In general, you shouldn’t be spending more than what you’re willing to take from your savings, what your family is willing to contribute, and what you can save from your monthly sinking fund.

Is $20,000 a realistic wedding budget?

Yes, you can feasibly have a wedding with $20,000. Your biggest consideration will be your venue and your guest list, which will help determine how much you spend in other categories. Consider how much you want to spend per guest. With 50 guests, you’ll be spending $400 per guest, which is well within the parameters for catering, drinks, venue costs and other expenses. At 100 guests, you’ll be spending $200 per guest, which means you may need to make some cuts in order to fit everything in your budget.

How do I talk to my partner about the wedding budget?

Start off with an idea of how much you’re willing to spend from savings and how much you’re willing to receive from family and cover with loans or credit cards. From there, you can start discussing priorities and allocating amounts to your categories. As you continue the process, be sure to keep discussing your budget on a regular basis and check in for large transactions.

What do most couples forget to include in the wedding budget?

Some of the more looked-over expenses include:

- Vendor gratuities (10% to 20% of your total vendor bills)

- Officiant and license fees

- Bank and card fees

- Delivery fees

- Alterations

- Cake and cutting fees

- Hair and makeup tryouts

Should we combine finances before or after the wedding?

While that depends on your lifestyle and your level of comfort, you will need to combine your finances to a certain degree if you both plan on paying for the wedding. Creating a shared wedding budget with shared goals, contributions, and savings can be a good first step in combining your finances before going all the way.